You might be dealing with a house you don't want to put on the market at all.

Maybe you're behind on payments and don't have time for cleaning, repairs, photos, and weeks of uncertainty. Maybe you inherited a property in Fayetteville or Spring Lake and live in another state. Maybe PCS orders hit and now you're trying to solve a housing problem before you solve the move itself.

That’s where the phrase we buy houses in any condition stops sounding like a slogan and starts sounding like a practical option. But it only helps if you understand the trade-offs, the process, and how to vet the buyer before you sign anything.

Understanding Cash Home Sales in Any Condition

In Cumberland County, urgency is common. Sellers call when a house has storm damage, bad tenants, code notices, probate complications, or a hard move-out deadline tied to Fort Bragg. Traditional listing works best when a seller has time, money for prep, and the ability to wait through showings and buyer financing. A lot of local owners don't have that luxury.

Nationally, all-cash buyers made up 32% of U.S. home sales in January 2024, the highest share since June 2014, according to the National Association of Realtors economist outlook on all-cash buyers. That matters in Cumberland County because relocation is a real driver here, especially around military moves and out-of-area ownership.

Why sellers choose this route

A cash buyer solves a different problem than a retail buyer.

A retail buyer usually wants financing, inspections, repair negotiations, and a home that can survive appraisal. A direct cash buyer is looking at the property as it sits today. Roof leaks, old plumbing, junk left behind, foundation concerns, unpaid taxes, inherited contents, tenant damage. Those issues don't automatically kill the deal.

The appeal is usually one of these:

- Timing control: You need a fast answer and a dependable closing date.

- Condition relief: You don't want to repair, clean, stage, or clear out everything first.

- Privacy: You don't want open houses, signs, lockboxes, or repeated walkthroughs.

- Problem solving: You need a buyer who can work around liens, title issues, or occupancy headaches.

Practical rule: If the house can sell conventionally with light effort and no deadline pressure, listing often gives you more upside. If the house is dragging a life problem behind it, speed and certainty can matter more than maximum price.

What as-is actually means

"As-is" doesn't mean the buyer ignores defects. It means the buyer prices the defects into the offer instead of asking you to fix them first.

That distinction matters. Sellers sometimes hear "we buy houses in any condition" and assume every buyer will pay near retail. That isn't how this works. You're selling convenience, certainty, and problem transfer along with the property.

If you need a plain-English breakdown of what a direct offer really is, this guide on what is a cash offer on a house is a useful starting point.

Preparing to Sell As-Is in Cumberland County

The fastest closings usually come from the best-prepared sellers.

Not polished sellers. Prepared sellers.

If you're requesting an as-is offer, gather the pieces that answer the buyer's main questions before the first call. That keeps the walkthrough cleaner, reduces back-and-forth, and helps prevent last-minute title surprises.

The local seller checklist

Start with the paperwork that affects ownership and payoff.

- Mortgage information: Bring the most recent statement and lender contact details if there's still a loan.

- Ownership documents: Deed, probate paperwork if applicable, trust paperwork if applicable, and anything showing who has authority to sign.

- Lien and notice records: Tax notices, HOA letters, judgment paperwork, utility balances, code enforcement notices, or demolition warnings.

- Occupancy status: Is the property vacant, owner-occupied, or tenant-occupied? If tenants are involved, keep the lease, payment history, and any written notices.

- Basic property facts: Age of roof if known, HVAC issues, water damage history, plumbing leaks, electrical concerns, fire damage, foundation movement, or unpermitted work.

A serious buyer doesn't need a perfect file to make an offer. But the closer your information is to reality, the less likely the number changes later.

What to note before the walkthrough

Walk room by room and make a blunt list.

Don't try to soften it. Don't guess at what "shouldn't matter." Distressed property deals go better when everyone works from the same facts.

Write down things like:

- Exterior problems: Soft spots, drainage issues, siding damage, broken windows, fencing, rot, sagging porches.

- Interior trouble areas: Subfloor damage, mold smell, stained ceilings, missing fixtures, nonworking bathrooms, kitchen leaks.

- Systems and safety items: HVAC not cooling, panel concerns, old water heater, sewer backups, missing smoke detectors.

- People issues: Occupants who won't cooperate, relatives still sorting belongings, inherited contents, or abandoned personal property.

The fastest way to lose time is to hide a major issue and let it surface later during title work or the property review.

Remote sale prep for out-of-state owners

This is one of the biggest gaps in most guides.

Absentee owners often aren't worried about the offer first. They're worried about control. Who gets access? Who verifies the condition? Who signs if they can't come back to North Carolina?

Recent North Carolina rules make remote closings more practical for absentee sellers. One source notes that NC’s 2025 digital notarization laws allow fully remote closings in 7 to 10 days and reduce fraud risks by 20% for absentee sellers, as discussed in this article on remote sales for out-of-state owners.

That doesn't eliminate the need for diligence. It changes the logistics.

For remote owners, add these items to your prep list:

- ID verification: Make sure your name matches the vesting on title documents.

- Access plan: Decide who can open the property for a walkthrough if you can't.

- Photo and video package: Current photos help reduce misunderstandings early.

- Signing authority: If another family member will sign, confirm legal authority before closing week.

- Wire instructions: Verify them directly with the closing office, not by forwarding email chains.

If you want a seller-focused primer before you request offers, this overview of what is an as-is home sale is worth reading.

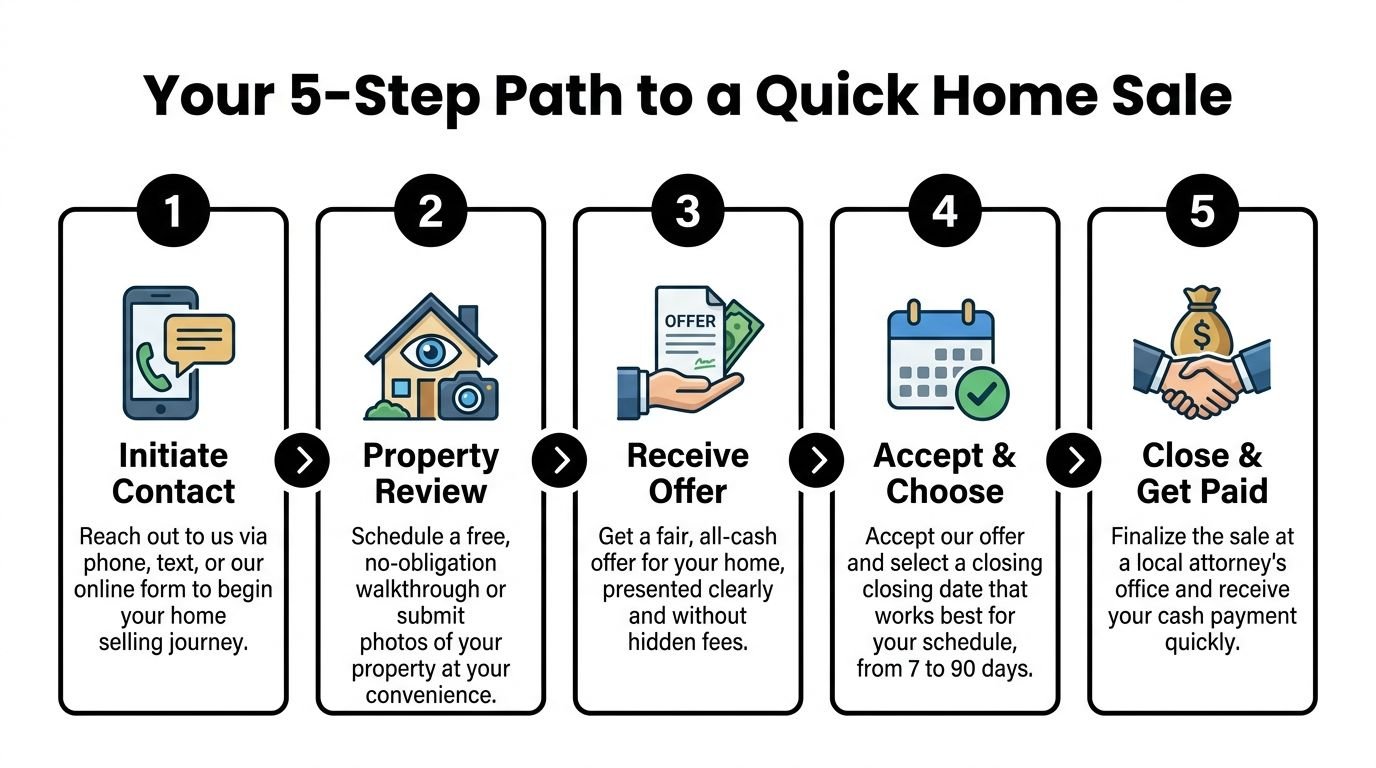

Step-by-Step Selling to DIL Group Buyers

The strongest cash sale process is simple, but it shouldn't feel vague.

You should know what happens first, what the buyer needs from you, when the offer comes, and what could slow things down. A good process cuts friction. It doesn't hide steps.

Step one starts with clear property facts

The first contact is usually by phone, text, or online form.

This part should be short. Address, occupancy, condition, timeline, and whether there are liens, foreclosure concerns, inherited ownership, or tenant issues. A seller who gives straight answers here usually gets a cleaner offer process later.

If you're local, this can move quickly. If you're out of state, send photos early and identify who can provide access.

Step two is the property review

A real buyer needs to understand what they're buying.

That might be a single walkthrough, or a virtual review supported by photos, records, and a local contact. The point isn't to criticize the house. The point is to confirm repair scope, title concerns, and whether the situation matches the intake call.

Watch for buyers who act like details don't matter. In distressed sales, details always matter.

Common review items include:

- Major repairs: Roof, foundation, plumbing, electrical, HVAC, moisture intrusion

- Layout issues: Additions, conversions, or work that may not match records

- Access problems: Locked rooms, hoarding, animals, or uncooperative occupants

- Sale blockers: Open permits, liens, probate questions, or missing heirs

Step three is the offer

At this stage, sellers need clarity, not pressure.

One source describing the standard investor workflow says the 5-step cash buying method closes in 1 to 3 weeks instead of 2 to 3 months, with a 90% success rate on accepted offers, as outlined in this breakdown of the cash home buying process.

The offer should state the purchase price, whether the buyer is covering normal transaction costs on their side, whether the sale is as-is, and what conditions remain before closing. If a buyer can't explain the offer in plain terms, keep shopping.

Ask one direct question: "What could cause this price to change after I sign?"

If the answer is fuzzy, the contract probably is too.

For a quick overview of the basic path from request to closing, review 3-step home sale.

Step four is choosing the closing date

This step matters more in Cumberland County than many sellers expect.

A PCS seller may need to close before reporting. An inherited-property seller may need more time to clear family contents. A landlord may want enough runway to coordinate occupant turnover. A seller in pre-foreclosure may need the fastest viable date.

A practical buyer should be able to work with your timing, not just theirs.

Step five is closing and getting paid

At closing, title documents are signed and funds are wired.

The best version of this step feels quiet. No surprise fees. No last-minute demands for repairs. No moving target on price because the buyer finally "noticed" what was obvious from day one.

What works well in local transactions

In Cumberland County, the cleanest transactions usually share a few traits:

- One honest walkthrough: The property gets reviewed once, thoroughly.

- Good title coordination: Any mortgage payoff, lien issue, or heirship question gets addressed early.

- Seller-specific timing: The date is built around the seller's actual problem, not an arbitrary closing window.

- Written expectations: Personal property left behind, utility transfer, and key handoff are agreed to in advance.

What tends to go sideways

Deals usually become messy for predictable reasons.

- Hidden occupancy issues: Sellers say a house is vacant when someone is still living there.

- Unclear ownership: Family members disagree about who can sell.

- Contract vagueness: The buyer reserves broad cancellation rights.

- Remote confusion: Out-of-state owners don't set up access or signing authority early enough.

A cash process should feel shorter than a listing, not sloppier than one.

Calculating Offers and Negotiation Points

Most sellers want to know one thing first. How did you get to that number?

A reasonable cash offer isn't random. It starts with what the property could be worth after repairs, then works backward through condition, holding risk, and transaction burden. You don't need investor jargon to understand it, but you do need to know the moving parts.

Offer Calculation Breakdown

| Component | Explanation |

|---|---|

| After-repair value | The buyer estimates what the house could sell for after needed work, using nearby comparable sales and current local demand. |

| Repair scope | This includes visible issues such as roof, flooring, plumbing, HVAC, cosmetic updates, cleanup, and debris removal. |

| Carrying costs | The buyer accounts for the cost of owning the property during repairs and resale, including time, utilities, insurance, and project risk. |

| Profit margin | Investors build in a margin because they are taking on repair risk, resale risk, and capital exposure. |

| Title and situation complexity | Liens, probate, tenants, code violations, or access problems can affect the offer because they create delays or legal work. |

| Seller convenience value | A faster close, no showings, no repairs, and leaving unwanted contents behind often justify a lower but more certain number. |

What experienced sellers ask about

Good negotiation doesn't mean arguing every line item. It means asking the right questions.

If the repair number feels heavy, ask the buyer which items drive it. If the house has newer systems or you have contractor estimates, show them. If the title looks cleaner than the buyer assumed, say so. If you can make access easier or leave on a schedule that reduces holding time, that may help too.

The strongest negotiation points are usually practical:

- Clean access: Easier inspection and contractor review reduces uncertainty.

- Documentation: Receipts, permits, or recent repair records can improve confidence.

- Flexible possession: A closing date that fits the buyer's workflow can strengthen the deal.

- Multiple bids: Competing offers often expose who is pricing fairly and who is fishing low.

What doesn't work

Some sellers anchor on what the house would be worth if it were fully renovated and owner-occupied tomorrow.

That isn't the same as today's as-is value. A cash buyer is not paying retail for your future plan. They're paying for the property plus the problems they are agreeing to absorb.

Another weak move is withholding obvious defects because you think revealing them lowers the offer. Usually the opposite happens. Hidden issues don't improve pricing. They damage trust and increase the chance of retrading later.

Bring facts, not optimism. A written roof quote, clear photos, and a payoff statement help more than saying "it just needs cosmetic work."

Handling Special Situations When You Need Speed

Cumberland County sellers rarely call because everything is simple.

They call because the house is tied to a deadline, a family problem, or a property issue that keeps getting worse the longer it sits. In those situations, a direct cash sale is less about convenience and more about reducing damage.

Military PCS pressure near Fort Bragg

Military moves create one of the clearest speed cases in this market.

A household gets orders. One spouse may already be coordinating the next base, school timing, movers, and temporary housing. The house at home still needs to be sold. Showings become disruptive fast, especially if one spouse deploys or leaves early.

One industry source says Fort Bragg’s 2025 PCS cycle impacted over 10,000 families, and cash buyers helped sellers save $8,000+ in holding costs by closing in 7 to 14 days instead of 90+ days, according to this article related to Fort Bragg PCS and fast cash sales.

That doesn't mean every military seller should take a cash offer. It means speed has a real dollar value when dual payments, vacancy, and travel overlap.

Inherited houses with long-distance family coordination

Inherited property sales often stall because nobody wants the house, but everyone has a different opinion about how to handle it.

One heir wants top dollar. Another wants it gone. A third lives out of state and can't manage cleanup or access. The property sits. Yard problems grow. Utilities stay on. The city notices deferred maintenance before the family reaches agreement.

The practical path is usually this:

- confirm who has legal authority to sell

- collect the documents tied to the estate

- decide what stays in the house

- get a direct offer based on actual condition

- solve title and closing logistics before emotions take over again

The common mistake is trying to "lightly list" a house that still contains years of contents and deferred maintenance. That usually creates more friction than value.

Landlords with bad tenants or neglected rentals

Rental properties create their own version of urgency.

An owner in another city may be dealing with missed rent, lease disputes, property damage, trash accumulation, or tenants who make access difficult. Listing that kind of house is hard because every showing depends on cooperation you may not have.

A direct buyer can sometimes work around that problem more effectively than a retail listing because the property doesn't need to be show-ready. The important part is being honest about the tenant situation up front, including whether the lease is active, whether rent is being paid, and whether the occupants are likely to resist entry or move-out.

Pre-foreclosure and credit protection

When sellers are behind on payments, the biggest mistake is waiting for certainty before making calls.

You don't need every answer before exploring options. You need enough time to compare them.

In a distressed timeline, what helps most is a buyer and closing team that can quickly identify the mortgage payoff, coordinate title issues, and set a closing date that beats the lender timeline. What hurts is spending weeks chasing cosmetic fixes that don't change the core problem.

If the house problem is really a time problem, solve for time first.

Closing Timeline and Required Documents

Once a seller accepts an offer, the transaction shifts from valuation to execution.

This is the phase where good deals stay smooth or start drifting. Most delays don't come from the house itself. They come from title questions, missing signatures, payoff gaps, or remote sellers waiting too long to gather documents.

What the title company or closing attorney usually needs

Expect to provide the documents that prove identity, ownership, and payoff status.

Use this as your working checklist:

- Government ID: Current photo identification for every required signer.

- Deed or ownership paperwork: Anything showing how title is held.

- Mortgage payoff information: Loan account details and lender contact info.

- Estate or trust documents: If the owner is deceased or the property is held in a trust.

- Power of attorney documents: If someone else will sign on the seller's behalf.

- HOA or tax notices: If balances or status need to be verified.

- Tenant documents: Lease, notices, or occupancy records if the property isn't vacant.

If there are liens, judgments, or old ownership issues, disclose them early. "Maybe it won't come up" is not a strategy in title work.

A practical timeline

Cash sales move faster because they remove mortgage underwriting and appraisal risk. They still require sequence.

A normal closing path often looks like this:

- Offer accepted and contract signed.

- Title opened with the closing office.

- Payoffs ordered for mortgage or other recorded balances.

- Title review completed and defects addressed if needed.

- Signing scheduled in person or remotely.

- Funds wired after closing conditions are complete.

- Keys or access transferred based on the agreement.

The exact timing depends on title clarity, seller responsiveness, and whether all decision-makers are ready to sign.

Remote closings for out-of-state owners

Remote closing works best when the seller plans for it early.

That means verifying names exactly as they appear on title, confirming where documents will be signed, and avoiding last-minute changes in banking instructions. If a power of attorney is needed, line that up before closing week, not during it.

A short explainer can help if you're new to direct-sale closings:

What to expect on closing day

Closing day should feel administrative, not dramatic.

In most transactions, the seller signs the final documents, the closing office confirms any payoffs, and then funds are released by wire. If the property is vacant, keys, garage remotes, and codes are turned over as agreed. If contents are staying behind, that should already be written into the deal.

Common delay triggers

A few issues create most closing delays:

- Name mismatches: ID doesn't match vesting.

- Missing heirs or signatures: Someone with legal interest hasn't signed.

- Payoff surprises: Loan balances or lien details weren't confirmed early.

- Wire confusion: Sellers change account instructions at the last minute.

- Occupancy disputes: Tenants or family members haven't vacated.

The best closing is boring. All the hard work should be done before the signing appointment.

Benefits Trade-Offs and Buyer Vetting

Selling to a cash buyer works well when the problem is speed, condition, complexity, or all three at once.

It does not work well when a seller wants retail pricing without doing retail-sale preparation. That mismatch causes most disappointment.

The biggest trade-off is price versus convenience. A Drexel University study found that investor purchases in off-market deals sold for 51% less than comparable MLS sales, which is a sharp reminder that speed usually comes with a discount. The study is summarized in Drexel's report on off-market investor home purchases.

That doesn't make direct sales good or bad by itself. It makes them situational.

What you gain

- Speed and certainty: Fast timelines matter when foreclosure, relocation, or vacancy costs are pressing.

- No repair burden: You can sell the house in its current state.

- Simpler logistics: Fewer showings, less prep, and less disruption.

- Problem transfer: The buyer takes on the rehab, resale risk, and much of the coordination burden.

What you give up

- Higher possible sale price: Listing usually offers more upside when time and condition allow.

- Broad market exposure: You're selling to a narrower buyer pool.

- Negotiation advantage from retail demand: Distressed direct-sale deals are priced around risk, not dream value.

The vetting checklist most guides miss

Not all buyers who say they buy houses in any condition are equal. Some are end buyers. Some are wholesalers. Some are organized. Some are just marketing.

Use this checklist before you sign:

- Ask who is buying: Are they the direct buyer or assigning the contract?

- Request proof of funds: A serious cash buyer should be ready for that question.

- Read cancellation language: Look for broad exit clauses that let the buyer walk for almost any reason.

- Confirm local transaction experience: Cumberland County title, tenant, and inherited-property issues are easier for buyers who know the area.

- Check communication quality: Slow answers early usually become slower answers during title work.

- Review all fees in writing: The contract should make the economics plain.

- Ask what changes the price: Force clarity before you commit.

- Compare more than one offer: Even in urgent situations, one extra conversation can reveal a lot.

The right buyer isn't just the one with the quickest pitch. It's the one whose process stays consistent from first call to closing.

If you need to sell a house fast in Fayetteville, Hope Mills, Spring Lake, Eastover, Stedman, Raeford, Parkton, Dunn, Grays Creek, or nearby areas, DIL Group Buyers offers a direct local option. They buy houses in any condition, work with inherited properties, foreclosure situations, bad-tenant rentals, military PCS timelines, and out-of-state owners, and they focus on straightforward closings without realtor commissions, attorney fees, or repair demands. If your priority is a clear offer and a closing date that fits your situation, reach out and get the numbers for your property.