A Notice of Default is the formal notice from your lender that officially starts the foreclosure process after your mortgage is seriously past due, often around 90 days behind. It’s serious, but it is not the end. It’s a warning window, and if you act quickly, you still have options.

If you're in Cumberland County, this usually doesn't feel like a legal concept. It feels like a certified letter on the counter, a missed call from your servicer, and a knot in your stomach because you already know money has been tight. Maybe you fell behind after a job loss. Maybe you're dealing with repairs, tenants, divorce, or a sudden move. Maybe you're stationed elsewhere now and the house in Fayetteville became a problem faster than you expected.

The biggest mistake I see is simple. People freeze.

That’s understandable. It’s also dangerous.

A Notice of Default tells you the lender has moved past reminders and late notices. They are now using the legal process to protect their interest in the property. Your job is to stop guessing, get clear on your timeline, and make a decision that protects your credit, your equity, and your peace of mind.

The Envelope No One Wants to Receive

That envelope usually arrives when life is already messy. You open it standing at the kitchen counter, skim a few words, and your eyes lock onto the ones that matter: default, cure, acceleration, foreclosure. Your brain jumps straight to losing the house.

That reaction is normal. But a Notice of Default is not a lock on the door and it’s not an eviction notice. It’s the lender’s formal notice that your mortgage is far enough behind that they are beginning foreclosure steps.

In plain English, this is the moment the problem becomes official.

A lot of homeowners in Fayetteville, Hope Mills, and Spring Lake wait too long because they think the lender will “work with them later.” Sometimes the servicer will. Sometimes they won’t. You cannot afford to build your plan around hope alone. If you want a deeper look at the chain of events, this guide on what happens when you default on mortgage is worth reading after this.

The broader picture matters too. In 2025, 227,360 consumers in the U.S. received a new foreclosure filing, up 30.6% from 174,100 in 2024, according to LendingTree’s U.S. mortgage market statistics. This isn’t rare bad luck. A lot of families are under pressure.

Practical rule: When you receive a Notice of Default, stop asking “How did this happen?” and start asking “What deadline am I facing, and what am I doing by tomorrow?”

That shift matters. Panic wastes time. Action creates options.

Decoding the Notice of Default Document

A Notice of Default is basically the lender’s final formal invoice before the foreclosure machinery starts moving. It is more serious than a late notice because it becomes part of the legal record.

You don't need to read it like a lawyer. You need to read it like someone protecting a deadline.

What to look for first

Start with the basics. Who sent it? Is it your servicer, a law firm, or another party acting for the lender? Then find the default amount, the cure instructions, and the deadline.

A proper Notice of Default is not supposed to be vague. Federal rules and state statutes require specific details, including the exact nature of the default, the actions needed to cure it, a firm deadline, and a warning that the full loan balance could be demanded through acceleration, as explained in Better’s notice of default guide.

That means your notice should tell you, clearly:

- What went wrong: The missed payments or arrears.

- What fixes it: The amount and action required to cure.

- When it must be fixed: The deadline.

- What happens next: The lender may accelerate the loan if you don’t cure.

- What rights you may still have: Including the ability to challenge errors.

Why the details matter

This document is regulated for a reason. Lenders don’t get to wing it.

If the notice contains mistakes, those mistakes can matter. I’m not telling you every typo kills a foreclosure. It doesn’t. But if the amount is wrong, the payment history is off, or required details are missing, that can affect your response strategy. That’s one reason homeowners should keep every statement, bank record, and servicer letter.

A Notice of Default is not just a threat. It’s also evidence.

One more term you'll hear later is lis pendens. That’s a separate public notice tied to foreclosure litigation and property title issues. If that term has started popping up in your paperwork search, this explanation of what is lis pendens notice will help you understand the difference.

What makes it different from a collection letter

A collection letter says you owe money. A Notice of Default says the lender is now invoking legal remedies tied to the mortgage.

That’s the key difference.

Treat it like a starting gun. Once it arrives, every day you delay makes the next option harder.

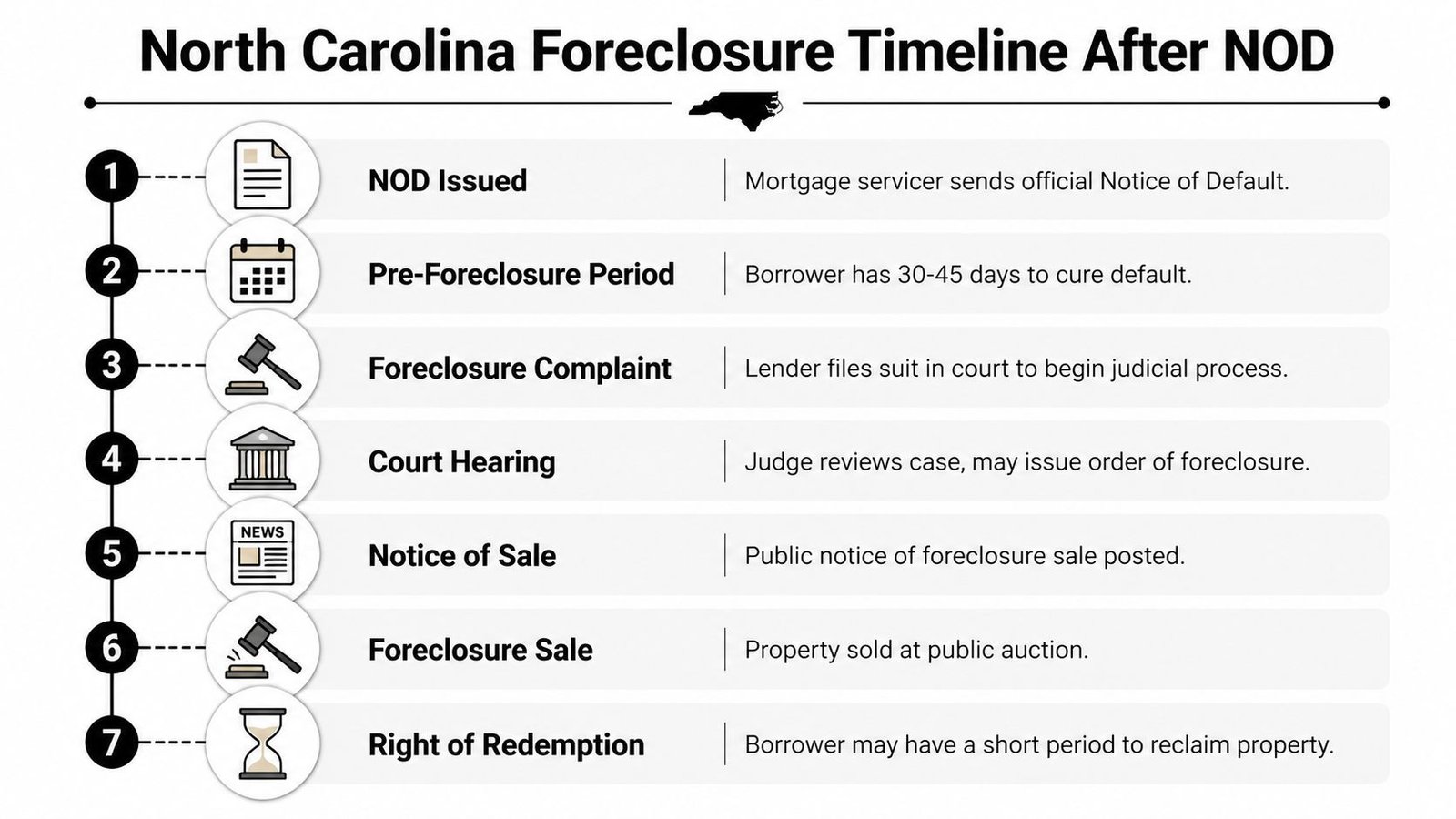

The North Carolina Foreclosure Timeline After a NOD

North Carolina gives homeowners a process. That’s the good news. The bad news is that the process still moves fast if you do nothing.

Once the Notice of Default period runs out, the lender can move toward a court hearing. Your timeline is not endless, and your credit is already under pressure from the missed payments that led here.

What happens after the notice

Here’s the plain version of the North Carolina sequence:

- You fall behind

- The lender sends the Notice of Default

- The cure period runs

- The lender files for a hearing

- The court reviews the foreclosure

- A sale is scheduled

- The property is sold if nothing stops it

The credit damage starts early

A lot of people think foreclosure ruins credit only at the sale stage. That’s not how it works. The damage starts with the serious delinquency itself.

The first 90-day delinquency can cause a FICO score drop of 85 to 160 points, and in North Carolina the lender files for a court hearing after the NOD cure period expires. If you don't act, the full process from NOD to a sheriff's sale can take as little as a few months, according to Corporate Finance Institute’s notice of default overview.

That’s why “I’ll deal with it next month” is not a plan.

A realistic local reading of the timeline

If you own in Cumberland County, don’t focus on the outer edge of how long a foreclosure could take. Focus on how quickly your good options shrink.

Your easiest window is usually right after the notice arrives. That’s when you still have the most flexibility to reinstate, negotiate, list, or sell directly. Once a hearing date is on the calendar, the pressure changes. Buyers get cautious, paperwork gets tighter, and your lender gets less patient.

Here’s a simple way to think about it:

| Stage | What it means for you | Best move |

|---|---|---|

| Notice received | You still control the most choices | Read the deadline and make calls immediately |

| Cure period running | You may still fix or resolve the default | Compare all options, not just one |

| Hearing filed | Legal pressure increases | Respond fast and get documents organized |

| Sale approaching | Time gets scarce | Choose certainty over delay |

If you're waiting for the “perfect” solution, you may miss the practical one.

What homeowners often misunderstand

People often believe the court hearing means they can explain everything and automatically get extra time. Sometimes you can raise real issues. But the court process is not a counseling session. It’s a legal step.

You need a concrete response before that stage. Money to reinstate. A workout approved by the servicer. A sale in motion. A bankruptcy filing if that’s appropriate. Something real.

Your Seven Options for Responding to a Default Notice

You have more than one option after a Notice of Default. That’s the good part. The hard part is that some options fit your situation and some don’t.

If your income problem is temporary, one route may work. If the house is vacant, damaged, or tied to a PCS move, another route makes more sense. Don’t force the wrong solution just because it sounds better emotionally.

Comparing your options

| Option | Time to Resolution | Credit Impact | Keeps Home? | Key Benefit |

|---|---|---|---|---|

| Reinstatement | Fast if you have funds ready | May limit further damage | Yes | Stops default by catching up |

| Loan modification | Slower, lender approval required | Delinquency still matters | Yes | Can make payment more manageable |

| Forbearance | Temporary relief | Depends on overall loan status | Usually | Buys short-term breathing room |

| Short sale | Moderate | Less damaging than completed foreclosure in many cases | No | Exit with lender approval |

| Deed-in-lieu | Moderate | Negative, but may avoid full foreclosure | No | Cleaner surrender path |

| Bankruptcy | Immediate legal pause, but complex | Major credit impact | Maybe | Can stop the sale temporarily |

| Sell to a local cash buyer | Fast | Can help avoid completed foreclosure | No | Speed and certainty |

If you want more foreclosure prevention strategies, this page on how to stop foreclosure on my home covers the broad playbook.

Option 1, reinstate the loan

If you can pay the arrears, fees, and required costs, reinstatement is the cleanest fix. You keep the house and stop the default process.

The catch is obvious. Those who receive a Notice of Default often don’t have a pile of extra cash sitting around. If family help, savings, or a retirement loan gives you a real path to reinstatement, move fast. This option gets weaker with delay.

Option 2, ask for a loan modification

A modification changes the loan terms so the payment is more manageable. This can help if the home is affordable long term but you hit a rough patch.

This route is paperwork-heavy. Expect requests for pay stubs, hardship letters, bank statements, and tax documents. If your income is unstable or the property is no longer practical for you, a modification can waste valuable time.

Option 3, request forbearance

Forbearance is a temporary pause or reduction. It can help when the hardship is short and you know how you’ll resume payments.

This is not forgiveness. It is a delay structure. If you don’t have a realistic catch-up plan, you’re just pushing the problem forward.

Best use: Forbearance works when your setback is temporary and documented, not when the house has become permanently unaffordable.

Option 4, pursue a short sale

A short sale means the lender agrees to let the property sell for less than what’s owed. This can be useful if the house won’t bring enough to cover the mortgage.

It’s often better than letting the foreclosure finish. But lender approval can drag, and traditional buyers frequently move too slowly for a distressed timeline.

Option 5, offer a deed-in-lieu

With a deed-in-lieu, you voluntarily transfer the property back to the lender. It can be cleaner than foreclosure, but lenders don’t always accept it.

This option usually works better when there aren’t title issues, junior liens, or occupancy complications. It also means giving up the property without testing whether a sale could produce a better outcome.

Option 6, file bankruptcy

Bankruptcy can trigger an automatic stay and stop the sale process for a period. For some families, that breathing room matters.

But let’s be direct. Bankruptcy is not a casual foreclosure tool. It’s a major financial decision with serious consequences. If you're considering it, you need legal advice from a qualified bankruptcy attorney, not guesses from the internet.

Option 7, sell the house quickly for cash

For many distressed owners, this is the most practical move. Not the most emotional. The most practical.

A fast sale can help you avoid the completed foreclosure, cut off ongoing missed payments, and move on without repairs, showings, or months of uncertainty. That matters if the property needs work, tenants have caused problems, or you're no longer even living in the area.

This option is especially strong when:

- You’ve already moved out: Managing from another city or state is slow and expensive.

- The house needs repairs: Retail buyers often want credits, inspections, and financing contingencies.

- Time is short: Certainty matters more than squeezing for top dollar.

- You want closure: Stress has a cost, even when no one puts it on paper.

If you can keep the house on sustainable terms, do that. If you can’t, sell before the process takes the decision away from you.

An Immediate Action Checklist for Homeowners

You do not need to solve the whole problem today. You do need to stop drifting.

Do these first

Open everything

Read the full notice, every page. Don’t leave certified mail unopened because you’re afraid of what it says. The deadline exists whether you read it or not.

Find the cure deadline

Circle it. Put it in your phone. Put it on paper. If you miss everything else, don’t miss the date.

Call a HUD-approved housing counselor

Free housing counseling can help you understand workout options, required paperwork, and lender communication. This is one of the smartest first calls you can make.

Gather your documents

Pull your mortgage statements, payment history, hardship explanation, bank statements, pay stubs, tax returns, and any letters from the servicer. Sloppy paperwork slows everything down.

Contact the servicer

Not to beg. To document. Tell them you received the notice and ask what options are available right now. Take notes, including names and dates.

Keep your response organized

Use one folder, paper or digital, for every foreclosure-related item. Keep copies of letters, screenshots of account pages, and a simple call log.

That one habit can save you from confusion later.

This short video can also help you settle your nerves and focus on the first steps instead of worst-case scenarios.

Decide the direction fast

Once you know the deadline and your finances, choose a lane:

- Keep the home if it’s affordable

- Negotiate temporary relief if the hardship is short

- Sell before foreclosure if the property no longer fits your life

Waiting for certainty usually creates worse options, not better ones.

That’s especially true when the property is vacant, inherited, damaged, tenant-occupied, or tied to a move.

Advice for Military Families and Out-of-State Owners

Fayetteville is not a generic housing market. Fort Bragg moves families in and out constantly, and that changes how mortgage trouble shows up.

For military families, the problem is often timing. You get PCS orders, the house doesn’t sell fast enough, and then a payment issue turns into a legal issue. Even if you have protections in other parts of military life, those protections don’t magically make an unwanted house easy to carry from another state.

If the home no longer fits your assignment, your budget, or your family’s location, stop treating it like a temporary inconvenience. It’s a financial liability until it’s resolved.

The absentee owner problem is worse than most guides admit

National articles often assume you live in the house and check the mailbox daily. A lot of Cumberland County owners don’t. They live in another county, another state, or overseas.

That creates a real danger. A 2024 analysis found that 23% of default notices sent to out-of-state addresses were delayed by over 10 days, which can eat up a big part of a cure window before the owner even knows there’s a problem, according to Rocket Mortgage’s mortgage default overview.

If you're out of state, do these things immediately:

- Confirm the lender has your correct mailing address

- Check whether notices are also available online through your servicer account

- Put a local contact in place if the house is vacant

- Choose solutions that can close remotely if time is tight

Why speed matters more for these owners

Military families and absentee owners often don’t have the luxury of slow solutions. Repeated showings, contractor coordination, and drawn-out negotiations are hard enough when you live nearby. They’re much worse when you're managing the house from a different ZIP code.

In these situations, fast and certain usually beats complicated and theoretical.

Answering Your Top Questions About Mortgage Default

Can I stop foreclosure after a Notice of Default?

Yes, sometimes. But “can” depends on whether you act while options still exist. Reinstatement, modification, forbearance, bankruptcy, or selling before the foreclosure finishes can all interrupt the path in different ways.

What doesn’t work is silence.

Does the Notice of Default itself ruin my credit?

The late payments already hurt you before the notice arrived. The notice signals that the problem is now formal and serious. If the foreclosure completes, the damage is usually worse than if you resolve the situation earlier through a sale or workout.

Will the sheriff remove me right away?

No. A Notice of Default is not immediate physical removal. It starts a legal process. That said, don’t confuse “not immediate” with “not urgent.” Those are very different things.

Should I wait for the lender to offer me a solution?

No. Call them, but don’t sit back and hope they lead the process in your best interest. The lender’s goal is to resolve the loan. Your goal is to protect yourself. Those goals overlap sometimes, but they are not the same.

If I’m already out of the house, should I still care?

Absolutely. You can still face financial consequences, credit damage, and a worsening title situation if you abandon the property emotionally before the process is over. A vacant house also tends to get more expensive, not less, because of maintenance, utilities, and risk.

What is a notice of default on mortgage in the simplest possible terms?

It’s the lender’s official legal notice that your mortgage is seriously behind and foreclosure has begun unless you cure the default or resolve the debt another way.

If that’s where you are right now, don’t chase perfect. Chase workable. A clean exit before foreclosure is often better than months of stress followed by less control and more damage.

If you're in Fayetteville, Hope Mills, Spring Lake, Raeford, Dunn, or nearby and need a fast, practical way out, DIL Group Buyers can help you sell your house as-is for cash on your timeline. That can be a strong option for homeowners facing foreclosure, military families dealing with PCS, and out-of-state owners who need a remote-friendly sale without repairs, listings, or drawn-out uncertainty.