You may be sitting at the kitchen table right now, staring at a mortgage statement, a separation agreement draft, and a house neither of you can think clearly about anymore. One of you wants to keep the home. One of you wants out. Both of you are tired, and both of you are probably underestimating how dangerous it is to leave the mortgage unresolved.

Here’s the blunt truth. Your divorce can be final, and your mortgage can still be very much married.

That disconnect causes more damage than almost anything else in a divorce involving a house. The court can assign responsibility. The lender can ignore that assignment unless the loan is paid off, refinanced, or formally assumed. If your name is still on the note, you’re still on the hook. That’s the part too many people in Cumberland County learn after a missed payment, a denied loan application, or a surprise call from the servicer.

If you’ve been searching what happens to mortgage after divorce, the answer is simple in principle and messy in practice. You need to separate the legal divorce from the lender’s contract, decide quickly whether the home should be sold, refinanced, assumed, or temporarily left in both names, and protect your credit before emotion makes the decision for you.

Navigating the House and Mortgage in a Divorce

The house is usually the biggest asset, the biggest debt, and the biggest source of conflict. It also carries emotional weight that can cloud judgment fast. I’ve seen people fight to keep a home they can’t reasonably afford, and I’ve seen departing spouses sign over ownership thinking they’re safe, only to find out months later that the mortgage is still dragging behind them.

That’s why you need to treat the house as a financial file first and an emotional issue second. Hard advice, yes. Necessary advice, absolutely.

For many couples, the home decision comes down to four real-world questions:

- Who is legally responsible today: Check whose names are on the mortgage note, not just the deed.

- Who can afford the payment alone: Wanting the house and qualifying for the house are two different things.

- How fast do you need a resolution: Some Cumberland County families have court deadlines, school timing issues, or military relocation pressure.

- What choice creates the cleanest break: In divorce, clean often beats clever.

The safest outcome is not the one that looks best on paper. It’s the one that fully ends shared liability.

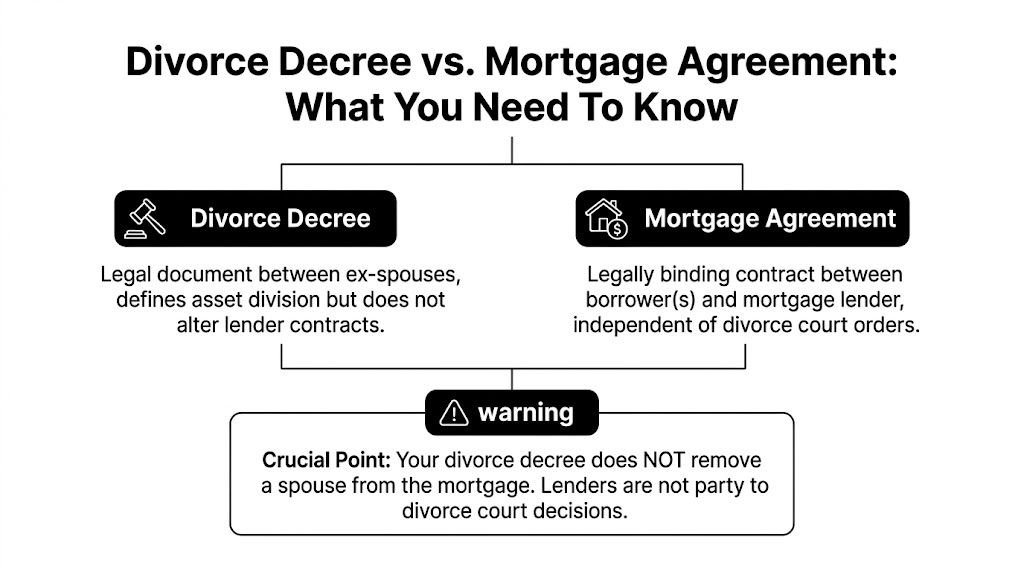

You also need to keep one central fact in view from the start. A divorce decree tells you and your ex what each of you must do. A mortgage agreement tells the lender who must pay. Those are separate tracks, and they do not automatically merge because a judge signed an order.

That’s where smart decisions begin. Not with who “deserves” the house. With who can carry the debt, who needs out, and what protects both credit files going forward.

Your Divorce Decree vs Your Mortgage Agreement

A divorce decree is a court order between former spouses. A mortgage is a contract with a lender. That distinction isn't technical fluff. It’s the whole game.

If you and your ex co-signed a car loan, and the divorce says your ex will take the car and make the payments, the lender still sees both borrowers until the loan is replaced or paid off. A house works the same way. The decree may assign responsibility, but the lender never agreed to rewrite its contract just because your marriage ended.

What a quitclaim deed does and doesn’t do

A quitclaim deed transfers ownership interest. It can move title from both spouses to one spouse. That matters for ownership. It does not remove either borrower from the mortgage debt.

If you're dealing with title transfer, review the practical steps in this guide on how to file a quitclaim deed. Just don't confuse that deed with lender release. They are not the same thing.

According to Scott J. Kalish's explanation of post-divorce refinancing and mortgage liability, transferring property title by quitclaim deed does not release either spouse from joint mortgage liability, and the Garn-St. Germain Depository Institutions Act of 1982 prevents a lender from enforcing a due-on-sale clause after a divorce-related transfer but does not waive liability. The same source notes that a single 30-day delinquency can drop a FICO score by 90-110 points.

What the lender still sees

The lender cares about one thing. Who signed the promissory note.

If both of you signed, then both of you remain liable unless one of these things happens:

- The mortgage is refinanced into one person’s name

- The mortgage is paid off through a sale

- The loan is formally assumed, if the loan program and servicer allow it

Practical rule: If your name is on the mortgage statement, your risk is still alive.

Moving out doesn’t change that. Signing over title doesn’t change that. A court order by itself doesn’t change that. If you leave a divorce with your name still attached to the mortgage, you have unfinished business with real financial consequences.

Four Common Ways to Settle the Marital Home

At the kitchen table, one spouse says, “I’ll keep the house.” The other hears, “Great, I’m free of it.” That is where people get hurt. Keeping the house and getting off the mortgage are two different outcomes, and your credit is on the line until the loan is dealt with.

You have four common options. Some preserve the house. Some protect your financial future. Those are not always the same thing.

Selling the home

For many Cumberland County couples, selling is the cleanest break.

A sale pays off the joint mortgage in full, turns the equity into real numbers, and ends the risk that one ex-spouse misses payments while the other keeps taking credit damage. If your top goal is to stop future liability, this option deserves serious attention first, not last. If you want a local overview, review this guide on how to sell a house during divorce.

Selling is not free. In Bankrate’s discussion of divorce and mortgage decisions, a home valued at $400,000 with $275,000 left on the mortgage would create about $125,000 in equity before sale costs, but realtor commissions of 5-6% plus average closing costs of $6,905 can eat up more than $30,000 of that equity. The same source also notes the Housing Affordability Index was 99.2 as of October 2023, which helps explain why many retaining spouses struggle to keep the home on one income.

Even so, a controlled loss from sale costs is often better than months or years of shared liability, refinancing delays, and damaged credit.

Refinancing into one spouse’s name

Refinancing works when one spouse wants the home and can qualify alone.

The lender will look at income, debts, credit, support obligations, and the full monthly housing cost. Sentiment does not matter. Past payment history as a couple does not matter much either. The question is simple. Can one borrower carry this house without stretching to the breaking point?

My advice is blunt. If the numbers are tight on paper, they will be worse in real life once repairs, utilities, taxes, insurance, and post-divorce legal expenses start hitting the account. Do not agree to a refinance timeline based on hope.

Mortgage assumption

Assumption is often the best option on paper if the current interest rate is far better than today’s rates.

One spouse takes over the existing loan instead of replacing it with a new one. That can preserve an affordable payment. It can also fail because the loan is not assumable, the servicer drags its feet, or the release of liability is not handled correctly.

This option is worth checking early. Get the servicer’s requirements in writing. If the assumption does not remove the departing spouse from the note, it does not solve the underlying problem.

Continued co-ownership for a period

This is the option people choose when they are trying to buy time.

Sometimes there is a reason. Children need stability for one school year. The house needs work before listing. One spouse expects a job change or support order that could improve qualification later. Those are understandable reasons. They do not reduce the risk.

Co-owning after divorce keeps both of you financially tied to the same property, the same payment history, and the same chance that one dispute turns into a late mortgage payment. I have seen this arrangement create more damage than any other option because it extends the marriage financially after the marriage is over.

If you do this anyway, set a hard sale or refinance deadline in writing, decide who has access to statements, decide who pays for repairs, and decide what happens if a payment is missed. Without that level of detail, this arrangement is a credit trap.

Which option fits which situation

- Sell the house: Best for couples who want a clean break, need to pay off the loan, or cannot support the home on one income.

- Refinance: Best for one spouse with strong income, solid credit, and enough margin in the budget to handle the full cost alone.

- Assume the loan: Best when the mortgage is assumable, the current rate is favorable, and the lender will fully release the departing spouse.

- Co-own temporarily: Best only for short, tightly managed situations with written deadlines and full transparency.

The biggest mistake is treating the home like an emotional asset instead of a financial obligation. Protect your credit first. In many divorces, that points straight to a sale.

Choosing Your Path Refinance Sale or Assumption

You don’t need a clever plan. You need the plan that solves the right problem.

If your top priority is ending all future liability, selling usually wins. If your top priority is staying in the home and you can qualify alone, refinancing may work. If the current loan has a strong rate and the servicer allows it, assumption deserves serious attention.

Comparing the main options

| Option | Speed | Financial Risk | Complexity | Best For |

|---|---|---|---|---|

| Sell the home | Often the clearest route once both parties agree | Low after closing because the mortgage is paid off | Moderate, especially if repairs or listing prep are needed | Couples who want a clean break and full payoff |

| Refinance | Depends on lender approval and documentation | Moderate to high if the new payment strains one income | High | One spouse with solid income, credit, and a realistic budget |

| Assume the mortgage | Depends on loan type and servicer process | Lower than refinance if the current rate is favorable and liability is formally released | High because servicer rules can be slow or inconsistent | Borrowers with an assumable loan who need to preserve the current terms |

Use this decision filter

Ask these questions in order, not all at once.

Can one person truly afford the home alone

This isn’t about scraping by for six months. It’s about carrying the payment, taxes, insurance, repairs, and the rest of life on one income. If the answer is shaky, don't force a refinance just to preserve sentiment.

Is the current mortgage worth trying to keep

If the loan has terms that would be hard to replace today, assumption may be worth the effort. But only if the servicer will process it and only if the departing spouse gets a real release from liability.

How much uncertainty can you tolerate

A sale gives finality. Refinancing and assumption can work, but they involve lender review, paperwork, timing, and the possibility of delay. If your life is already unstable because of divorce, less uncertainty has real value.

If you need speed, certainty, and a hard stop to shared debt, sale is usually the strongest choice.

A lot of people search what happens to mortgage after divorce because they want a rule. There isn't one rule. There is one priority, though. Protect your financial future first, then build the rest of the settlement around that.

The Hidden Dangers to Your Credit and Finances

The biggest mistake departing spouses make is thinking, “I moved out, so the risk is over.” It isn’t.

If your ex keeps the home but your name stays on the mortgage, one missed payment can hit both of you. The lender doesn’t care who was “supposed” to pay under the divorce order. It reports against the loan account. If you’re still a borrower, your credit can take the blow.

That matters because post-divorce life usually requires new financing. You may need another rental, another house, a vehicle, or even just cleaner credit to lower everyday borrowing costs. If the old mortgage is still attached to your credit profile, it can block your next move before you’re emotionally ready for another fight.

The affordability trap after divorce

The numbers are already stacked against recently divorced homeowners. According to Curran Moher Weis’s analysis of rising rates and divorcing homeowners, the homeownership rate for divorced individuals is 49.7% compared to 78.5% for married couples, and someone who locked in a 3% mortgage may now face a 7% rate, increasing the payment by $1,000 or more per month.

That’s one reason many people cannot keep the house after divorce, even when they want to. It also explains why dragging out a shaky refinance plan can do more harm than good.

If you’re already falling behind or worried that the mortgage will go unpaid, review the credit consequences in this guide on what happens when you default on a mortgage. It’s better to confront that risk early than pretend it won’t happen.

What this looks like in real life

A common scenario goes like this:

- One spouse moves out: They trust the other spouse to keep paying.

- Paperwork stalls: The refinance doesn’t happen on schedule.

- A payment gets missed: Both borrowers feel it on their credit.

- The departing spouse applies for new financing: The old mortgage still counts against them.

- Everything gets harder: Housing, transportation, and rebuilding after divorce all become more expensive.

This short video gives a useful overview of why mortgage issues after divorce can keep causing trouble long after the decree is signed.

You don’t protect your future by hoping your ex pays on time. You protect it by removing your liability.

That’s the standard you should use. Not optimism. Not verbal promises. Documented removal.

Your Practical Checklist for Protecting Your Finances

When emotions are high, a checklist beats memory. Use one and stick to it.

Before filing or early in the separation

Start by gathering facts. Not opinions. Not rough estimates.

- Pull the mortgage documents: Confirm who signed the note and who appears on the deed.

- Get a current mortgage statement: You need the payoff picture, not last year’s memory.

- Order a home valuation: Use an appraisal or another reliable valuation method your attorney can work with.

- Pull credit reports: Look for the mortgage, joint debts, and anything else that could become a negotiating advantage or liability.

- Make a housing budget: Build it on one income, not on wishful thinking.

During the divorce negotiation

Vague language causes expensive trouble later. Your agreement should be specific.

Put deadlines in writing

If one spouse will refinance or assume the loan, the agreement should include a firm deadline. If that deadline passes, the backup plan should already be stated, usually a sale.

Require document access

The spouse staying in the home should provide account visibility if both names remain on the mortgage for any period. That means statements, payment proof, and immediate notice of any servicing issue.

Don’t sign a settlement that says one spouse “will try” to refinance. “Try” is not a plan.

Coordinate your attorney and lender early

Don’t wait until the decree is entered to find out the lender won’t approve the chosen path. A practical conversation with the servicer or lender early can save months of conflict.

After the decree is signed

A decree is a milestone, not the finish line.

- Confirm title transfer: Make sure the deed matches the settlement.

- Verify mortgage resolution: Refinance, assumption, or payoff should be completed, not merely promised.

- Keep proof of release or payoff: Save every closing document and lender confirmation.

- Monitor your credit: Watch for reporting errors or signs the old mortgage still appears as active against you.

- Act fast on missed deadlines: If the other party doesn’t complete the required step, move to the backup remedy right away.

The strongest post-divorce move is almost always the one that reduces future contact around money.

A Clean Break Solution for Cumberland County Homeowners

In Cumberland County, mortgage problems after divorce get harder when real life piles on. PCS orders hit. Someone relocates out of state. One spouse is trying to manage the property from another city. The servicer asks for another document, then another, then stops communicating clearly. Meanwhile, the mortgage is still sitting there in both names.

That’s why I’m opinionated about clean breaks. They save people from slow-motion financial damage.

Why lender problems matter so much

A lot of divorce advice assumes the servicer will process everything smoothly. That’s not how it always works. According to the CFPB report on homeowners facing mortgage company problems after divorce or death, many homeowners deal with servicing problems such as delays in paperwork processing and refusals to release liability without a full refinance. The same source notes this is a common issue in Cumberland County, NC, and points out that mortgage assumptions can be an overlooked option for low-rate loans.

That’s useful to know. It also reinforces the larger point. The longer you stay entangled with the mortgage, the more room there is for delay, error, and conflict.

When a direct cash sale makes the most sense

A direct cash sale is often the cleanest answer when:

- Neither spouse can qualify alone

- The home needs repairs

- One or both spouses live out of state

- You’re on a short legal or relocation timeline

- You want to stop the joint liability quickly

This approach avoids the usual listing cycle, avoids repair negotiations, and avoids waiting on a retail buyer’s financing. For military families near Fayetteville and Fort Bragg, and for absentee owners who can't keep managing a house from afar, that certainty matters more than theoretical upside.

The best divorce housing outcome is often the one that ends the problem cleanly, not the one that keeps the house at all costs.

If assumption works, explore it. If refinancing is solid, pursue it. But if both of those paths are weak, stop trying to rescue a deal that no longer fits your life.

Conclusion Securing Your Financial Future Post-Divorce

The mortgage issue in divorce isn’t just about the house. It’s about your next five years.

If your name remains on the loan, you remain exposed. That’s true even if the divorce decree gives the house to your ex. The primary objective is a clean financial separation. Typically, that means one of three outcomes. Refinance the mortgage into one person’s name, complete a valid assumption with a real release of liability, or sell the property and pay the loan off.

What happens to mortgage after divorce depends on what action gets taken with the lender, not just what the court orders. That’s the distinction you can’t afford to miss.

Protect your credit. Insist on deadlines. Verify every document. And if the numbers no longer work, accept that quickly and move toward a solution that does. A difficult decision made early is usually cheaper than a bad decision stretched out over months.

If you need a fast, straightforward way to end mortgage liability after divorce in Fayetteville, Hope Mills, Spring Lake, Grays Creek, Eastover, Stedman, Raeford, Parkton, Dunn, or nearby areas, DIL Group Buyers can help. They buy houses as-is for cash, work with out-of-state owners and military families on tight timelines, and offer a direct path to settling the mortgage without listings, repairs, commissions, or financing delays. If your priority is a clean break and a clear next step, reaching out to DIL Group Buyers is a practical move.