You pull a box away from the garage wall, or open up a closet that’s been shut for months, and there it is. Dark spotting. A musty smell. Stained drywall. If you were already thinking about selling, your mind usually goes to the same place fast: Is this going to kill the deal?

That reaction is normal. Mold makes people nervous because it raises two problems at once. One is the house itself. The other is everything that comes with a sale, including disclosure, repairs, inspections, financing, and whether a buyer will bolt the second they hear the word.

In Cumberland County, this comes up more often than most owners expect. Mold isn’t some rare outlier. Approximately 47% of homes in the United States currently have mold growing on them, and fungal diseases caused by mold exposure lead to approximately 75,000 hospitalizations each year in the U.S., according to mold prevalence and health data compiled here. The point isn’t to alarm you. It’s to make clear that you’re not the only owner dealing with this.

Selling a house with mold problems is possible. The critical question is which path makes sense for your timeline, your budget, and your tolerance for risk.

You Found Mold Now What?

A lot of sellers make the same mistake in the first day or two. They panic, scrub it, paint over it, and hope they can make it disappear before anyone notices. That usually creates a worse problem later because now the visible evidence is disturbed, the moisture source may still be active, and you’ve made documentation harder.

Slow down before you spend money

The first thing to do is simple. Confirm what you’re looking at, where it is, and whether there are signs the issue goes beyond one visible patch. A little growth around a window after condensation season is a different situation from mold tied to a roof leak, crawl space moisture, plumbing failure, or long-term humidity.

The second thing is just as important. Don’t assume your only respectable option is to fix everything before you sell. Sometimes remediation is the smart move. Sometimes it isn’t. Owners get into trouble when they start spending before they understand how the sale itself will be affected.

Practical rule: Treat mold as both a property condition issue and a transaction issue. If you only focus on cleanup, you can still get blindsided later by disclosure, financing, or buyer hesitation.

What usually matters most

In the Fayetteville area, the sellers under the most pressure tend to care about one of three things:

- Speed: You’re relocating, dealing with an inherited property, or you need the sale done without months of back-and-forth.

- Cash exposure: You don’t want to pour money into a house before you know whether you’ll get it back.

- Certainty: You want to know the deal will close, not die during inspection or loan underwriting.

Mold affects all three. It can stretch a normal sale into a grind. It can force repair decisions you didn’t plan for. And it can scare off buyers who loved the house five minutes earlier.

Don’t make the decision emotionally

You don’t need to solve the whole problem today. You need to get organized. Figure out the scope. Understand what North Carolina requires you to disclose. Then compare the two real paths in front of you: remediate and list, or sell as-is and let the next buyer take it on.

That’s how owners make clear decisions instead of expensive ones.

First Steps Assessing the Mold Damage

A seller in Cumberland County usually reaches this point after finding a dark patch behind a bathroom vanity, smelling something musty in the crawl space, or seeing stains come back after repainting. The mistake is treating every mold problem like a simple cleanup job. Before you spend money, figure out whether you have a surface issue, a hidden moisture issue, or a house that will keep raising red flags with buyers even after repairs.

Start with a seller's triage, not a contractor shopping spree

Walk the house slowly with your phone and a notepad. Take photos. Write down where you see staining, peeling paint, warped trim, soft drywall, mildew smell, or signs of past leaks. Sellers who skip this step often pay for testing before they understand the problem, or they spend on cleanup in one room and find out later the underlying issue was in the attic, crawl space, or behind the walls.

Pay closest attention to the areas that usually expose the pattern:

- Bathrooms and laundry areas: around tubs, toilets, exhaust fans, supply lines, washer hookups, and baseboards

- Windows and exterior walls: recurring condensation, bubbling paint, dark spotting, soft drywall

- Attics and crawl spaces: roof leaks, bad ventilation, wet insulation, damp framing

- Under sinks, utility rooms, and around HVAC equipment: slow plumbing leaks and condensation problems often start here

Visible mold already answers one question. There is a condition issue. The harder question is whether the problem is isolated or tied to a larger moisture source that could affect repairs, buyer confidence, and financing.

What a limited mold issue usually looks like

A small patch in one area can stay a small problem if the source is obvious and already fixed. For example, an old supply line leak under a sink that stained one cabinet wall is a different situation from recurring mold on multiple exterior walls.

The warning sign is recurrence.

If the same smell or staining keeps coming back, the house probably has an active moisture problem, poor ventilation, hidden water intrusion, or materials that are already compromised. At that point, the cheap fix often turns into the expensive one because you pay for cleanup first and diagnosis second.

When professional help makes sense

Bring in a qualified mold inspector or remediation contractor when the source is unclear, the house has a history of leaks or flooding, or the damage may be inside walls, subflooring, insulation, or ductwork. This matters even more if you are considering the repair-and-list route, because buyers will ask questions and their inspector will do the same.

A solid inspection should do more than confirm what your eyes already see. It should help identify where the moisture came from, whether it is still active, and how far the damage may extend. In houses headed for the open market, that paper trail can help. It can also reveal that the job is larger, slower, and less predictable than the seller expected.

Here’s a quick visual overview of what that process can look like:

What not to do during assessment

A few mistakes create extra cost fast:

- Do not open walls just to see what is there. You can spread contamination and create a bigger repair bill before you have a plan.

- Do not paint over stains or scrub everything before documenting it. You may destroy evidence that helps explain the scope and cause.

- Do not throw away old invoices, leak reports, or contractor notes. That paperwork matters if you remediate, disclose the issue, or compare your options.

- Do not assume an inspection automatically means you should repair and list. Sometimes the inspection confirms that an as-is home sale process gives you a cleaner exit with less cash risk.

The practical goal of this step

You are trying to answer three questions:

- How far does the problem likely go?

- Is the moisture source active, old, or still unknown?

- Will estimates and repairs put you in a stronger selling position, or just sink more money into a house that will still face stigma, inspection pushback, and buyer loan issues?

That last question matters more than sellers expect. In Fayetteville, some owners spend weeks getting mold assessed because they assume that is the first step toward listing. Sometimes it is. Sometimes the inspection is what shows them the traditional path will be slower, riskier, and more expensive than taking a certain cash offer and being done with it.

Your Legal Duties Mold Disclosure in North Carolina

North Carolina confuses a lot of sellers because people hear the phrase buyer beware and assume that means the seller can stay quiet. That’s not how smart risk management works in a mold sale.

Known mold is the issue that matters

If you know there’s mold, signs of mold, past remediation, or an underlying moisture problem tied to mold risk, you need to think in terms of material facts. A material fact is anything a reasonable buyer would care about because it affects value, safety, condition, or the decision to buy.

Mold usually falls into that category. Not because every spot is catastrophic, but because buyers, inspectors, lenders, and insurers all view it as important.

How disclosure works in practice

In a standard North Carolina sale, you’ll deal with a property disclosure form that asks about the condition of the home. Sellers often get stuck on whether to answer yes, no, or no representation. The mistake is treating those choices like a game.

If you know about a defect and try to hide behind vague wording, you increase your risk. If you don’t know, that’s different. But once you’ve seen mold, cleaned mold, hired someone for mold, or dealt with the leak that caused it, you’re in known territory.

A practical way to view it:

- Known current issue: Disclose it plainly.

- Past issue that was addressed: Disclose the history and keep the paperwork.

- Suspected issue without certainty: Don’t guess. Describe what you know, such as leak history, musty odor, or prior moisture intrusion.

Why concealment backfires

Most sellers don’t get in trouble because mold existed. They get in trouble because the buyer believes they knew and hid it. A buyer who discovers concealed mold after closing may involve an attorney, especially if the house had fresh paint over damaged drywall, recent patchwork in a problem area, or contradictory statements in the contract file.

You can sell a house with defects. You can't safely sell a house after misleading the buyer about defects you knew about.

That’s one reason some owners choose a simpler route and look into what selling a house as-is means in North Carolina. Selling as-is does not erase disclosure duties. It only means you’re not agreeing to make repairs. You still need to be honest about known conditions.

Keep a paper trail

If mold has been part of the home’s history, save anything that helps tell the story clearly:

- Photos: Before cleanup, during repairs, and after remediation

- Invoices: Plumbing, roofing, HVAC, remediation, demolition, and drying work

- Reports: Inspections, moisture findings, air sampling, and clearance documents

- Communication: Emails or notes showing what was found and what was done

This protects you in two ways. First, it helps the buyer understand the issue. Second, it protects you if anyone later claims you failed to disclose what you knew.

A plain-English rule for Cumberland County sellers

If you’d want to know about it before buying the house yourself, disclose it. If a moisture event happened and could matter to a future owner, disclose that too. The cleaner and more direct you are, the lower your legal risk tends to be.

That approach doesn’t guarantee every buyer will be comfortable. It does put you on much stronger footing when you move to contract.

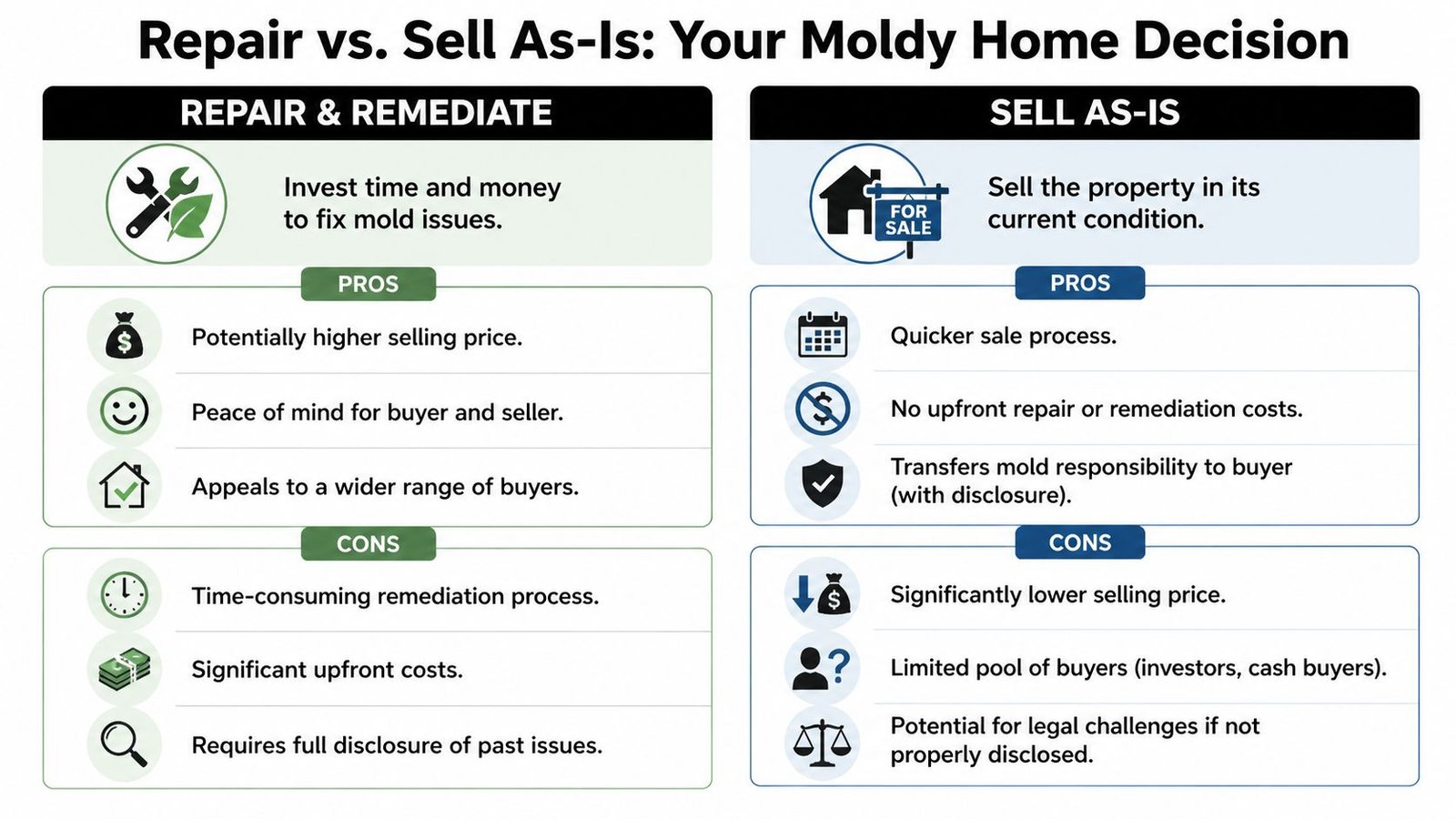

The Big Decision Repair and Remediate or Sell As-Is

This is the point where Cumberland County sellers decide whether they are paying for a cleaner sale or paying for more uncertainty.

A lot of owners assume the responsible move is to remediate, list the house, and make the money back at closing. Sometimes that works. Sometimes it turns into weeks of contractor coordination, surprise repair invoices, buyer skepticism, and a final sale price that still reflects the home's mold history.

What the repair path really asks from you

Proper remediation is a real project. It usually means isolating the work area, removing affected materials, drying the space, fixing the moisture source, cleaning thoroughly, and getting documentation that shows the work was completed correctly.

That takes money. It also takes discipline.

According to Angi's overview of mold-related value loss and remediation costs, remediation costs can range from a modest cleanup bill to major five-figure work when damage spreads into framing, drywall, flooring, HVAC components, or multiple rooms. In my experience, the mold invoice is often only part of the story. Roof leaks, plumbing failures, drainage problems, crawl space moisture, and interior rebuild costs are what push the budget off course.

The costs sellers do not see at first

The repair bill is the obvious cost. The hidden costs are what catch people off guard.

Stigma can stay after the work is done

A clean report helps. It does not erase buyer concern.

Once mold becomes part of the property's history, many buyers treat the house differently than a comparable home with no such history. They ask more questions. They scrutinize repairs. Some walk before they even schedule a showing. Others stay interested, then use that history to justify a lower offer.

That matters because you can spend real money on remediation and still sell into a discounted buyer mindset.

Financing can still become a problem

This is a major trade-off with the traditional route. A financed buyer brings in more people who can slow or derail the deal. The buyer's inspector, the appraiser, the lender, and sometimes the insurance side all have a chance to react to visible damage, prior moisture issues, replaced materials, or incomplete documentation.

Even when the mold is gone, the transaction may still feel unsettled to the financing side. That creates delays, repair requests, or a loan denial after you've already spent money getting the house ready.

Timelines get harder to control

Repair and list sounds straightforward on paper. In practice, the schedule depends on contractor availability, drying time, follow-up work, listing prep, showings, inspection results, buyer financing, and renegotiation. One delay tends to push the next one.

Sellers dealing with inherited houses, job transfers, divorce, probate, or mortgage pressure usually do not have much appetite for that kind of timeline risk.

Cheap remediation can become expensive remediation

If the root moisture problem is not fixed, the sale can circle right back to the same issue. A low bid may cover cleaning and surface treatment but miss the drainage correction, leak repair, crawl space work, or ventilation problem that caused the mold in the first place.

That is how sellers end up paying once for cleanup and again for a buyer concession.

Hard truth: Spending money on remediation does not guarantee a retail-price sale, and it does not guarantee a smooth closing.

When repair and listing can still make sense

There are cases where repairing first is the better play:

- The affected area is limited and clearly identified

- The moisture source has already been fixed

- The rest of the house shows well enough to compete on the open market

- You have cash available for remediation, repairs, and holding costs

- You can tolerate the chance of delays, credits, or a failed contract

If those boxes are checked, listing after remediation may produce a stronger top-line price. Just be honest about the trade-off. Higher price potential on paper does not always mean more money in your pocket after repairs, carrying costs, and concessions.

What selling as-is actually gives you

Selling as-is means the buyer accepts the property in its current condition, with full knowledge of known issues and without expecting you to complete repairs before closing. For the right seller, that is not a last-ditch move. It is a way to cap the risk.

Cash buyers and investors usually look at a mold house differently. They are not buying with the expectation that the home must satisfy a retail lender's property standards on day one. They are pricing the work, the risk, and the timeline upfront. That often leads to a simpler decision and a more predictable closing.

If the mold problem started with a leak, drainage failure, roof issue, or crawl space moisture, it helps to read how buyers evaluate selling a house with water damage, because those issues often show up together.

The real trade-off

Here is the clean version.

Repair and list if you want to test the retail market and you have enough time, cash, and patience to handle the process.

Sell as-is if your priority is certainty. That usually means no repair budget, fewer moving parts, no lender waiting to approve the condition, and a closing timeline that is easier to predict.

A cash offer is not always the highest number on the first line. It is often the clearest number on the last line.

Side-by-side comparison

| Factor | Repair & List on MLS | Sell As-Is to Cash Buyer |

|---|---|---|

| Upfront cost | Seller usually pays for remediation, repairs, cleaning, and listing prep | Seller avoids doing the work before closing |

| Disclosure burden | Full disclosure still applies, including prior mold issues | Full disclosure still applies |

| Buyer pool | Larger pool, but many buyers hesitate once mold history comes up | Smaller pool, usually buyers already comfortable with property problems |

| Financing risk | Higher, because buyer approval depends on lender and appraisal | Lower, because cash buyers do not rely on mortgage approval |

| Timeline | Harder to predict due to contractors, showings, inspections, and underwriting | More predictable if title is clear and the buyer is ready |

| Price potential | May be higher if the market accepts the remediation and the house shows well | Usually lower headline price because buyer is taking on repairs and risk |

| Stress level | More coordination, more opinions, more chances for renegotiation | Fewer parties involved and fewer repair disputes |

| Best fit | Seller has time, reserves, and a manageable problem | Seller wants speed, simplicity, and closing certainty |

The mistake that costs sellers the most

The roughest outcome is usually the half-measure. The seller spends enough to start fixing the problem, does not fully solve the source or document the work well, lists the house anyway, then gets hit with inspection concerns and late price cuts.

Run the numbers before you choose. Include remediation, related repairs, carrying costs, likely concessions, and the cost of a delayed closing. Once you compare the actual net outcome instead of the hoped-for list price, the better option usually becomes obvious.

Finding the Right Buyer and Closing the Deal

Once you’ve chosen your path, the actual sale process starts to separate the two options very quickly. On paper, a remediated listing may look straightforward. In the field, a mold history changes how buyers behave.

If you list the house traditionally

An MLS listing can work, but you need to expect friction. Buyers scroll through photos casually. They behave differently once they read disclosures, smell an issue in person, or hear their inspector mention microbial growth, excessive moisture, prior leaks, or replaced materials in a problem area.

Three things often happen in a traditional sale:

- The first buyer gets nervous during inspections. Even a motivated buyer can change tone once their inspector starts flagging moisture stains, attic growth, or prior remediation.

- The lender wants a cleaner file. If the property condition looks unsettled, the financing side may ask for more clarity or repairs.

- The deal gets renegotiated late. A buyer who already spent money on inspections may not walk immediately. Instead, they may ask for credits, price reductions, or additional work.

That’s one reason mold history can linger over the transaction even after the house is cleaned up. According to this discussion of mold stigma and sale speed, professionally remediated homes can sell 20% slower than comparable clean homes, while cash as-is sales can close up to 85% faster because they avoid financing hurdles and buyer hesitation tied to the home’s history.

What buyers really react to

Most buyers don’t evaluate mold like a contractor. They evaluate it like risk. They hear “past mold” and start wondering what’s behind the walls, whether insurance will be difficult, whether the smell will return in summer, and whether they’ll be stuck explaining the same history when they sell.

That doesn’t make them irrational. It just means a seller should not confuse “problem fixed” with “problem forgotten.”

A clean report helps. It doesn't erase fear, and fear is what kills a lot of traditional deals.

Why cash buyers are a different category

Cash buyers are not merely buyers with money in the bank. The important difference is that they usually underwrite the property themselves. They’re not asking a retail lender, an appraiser, and a nervous first-time buyer to all agree on the same house.

That changes the sale in practical ways:

- No repair precondition for loan approval

- No endless prep for showings

- No waiting on a buyer to decide whether the issue is emotionally tolerable

- No late-stage lender surprise

For sellers in Cumberland County, this matters when life is already moving fast. Military relocation, inherited homes, landlord fatigue, code issues, vacant properties, and out-of-state ownership all make uncertainty more expensive.

Matching the buyer to the problem

A house with a clean history and cosmetic updates belongs in front of retail buyers. A house with unresolved mold, leak history, or complicated inspection risk often performs better when matched to buyers who expect that kind of project.

That’s not settling. That’s positioning.

If you’re evaluating direct sale options, it helps to compare with local home buyers who purchase houses in any condition. The value in that route isn’t just speed. It’s the reduction in transaction risk.

Closing without the usual drama

No sale is completely automatic. Title still has to be clear enough to transfer. Probate issues, liens, and inherited ownership questions still have to be handled. But a direct cash sale usually strips away the most unpredictable part of selling a house with mold problems, which is the emotional and financial fragility of a financed retail buyer.

That’s why many experienced sellers stop asking only, “What price could I get?” and start asking, “Which path gives me the best chance of closing on terms I can live with?”

Those are not always the same answer.

Your Mold Sale Checklist and Local Fayetteville Resources

A mold sale usually goes sideways when the seller starts spending before a real plan is in place.

I see this in Fayetteville all the time. A seller pays for cleanup, then learns the leak source was never fixed. Or they remediate one area, list the house, and lose weeks when the buyer's inspector raises questions about the crawl space, attic, or past water intrusion. The issue is not just repair cost. It is the risk of spending money and still ending up with a delayed closing, a lower price, or a buyer who cannot get financing approved.

Use this checklist to decide your next move in the right order.

Your checklist

- Document what is there now: Take clear photos, note visible growth, staining, odors, soft drywall, warped trim, and any rooms with repeated moisture problems.

- Pin down the moisture source: Check for roof leaks, plumbing leaks, crawl space humidity, poor bathroom ventilation, HVAC condensation, grading problems, or older flood damage.

- Decide if you need an inspection or just contractor bids: If the mold is visible and the cause is obvious, estimates may be enough. If the house smells musty or the problem may be inside walls, under flooring, or above ceilings, a mold inspection can define the scope before a buyer does.

- Write out what you know for disclosure: Dates, leaks, repairs, contractor visits, and any areas where mold has appeared before.

- Get remediation quotes only if you are seriously considering the repair-and-list route: Ask what they remove, how they isolate the work area, how they dry the structure, and how they confirm the job is done.

- Price the full listing path, not just the mold work: Include cleanup, source repair, holding costs, extra mortgage payments, utilities, insurance, yard upkeep, and the chance of a price cut after inspection.

- Collect your paperwork: Invoices, roof or plumbing receipts, insurance claim records, mold reports, repair photos, and maintenance records.

- Choose the sale path based on certainty, not hope: A retail listing can make sense if the problem is fully resolved and the house still fits buyer expectations. An as-is cash sale often makes more sense when time, disclosure risk, financing issues, or repeated moisture history are hanging over the deal.

What proper remediation should include

Sellers do not need to become mold experts, but they do need to know what a serious contractor sounds like.

A real remediation plan should explain containment, removal of damaged materials where needed, drying, cleanup, and clearance steps. It should also address the moisture source. If a contractor mainly talks about spray, paint, or surface treatment, keep looking. That approach often leaves the underlying problem in place, and that is exactly what creates stigma later when buyers review the home's history.

The practical question is simple. If you spend the money, does that work make the house easier to finance and easier to close? Sometimes yes. Sometimes the house still carries a mold history that makes buyers cautious, especially if there are old leaks, crawl space concerns, or incomplete records.

Fayetteville-area practical resources

Use local help based on the actual bottleneck.

- Mold inspector: Best for hidden growth concerns, conflicting contractor opinions, or a house with odor but limited visible staining.

- Source repair contractor: Roofer, plumber, HVAC company, crawl space specialist, or drainage contractor. Mold is often the symptom, not the first problem.

- Closing attorney or real estate attorney: Useful when the sale also involves inherited property, title problems, liens, or questions about how to document known defects.

- Cash buyer familiar with problem properties: Useful when the bigger problem is uncertainty. Sellers in Cumberland County often choose this route when they do not want to fund repairs, manage showings, wait on lender approval, or risk a late-stage buyer exit.

The best local resource is the one that helps you make a clean decision early. That matters more than cosmetic prep on a house with a moisture history.

Frequently Asked Questions About Selling a House with Mold

Can I just paint over mold and sell the house?

No. Paint hides appearance. It doesn’t solve the moisture source or remove the underlying issue. If a buyer, inspector, or contractor later finds covered mold, you’ve increased the chance of a dispute because it can look like concealment rather than repair.

What if the buyer finds mold I didn't know about?

That happens. Many sellers first learn about attic, crawl space, or hidden wall issues during a buyer inspection. If that comes up, the deal usually shifts into negotiation. You may choose to remediate, offer a credit, reduce the price, or let the buyer walk and put the house back on the market with updated disclosure.

Should I get a mold inspection before listing?

Sometimes yes, sometimes no. If there’s visible mold and you already know the issue exists, testing may not change the basic decision. If there’s a musty smell, a history of leaks, or concern about hidden growth, an inspection can help define the scope before a buyer does it for you.

Will homeowner's insurance cover mold?

Sometimes, but not always. Coverage often depends on the cause of the loss and the policy language. Many owners are surprised to find mold itself isn’t broadly covered unless it resulted from another covered event. The safest move is to call your carrier and ask about your specific claim situation before assuming reimbursement.

Is selling as-is with mold legal?

Yes, if you disclose known facts. As-is describes the property condition and repair expectations. It does not erase your duty to tell the truth about known issues.

If you need certainty more than cleanup drama, DIL Group Buyers offers a direct cash option for Fayetteville-area homeowners dealing with mold, water damage, inherited houses, tenant issues, PCS moves, and other difficult situations. You can skip repairs, showings, and financing delays, get a straightforward offer, and choose a closing date that works for your timeline.