A short sale is when you sell your house for less than you owe on the mortgage, and the lender agrees to accept that reduced payoff instead of forcing foreclosure. In current markets where short sales have reappeared, they still make up only 0.5% of local sales in some areas, and even with improved timelines, many still take 3 to 4 months and only 1 in 3 listings close in some markets.

If you're in Cumberland County and you're reading this because the mortgage is behind, PCS orders just landed, a tenant trashed the place, or the house won't sell for what you owe, you're not looking for theory. You need to know whether a short sale is a real way out, how ugly the process gets, and whether there's a faster path that protects your finances better.

That's what this guide is about. Plain English. No fluff. If you've been asking what is a short sale on a house, the basic answer is simple. The decision is not. A short sale can help some homeowners avoid foreclosure, but it comes with paperwork, lender control, delays, and real uncertainty. For many Fayetteville area owners, especially military families on a deadline, certainty matters more than squeezing through a process the bank may reject anyway.

Understanding the Short Sale Option

When most homeowners first hear the term short sale, they assume it means a fast sale. It doesn't.

A short sale means you're selling the property for less than the mortgage balance, and the bank has to approve that decision because the sale won't pay off the full debt. You're "short" on what the lender is owed. That's the whole idea.

When this becomes real in Fayetteville

This usually stops being an abstract real estate term when life changes fast.

Maybe you bought during a stronger market and now the house won't sell high enough to cover the loan. Maybe you got PCS orders and can't stay to manage a listing. Maybe your payment jumped from manageable to impossible after job loss, divorce, or another hit to your budget. Maybe you're already behind and trying to stop things from getting worse.

In those situations, a short sale can be one tool. It's not a magic fix. It's a negotiation with your lender where you ask them to accept a loss now because the alternative may be foreclosure later.

What a short sale is trying to accomplish

Its purpose is damage control.

For you, the goal is usually to avoid a foreclosure on your record and get out from under a house you can't keep. For the lender, the goal is to lose less money than they might lose in a foreclosure and resale.

Practical rule: If your biggest problem is time, a short sale is often a difficult fit. If your biggest problem is negative equity and you still have some runway, it may be worth evaluating.

Here's the simplest way to consider it:

- You owe more than the house can sell for. The sale proceeds won't fully pay the loan.

- The bank must approve the deal. You can't just accept an offer and move on.

- You usually need hardship. The lender wants proof that you're not just walking away for convenience.

- You don't control the timeline. The bank does.

The question you should really be asking

Most homeowners ask, "What is a short sale on a house?"

The better question is, "Is a short sale the right move for my situation in Cumberland County?"

That's a different issue entirely. If you're current on payments, have time, and can document real hardship, a short sale might be worth pursuing. If foreclosure is close, you're already out of state, or you need a certain closing date because the Army isn't waiting on your lender, then speed and certainty may matter more than the label attached to the sale.

How a Short Sale Really Works

A short sale starts with a math problem and turns into a bank approval problem.

If you owe more than the property can sell for, you're underwater. It's similar to selling a car for less than the auto loan balance. If the car buyer pays $15,000 but the loan payoff is $20,000, somebody has to agree to absorb the missing amount. With a house, that "somebody" is usually the mortgage lender, and they won't do it casually.

The two things lenders look for first

Before a lender even considers approval, they usually want to see two basics.

- Financial hardship

- Insolvency or negative equity

A hardship means something changed and you can't reasonably keep paying as agreed. Negative equity means the house isn't worth enough to clear the debt. Both matter because the bank wants to know this is a legitimate loss mitigation case, not just seller's remorse.

The documentation is not optional. Old Republic Title's overview of the short sale process states that approval hinges on proving hardship through a hardship letter, bank statements, and expense proof, and notes that lenders approve short sales because foreclosure auctions often yield 20% to 30% below market value.

What you usually have to submit

A lender review package often includes:

- A hardship letter: Explain why you can't continue with the mortgage.

- Bank statements and income records: The lender wants to see your actual financial condition.

- Expense documentation: Monthly obligations matter because the lender is judging ability to pay.

- Sale documents: Offer, estimated net sheet, and market support for the price.

That package is where many short sales slow down. Missing pages, outdated statements, inconsistent numbers, or a weak hardship explanation can stall the file fast.

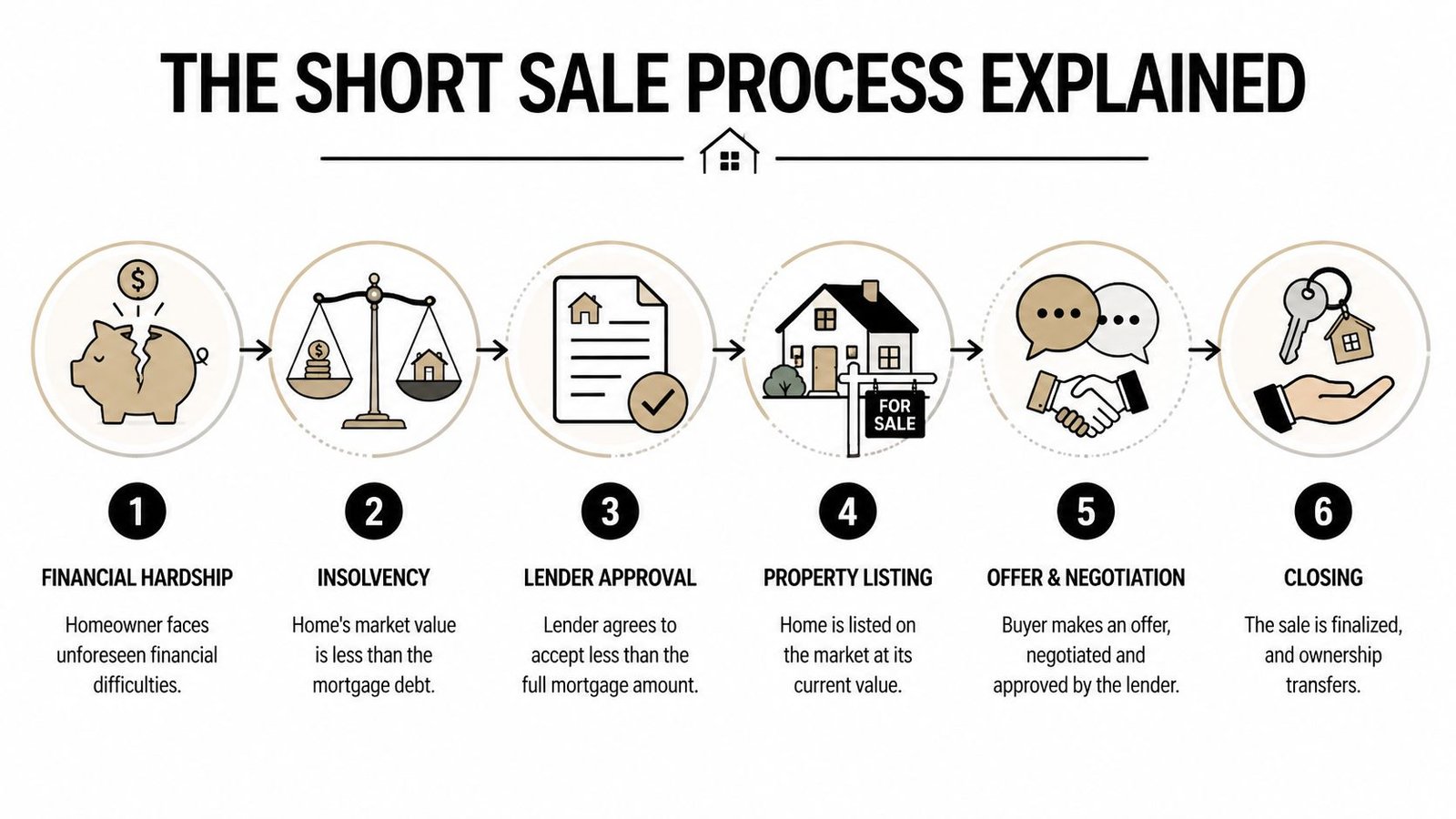

The process is easier to understand visually:

Why the bank would ever say yes

Homeowners often ask the wrong question here. They ask, "Why would a bank let me off the hook?" That's not how the bank sees it.

The bank is asking, "What's the least bad outcome?"

If they foreclose, they may take on delay, legal cost, maintenance issues, vacancy risk, resale hassle, and a lower sale price. If they approve a short sale, they may cut that loss earlier and move on.

Banks don't approve short sales because they're being generous. They approve them when the short sale looks better than the foreclosure file on the desk beside it.

That doesn't mean approval is easy. The lender still wants to verify the property value, review the buyer's offer, and decide whether accepting less now beats chasing the collateral later.

A quick explainer can help if you want to see the moving parts in action.

The actual sequence on the ground

Here's how it usually unfolds in real life:

- Step one: You or your agent contact the lender's loss mitigation department.

- Step two: You submit the hardship package and authorization forms.

- Step three: The property gets listed or marketed.

- Step four: A buyer makes an offer.

- Step five: The lender reviews that offer and orders a value check such as a Broker Price Opinion or appraisal.

- Step six: The lender negotiates, approves, counters, or rejects.

- Step seven: If everyone signs off, closing happens.

Some files move. Some crawl. Some die after months of effort.

What homeowners underestimate

Most sellers underestimate three things.

Lender control

You may own the house, but in a short sale, the lender controls the final yes or no. If there are multiple liens, the process gets harder because more than one party may need to agree.

Buyer fatigue

Buyers don't love uncertainty. If they have to wait months for approval, they may walk and buy another property.

The emotional drag

A short sale is not just paperwork. It's repeated document requests, delayed answers, and the stress of waiting while foreclosure risk may still hang over the property.

If you're already overwhelmed, choose your path based on how much uncertainty you can realistically handle, not on what sounds best in theory.

Short Sale vs Other Distressed Sale Options

When you're in trouble with a house, the worst move is drifting into default without choosing a strategy. You need to compare your options side by side, not emotionally.

A short sale is one path. It isn't the only one. In Cumberland County, the decision is usually between short sale, foreclosure, deed-in-lieu, or direct cash sale.

The direct comparison that matters

| Option | Timeline | Credit Impact | Seller Effort | Outcome Certainty |

|---|---|---|---|---|

| Short sale | Usually slow and lender-driven | Less severe than foreclosure | High | Uncertain |

| Foreclosure | Court and lender timeline | Most damaging of these options | Low day-to-day control, high long-term consequences | Certain if you don't intervene |

| Deed-in-lieu | Can be simpler than foreclosure in the right case | Negative, but often cleaner than foreclosure fight | Moderate | Depends on lender acceptance |

| Cash sale | Fast if title issues are manageable | Depends on whether loan can be paid off or separately resolved | Low | High if buyer is real and funds are available |

That table is the snapshot. The choice gets clearer when you look at each one carefully.

Short sale compared to foreclosure

A short sale usually beats foreclosure on financial fallout.

The strongest hard data on that point comes from the Philadelphia Fed analysis of short sales and foreclosures, which found that short sales sold for 9.2% to 10.5% higher prices than foreclosures and caused 1 percentage point less decline in neighboring property values. That same analysis notes the credit impact is milder than foreclosure.

That's the good news.

The bad news is a short sale asks more from you. You still have to maintain the property, respond to agents or buyers, gather lender documents, and wait on a bank that may reject the offer. Foreclosure is more damaging, but it can also feel deceptively passive because the bank drives it once the file gets rolling. Passive is not the same as safe.

If you want a breakdown focused on this exact decision, this guide on the difference between foreclosure and short sale is worth reading.

Deed-in-lieu compared to short sale

A deed-in-lieu of foreclosure means you give the property back to the lender instead of forcing them to foreclose.

This can work when there isn't a practical sale path and the lender wants the house back without the expense and delay of foreclosure. It's often cleaner on paper than a short sale because you don't need to market the property and wait for a buyer. But it's not automatic. Lenders may refuse it, especially if there are title issues, other liens, or occupancy complications.

A deed-in-lieu can make sense if the property won't sell easily and you're trying to end the situation with less chaos. It makes less sense if you still have a realistic sale option.

Cash sale compared to everything else

A direct cash sale is not the same thing as a short sale, but people confuse them all the time.

If the cash offer is enough to satisfy the debt, then it's just a sale. If the cash offer is not enough, then you still have a payoff gap and may need the lender's consent. The difference is practical. A serious local cash buyer may still give you a fast, clean baseline option so you can stop guessing and start making decisions.

Here is where I get opinionated. Certainty has value. If you're on a deadline, dealing with inherited title issues, handling bad tenants, or coordinating a move from another state, a guaranteed closing often matters more than trying to rescue every dollar from a distressed property.

How to choose based on your real priority

Use this filter instead of asking which option sounds best.

If your priority is credit damage

A short sale is often better than foreclosure based on the Philadelphia Fed findings above. That makes it worth exploring if you have enough time and enough cooperation from the lender.

If your priority is speed

Cash sale usually wins. Short sales can drag. Foreclosure timelines are not under your control. Deed-in-lieu depends on lender willingness.

If your priority is least paperwork

Foreclosure may require the least effort in the short run, but it creates the worst long-term fallout. That is a bad trade for most owners. A direct sale or deed-in-lieu is usually cleaner if available.

If your priority is certainty

Short sale is weak here. The lender can reject the package, counter the offer, or delay until the buyer walks. Foreclosure is certain in the worst way. Cash sale is usually the clearest route when the numbers work.

The right option isn't the one with the nicest label. It's the one that solves your problem before the problem gets bigger.

Short Sales for Fayetteville and Cumberland County Homeowners

Cumberland County isn't a generic housing market. A lot of homeowners here are dealing with military relocation, absentee ownership, rental problems, and time-sensitive decisions. That changes how a short sale works in practice.

A textbook short sale assumes you can wait, coordinate documents, keep the home accessible, and survive months of lender review. A Fayetteville owner facing PCS orders often can't do any of that comfortably.

Why PCS changes the whole decision

If you're military and you've been ordered to move, the biggest issue usually isn't just value. It's logistics.

You're trying to coordinate travel, family needs, command timelines, and housing on the next assignment. A normal sale is already disruptive. A short sale adds lender approval on top of that. According to Better's discussion of short sales for military families, military-specific short sales can average 4 to 8 months because of VA or USAA delays and out-of-state coordination, and 40% of attempts in North Carolina data fail due to lender rejection.

That number matters because it tells you something blunt. You can do everything right and still not get to the finish line.

The absentee owner problem

A lot of owners in Fayetteville and Fort Bragg's orbit no longer live here by the time the problem gets serious.

They're in another state. Sometimes another country. The house has a tenant who stopped paying, a family member living there without structure, deferred repairs, or a code issue that started small and became expensive. In those cases, a short sale becomes harder because the file needs active management.

Common obstacles for out-of-state owners include:

- Access issues: Buyers and agents need entry. Tenants may resist.

- Condition problems: A lender may question value if the home has obvious damage.

- Document lag: Every missing bank statement or unsigned form slows approval.

- Local deadlines: Taxes, HOA pressure, or foreclosure notices don't pause because you're stationed elsewhere.

If that's your situation, read this practical guide on selling a house in foreclosure. It helps frame the urgency correctly.

Why local distress doesn't look the same for every seller

A homeowner in Hope Mills with a vacant inherited property has a different problem than a service member leaving Fort Bragg next month. But they share one thing. They need a solution that matches the clock.

That's why I don't give blanket advice like "always try a short sale first." That can be terrible advice in Cumberland County.

A short sale may fit when

- You have real lender runway

- The home is accessible and marketable

- You can supply paperwork quickly

- You're trying to avoid foreclosure and can tolerate delay

A short sale may be the wrong fit when

- PCS orders create a hard deadline

- The property is vacant, damaged, or tenant-occupied

- You're already out of state

- You need certainty more than negotiation

In Fayetteville, the best option is usually the one you can actually execute while life is moving around you.

My local take

For military families, timing usually beats optimism. For absentee owners, simplicity usually beats process. For landlords with a problem property, a complicated approval track can be the last thing you need.

A short sale isn't wrong. It's just often slower and shakier than homeowners expect. In a place with frequent relocations and a lot of long-distance ownership, that matters more than people admit.

Your Next Step Deciding What's Right for You

If you're still deciding, strip away the jargon and answer three questions.

How far behind are you? How fast do you need this resolved? How much uncertainty can you tolerate?

Those answers usually tell you more than any real estate term ever will.

If a short sale fits, move fast

A short sale can be a legitimate foreclosure alternative. But it only works when you start early enough, document hardship clearly, and accept that the lender controls approval.

That last part is the problem for many homeowners. Sacramento Appraisal Blog's 2025 market discussion of short sale activity notes that short sales remain just 0.5% of local sales in some markets, processing times have improved to 3 to 4 months, and in some areas only 1 in 3 short sale listings close successfully. That's not a reason to panic. It is a reason to stop assuming this is a quick, dependable exit.

If speed and certainty matter more, choose accordingly

If foreclosure pressure is rising, if you've already moved, or if the house needs work and you don't want months of showings and lender back-and-forth, don't force yourself into the wrong strategy. A guaranteed sale with a clear closing date is often the smarter business decision.

Here's the advice I give distressed owners locally:

- Don't wait for the bank to become easy to work with. It usually won't.

- Don't pick a path just because it sounds less painful. Choose the one you can finish.

- Don't confuse "possible" with "practical." A short sale may be possible and still be the wrong fit.

- Get a real option in hand quickly. You make better decisions when you know what a straightforward sale would look like.

Make the decision like an owner, not like a bystander

You don't need to solve every issue at once. You need to stop the slide and take the next useful step.

If you want more context on urgent mortgage situations, this resource on how to stop foreclosure on your home is a good place to start.

My opinion is simple. If you have time and a cooperative lender, explore the short sale. If you don't, stop chasing a process that may leave you worse off and choose the route that gives you a firm outcome.

Frequently Asked Questions About Short Sales

Do I get any money from a short sale?

Usually, no.

In a true short sale, the house sells for less than the loan payoff, so the proceeds go toward the debt and closing costs. The entire transaction exists because there isn't enough value to cover what's owed. Most sellers should assume they are not walking away with proceeds.

Does the bank have to approve the buyer's offer?

Yes.

That approval is the core feature of a short sale. You can list the house and attract a buyer, but you cannot complete the sale without lender consent if the sale price won't fully satisfy the mortgage. If there are additional liens, more than one party may need to approve.

Is a short sale better for my credit than foreclosure?

Generally, yes.

The clearest support for that point appears earlier in this article from the Philadelphia Fed analysis. The short version is that foreclosure tends to hit harder. If your goal is to reduce long-term damage, a short sale is often the better of those two distressed outcomes.

How long does a short sale take?

It depends on the lender, the paperwork, the buyer, and whether there are multiple liens.

In practice, homeowners should expect a process that can feel slow and unpredictable. Some files move faster than others, but you should not choose a short sale if your situation requires a guaranteed near-immediate closing.

What if the bank rejects the short sale?

Then the sale doesn't close on those terms.

At that point, the options usually become practical rather than theoretical. You may submit a different offer, provide more documentation, pursue another loss mitigation route, negotiate a deed-in-lieu, or look for a direct sale alternative. If foreclosure is already moving, the timeline can get tight quickly.

A rejected short sale doesn't just waste time. It can shrink your remaining options.

Can I do a short sale if I'm already behind on payments?

Possibly, yes.

In fact, many short sale cases begin because the owner is already behind or knows default is coming. What matters is whether the lender sees a credible hardship case and whether there's still enough time to process the file before foreclosure overtakes it.

Is a short sale a good idea for military families with PCS orders?

Sometimes, but not automatically.

If you have time, access to documents, and a lender that responds, a short sale may help you avoid foreclosure. If your move timeline is hard, your lender is slow, or the property is difficult to manage from out of state, the process can become more burden than benefit.

Can I sell my house as-is instead of trying to fix it for a short sale?

In many distressed situations, yes.

The question isn't whether the house is perfect. The question is whether the buyer, lender, and title path can all align. If the house needs heavy work, has occupancy issues, or can't handle listing prep, that often pushes sellers toward simpler sale options rather than a traditional market approach.

What's the smartest first move if I'm overwhelmed?

Get organized before you get desperate.

Start with:

- Your mortgage statement: Know the payoff picture.

- Any foreclosure notices: Deadlines matter.

- Basic financial records: If you explore a short sale, you'll need them.

- A realistic sale option: Find out what a direct, uncomplicated sale would look like so you can compare.

That last point matters most. Once you know your realistic options, the fear usually drops and the decision gets clearer.

If you need a straightforward way out, DIL Group Buyers offers local homeowners in Fayetteville, Hope Mills, Spring Lake, Raeford, and nearby areas a direct cash sale option without repairs, listings, or commissions. If you're dealing with foreclosure pressure, PCS relocation, bad tenants, liens, or an unwanted house from out of state, get a no-obligation offer and compare it against the short sale route before you commit to months of uncertainty.