TL;DR: A deed in lieu of foreclosure is when you voluntarily transfer the home back to the lender instead of going through a full foreclosure. In North Carolina, that can sometimes resolve the problem faster than waiting for the foreclosure process to play out. But it is not automatic, and lenders often reject deed in lieu requests, especially if the title is messy, there are other liens, or the lender believes another option could recover more money. For military families dealing with a PCS move or homeowners who need a firmer timeline, a direct cash sale is often more predictable and may do more to limit credit damage and stress.

You are at the kitchen table with a stack of mortgage letters, and every envelope feels heavier than the last. Maybe you are in Fayetteville trying to decide what to do before a move. Maybe you inherited a house in Cumberland County and just found out the loan is already behind. Maybe you ran into a stretch of months that did not go the way you planned.

That is usually when the phrase "deed in lieu of foreclosure" shows up.

The term sounds technical, but the basic idea is simple. You give the property back to the lender by agreement, and in return, the lender may agree not to push the case through a formal foreclosure. It works a bit like returning collateral to settle a debt, except a house brings more rules, more paperwork, and more chances for the lender to say no.

That last part matters. Many homeowners hear about a deed in lieu and assume it is a clean exit. In practice, it can be hard to get approved. North Carolina homeowners, including military families on a deadline, often need an option with fewer unknowns. If you are trying to stop foreclosure on your home in North Carolina, the best path is often the one you can complete on time, not the one that sounds best on paper.

If you are searching for what a deed in lieu of foreclosure means, you are probably really asking three practical questions. Will it stop the foreclosure process. How much will it hurt my credit. What happens if the lender refuses. Those are the questions that matter, and they are the ones to focus on before you choose your next step.

Facing Foreclosure in North Carolina You Have Options

A homeowner in Fayetteville might miss payments after a job change. A military family might get PCS orders and realize they can't sell fast enough. An out-of-state owner might inherit a house in Cumberland County and then learn the mortgage is already in trouble. Different stories, same pressure.

What usually happens next is confusion. One person says, "Ask for a loan modification." Another says, "Do a short sale." Someone else says, "Just let it foreclose." None of that helps if you need a practical answer this week.

The first step is slowing the panic

You still have options, even if the lender has already started sending serious notices. The key is to act before the timeline tightens and your choices narrow.

A deed in lieu of foreclosure is one option. It isn't the right fit for everyone, but it can be useful when keeping the home isn't realistic and you want to avoid the full foreclosure process. Other homeowners may be better served by a reinstatement, modification, short sale, or direct sale.

If you're in default, the worst move is usually silence. Lenders tend to respond better when the homeowner engages early and documents the hardship clearly.

What North Carolina homeowners often need most

Most distressed owners aren't asking for a perfect outcome. They're asking for one of these:

- More time: Enough breathing room to avoid a rushed mistake.

- Less damage: A path that reduces long-term fallout where possible.

- Clear next steps: Not legal jargon, just a sequence they can follow.

- A real exit plan: Especially if the house has repairs, liens, or a tenant problem.

If that's where you are, start by understanding your full set of choices. A good place to begin is this guide on how to stop foreclosure on my home, then compare that against whether a deed in lieu fits your situation.

What a Deed in Lieu of Foreclosure Actually Means

A deed in lieu of foreclosure means you voluntarily transfer the home back to the lender instead of waiting for the lender to take it through foreclosure.

The closest real-world comparison is returning a financed car before repossession. The idea is similar, but a house involves more paperwork, more lender review, and more risk if the agreement is not written carefully.

For a North Carolina homeowner, the practical meaning is simple. You are asking the lender to accept the property as part of a settlement for a loan you can no longer keep current. If the lender agrees, you sign the deed over. In return, the lender may stop the foreclosure process and may agree to release some or all of the mortgage debt.

That word "may" matters.

A deed in lieu is not the same as dropping off the keys and being done. It is a negotiated agreement, and the lender controls whether the offer is accepted. If there is a second mortgage, tax lien, judgment, HOA balance, title issue, or significant property damage, the lender may reject it because taking title creates extra problems for them.

What you are really trading

A deed in lieu works like a settlement exchange:

- You give up ownership of the property

- The lender avoids the time and cost of foreclosure

- Both sides try to reduce further loss

- The final paperwork states whether any remaining debt is forgiven

That last point is where homeowners often get hurt. If the agreement does not clearly say the lender is accepting the property in full satisfaction of the debt, you need to ask more questions before signing anything.

Military families in North Carolina run into this confusion often. A PCS move, deployment, or sudden relocation can make the house impossible to keep, especially if repairs are needed or the local market has shifted. Many service members hear that a deed in lieu will let them exit cleanly. Sometimes it does. Sometimes the lender says no after weeks of document requests, or approves it without fully waiving the balance.

Why lenders consider it, and why they still hesitate

From the lender's side, a deed in lieu can be simpler than foreclosure. They get control of the property sooner, and they avoid some of the delay that comes with a formal foreclosure case.

But lenders do not accept these requests just because the borrower is cooperative. They look at whether the title is clean, whether the house is vacant, whether junior liens exist, and whether they expect to recover more money through another option. If the property needs major work or has legal complications, a deed in lieu can be a harder sell than homeowners expect.

That is why a deed in lieu often sounds cleaner on paper than it feels in real life.

If you are weighing the practical difference between these outcomes, this guide on deed in lieu vs foreclosure in North Carolina can help clarify how much control you may still have.

The plain-English version

A deed in lieu of foreclosure is a voluntary handoff of the home to the lender, with terms that must be approved in writing. It can reduce the damage compared with a completed foreclosure, but it is not automatic, and it is not guaranteed to wipe out every debt tied to the property.

For homeowners who need certainty fast, especially military families on a deadline, that rejection risk is a big deal. A direct cash sale is often considered alongside a deed in lieu for exactly that reason. It can be faster, more predictable, and easier to finish before the lender timeline gets tighter.

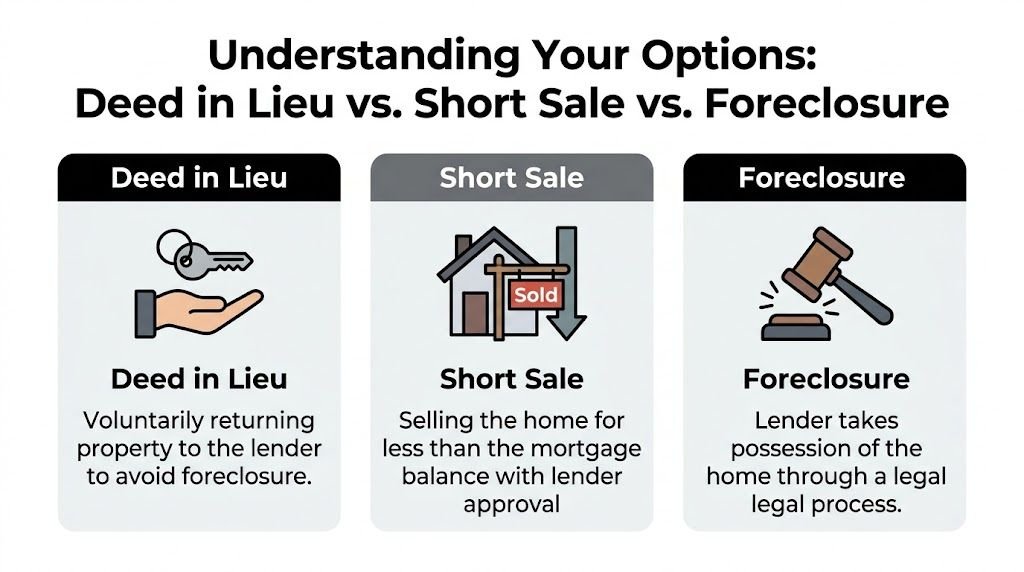

Deed in Lieu vs Short Sale vs Foreclosure

A North Carolina homeowner who is a month or two behind usually asks a practical question first. Which option gives me the best chance to protect my credit, finish on time, and avoid a worse mess?

That is the right question. A deed in lieu, a short sale, and a foreclosure can all end with you no longer owning the house, but they get there in very different ways. One is a negotiated handoff. One is a sale that still needs lender approval. One is the lender taking control through the legal process.

The quick comparison

| Factor | Deed in Lieu of Foreclosure | Short Sale | Foreclosure |

|---|---|---|---|

| Basic idea | You transfer the property to the lender by agreement | You sell the property for less than the loan balance, with lender approval | The lender takes the home through the legal process |

| Control | Some control, because you are still negotiating terms | Some control, but buyer and lender approval can slow or stop the deal | Very little control once the process is underway |

| Credit impact | Usually less harmful than a completed foreclosure | Negative, but often less severe than foreclosure | Usually the most damaging option |

| Future loan recovery | Recovery may be faster than after foreclosure, depending on the loan program and your full history | Depends on the loan type, lender rules, and how the account is reported | Recovery usually takes longer |

| Deficiency risk | May be waived, but only if the written agreement says so clearly | May be waived if the lender approves that term | Can still be an issue depending on the facts and documents |

| Public process | More private than foreclosure | Involves listing, buyer activity, and lender review | Formal legal process with public records |

| Timeline | Often shorter than foreclosure if approved | Unpredictable because you need both a buyer and lender approval | Usually the slowest and most rigid path |

Where each option helps, and where it breaks down

A deed in lieu can look attractive because it is direct. You and the lender are trying to solve one problem: transfer the property and settle the mortgage on agreed terms. If the lender says yes and the paperwork is written well, it can reduce the fallout compared with foreclosure.

Short sale sits in the middle. It gives you a chance to sell instead of handing the property back, which can feel more normal. But it often works like trying to close two deals at once. You need a real buyer, and you need the lender to approve the payoff. If either side stalls, the whole plan can drag out.

Foreclosure is the path with the least flexibility. Once it gets far enough along, your choices shrink fast. That loss of control is one reason many owners try hard to avoid it.

Why deed in lieu is not always the safest bet in real life

On paper, deed in lieu often sounds like the cleanest option. In practice, it has a major weakness. The lender can reject it.

That matters a lot for military families, out-of-state owners, or anyone facing PCS orders, a job transfer, or a hard deadline. You can spend weeks gathering documents, explaining hardship, and waiting for a decision, only to learn the lender wants a different route. By then, the foreclosure clock has not paused much, if at all.

Short sale has its own timing problem. Even if the lender is open to it, the house still has to attract a buyer. If the property needs repairs, has tenants, sits vacant, or is hard to show, that delay can become expensive.

How to compare them like a homeowner, not a lender

Ask four plain questions:

- How likely is this option to get approved?

- How much time do I have before the lender pushes ahead?

- Do I need the lender's written promise that the debt is fully settled?

- Can I handle repairs, showings, move-out deadlines, and paperwork?

Those questions often change the answer.

A deed in lieu may be better than foreclosure if the lender is cooperative and the title is clean. A short sale may be better if the house is marketable and you have enough time. But if certainty is the top priority, especially when credit damage and deadlines are colliding, a direct cash sale is often the more dependable path. You avoid the lender approval risk that can sink a deed in lieu and the buyer fallout that can sink a short sale.

A practical rule of thumb

Use deed in lieu if you want to try for a negotiated exit and your lender is willing to review it seriously.

Use short sale if the property can sell on the open market and you have time for buyer and lender approval.

Treat foreclosure as the outcome to avoid if possible.

For many North Carolina homeowners, especially military families who cannot afford delays, the actual comparison is not just deed in lieu versus foreclosure. It is whether either lender-controlled option is too uncertain compared with a faster as-is sale. If you want a more focused breakdown, this guide to deed in lieu vs foreclosure in North Carolina explains how the tradeoffs usually play out.

The Deed in Lieu Process and Eligibility Requirements

A deed in lieu is not a simple handover of the keys.

In North Carolina, it usually works more like an application file that the lender reviews line by line. You ask the lender to accept the property instead of continuing toward foreclosure, and the lender decides whether that solves its problem better than the other options on the table. For a homeowner under stress, especially a military family dealing with PCS orders, deployment timelines, or a move out of state, that review process can feel painfully slow.

What the process usually looks like

A typical deed in lieu file moves through several stages.

You contact the lender's loss mitigation department.

Ask whether the lender accepts deed in lieu requests at all. Some servicers list it as an option but still require you to complete their review process before they will say yes or no.You submit a hardship package.

This usually includes a hardship letter, recent income information, bank statements, monthly expense details, and the lender's own forms. The lender wants a clear explanation of why keeping the loan is no longer realistic.The lender reviews title and property condition.

The house is only part of the decision. The lender also looks for title problems, other liens, occupancy issues, and condition concerns that could make resale harder.The lender decides whether to offer terms.

If the file passes review, the lender may send a written agreement spelling out what you must do before transfer, including vacancy dates, condition expectations, and whether any debt will remain.You sign the deed and complete move-out.

After signing and recording, ownership transfers to the lender under the agreed terms.

That sounds orderly on paper. In real life, delays are common. Missing bank statements, a second lien that surfaces late, or a servicer that takes weeks to respond can stall the file at any stage. That uncertainty is one reason many North Carolina homeowners look at a direct cash sale instead. It gives you a defined closing path without waiting on a lender to approve every step.

The paperwork that matters most

One of the most misunderstood parts of a deed in lieu is the written agreement itself.

A good way to view it is this: the deed transfers the house, but the agreement controls the consequences. If that paperwork does not clearly say the mortgage debt is satisfied in full, you need to slow down and ask questions. Giving back the property does not automatically erase every financial obligation.

The estoppel affidavit is one document that often causes confusion. It is part of the lender's closing package and helps set out the agreed facts and terms. Homeowners often focus on the move-out date and miss the bigger issue, whether the lender is releasing the full debt or reserving the right to pursue a deficiency if allowed.

Important document: If the agreement does not clearly state what happens to the remaining loan balance, the biggest financial question in the deal may still be open.

Some lenders also require the home to be vacant, broom clean, and free of personal property by a set date. For military families, that timing can be hard to coordinate if orders change or housing on the next duty station is not ready yet.

Basic eligibility issues lenders look at

Lenders do not all use the same checklist, but several issues come up again and again:

- Documented hardship. Job loss, divorce, illness, relocation, reduced income, and payment increases are common examples.

- A clear title picture. Second mortgages, tax liens, HOA balances, and judgments can slow or block approval.

- A property the lender can resell without major trouble. Serious damage, problem tenants, or deferred maintenance may hurt your chances.

- A complete and responsive file. If documents are missing or the lender has to keep asking for updates, the request can lose momentum.

A simple analogy helps here. The lender is not just receiving a house. It is taking over everything attached to that house, including legal risks, title questions, and resale headaches. If the file looks messy, many lenders would rather keep the foreclosure process on track.

Where homeowners lose time

The biggest slowdowns are usually practical, not legal.

Incomplete forms, vague hardship letters, missing pay stubs, unresolved liens, and long response gaps can drag the process out. Waiting too long to apply is another common problem. If a sale date is getting close, the lender may not have enough time to review the request before foreclosure moves ahead.

That timing issue matters a lot in North Carolina. If your goal is credit protection and a definite exit date, a deed in lieu can be hard to rely on because approval is never guaranteed. A direct as-is cash sale is often more certain for homeowners who need speed, want to avoid repair demands, or cannot risk a lender-controlled process stretching past their deadline.

Hidden Risks and Why Lenders Often Say No

You send in the paperwork, explain the hardship, and wait for relief. Then the lender says no, even though handing over the home seems like the cleaner solution for everyone.

That feels backward at first. A deed in lieu sounds simple from the homeowner's side. From the lender's side, it works more like a risk filter. The lender is asking one business question: "Do we want this property, with all its title issues, condition problems, occupancy questions, and resale costs, right now?"

Approval is less predictable than many homeowners expect

As noted earlier, approval rates for deeds in lieu are much lower than many distressed homeowners assume. Even among borrowers who appear to qualify on paper, lenders approve only a small share.

That matters because a deed in lieu is not something you can count on until the lender gives written approval. If your foreclosure timeline is tight, uncertainty is a real risk, not a technical detail.

Why lenders reject these requests

A deed in lieu works best for the lender when the file is clean and the home is easy to take over and resell. Many North Carolina homeowners do not have that kind of file by the time they explore this option.

Common deal-breakers include:

- Other liens on the property. A second mortgage, HOA debt, tax claim, or judgment can stop the lender from accepting the deed.

- A home that needs too much work. Serious repairs, code violations, or deferred maintenance can make direct takeover less appealing.

- Occupancy complications. A tenant, family member, or holdover occupant can create delay and added legal expense.

- A hardship package that does not fully support the request. If the documents are inconsistent, outdated, or incomplete, the lender may decline instead of asking for more time.

A useful comparison is a used-car trade-in. If the title is clear, the car runs, and the paperwork is complete, the dealer can make a quick decision. If the car has a lien, body damage, and missing records, the dealer hesitates. Lenders look at deeds in lieu in much the same way.

Lenders approve deeds in lieu when taking the property looks safer, cheaper, and simpler than finishing the foreclosure process.

A risk military families should weigh carefully

This issue comes up often around Fayetteville and other military communities. A service member may need to relocate fast, manage the home from another state, and still protect future buying power.

A deed in lieu can affect the waiting period before using VA financing again. For a military family planning the next purchase after PCS orders, that timing can matter as much as the current mortgage problem. The short-term exit may solve one crisis while creating a later housing setback.

That is why military homeowners should look beyond "Can I get out of this house?" and ask "What does this choice do to my next move?"

Why rejection risk is a practical problem, not just a legal one

In North Carolina, a deed in lieu often breaks down over ordinary real-world issues. The house is not vacant yet. The title has an old lien. Repairs piled up after a deployment, job loss, or divorce. The lender asks for another document while the foreclosure clock keeps ticking.

For a stressed homeowner, that delay can be costly. You may spend weeks chasing an approval that never comes, only to end up closer to foreclosure with fewer backup options. That is one reason a direct cash sale is often more certain. If the buyer can purchase the property as-is, without lender discretion controlling the outcome, you have a clearer closing path and a better chance to limit further credit damage.

The practical takeaway

Before relying on a deed in lieu, ask yourself:

- Is there anything else recorded against the property besides the main mortgage?

- Can the home be delivered vacant if the lender requires that?

- Would the lender put any debt forgiveness in writing?

- If you are active-duty or recently relocated, how could this affect future VA financing?

- Do you have a backup plan if the lender says no or takes too long?

If those answers are unclear, treat a deed in lieu as one possible option, not the safe option. For many North Carolina homeowners, especially military families on a deadline, a direct as-is cash sale offers something a deed in lieu often does not. Certainty.

Deed in Lieu Rules for North Carolina Homeowners

North Carolina homeowners need to think locally, not just generally. The same option can play out differently depending on the state process, local court pace, and how your loan documents are written.

A deed in lieu is still a private agreement with the lender, but it exists in the shadow of North Carolina foreclosure law. That matters because the lender knows what its foreclosure alternative looks like here, and that affects negotiation.

Why North Carolina changes the conversation

North Carolina foreclosure practice often revolves around deeds of trust and formal procedures that can be difficult for a stressed homeowner to decode. That legal framework gives lenders a defined path if negotiations fail.

For the homeowner, that means timing matters. If you're waiting until every notice has piled up on the counter, the lender may be less flexible. If you're communicating early and keeping records organized, you may have more room to negotiate.

Issues local homeowners should review carefully

A North Carolina owner considering a deed in lieu should review:

- The exact mortgage and deed of trust documents

- Whether there are other recorded claims against the property

- Whether the house is vacant, occupied, or tenant-occupied

- Whether the lender's written agreement fully resolves the debt

North Carolina homeowners shouldn't rely on verbal promises in a distress sale situation. If a term matters, it needs to appear in the written agreement.

For Fayetteville and Cumberland County families

Military moves create unusual pressure. A family may already be leaving the area before the lender finishes reviewing documents. Absentee owners often have the same problem. They need a solution that doesn't depend on repeated trips, repairs, or endless back-and-forth.

Local homeowners should also be realistic about logistics. If the property has personal property left behind, deferred maintenance, or a problematic occupant, those issues can affect whether a deed in lieu is workable at all.

Get help before signing anything

If you're in Fayetteville, Hope Mills, or nearby parts of Cumberland County, it's wise to speak with a foreclosure attorney, legal aid resource, or HUD-approved housing counselor before signing a deed in lieu agreement. A short review of the paperwork can help you spot whether the deficiency language, possession date, and release terms protect you.

When the stakes are this high, clarity beats speed. But when speed matters too, you need to compare the lender route against other exit options right away.

A Faster Alternative to Protect Your Credit and Sell As-Is

A deed in lieu can work. The problem is uncertainty.

You can spend weeks gathering documents, explaining hardship, answering lender requests, and waiting for a decision that may still be no. If the property has liens, bad tenants, repair issues, or title complications, that uncertainty gets worse.

Why a direct sale appeals to many distressed owners

A direct cash sale solves a different problem than a deed in lieu. It doesn't ask the lender to take the property back. It gives the homeowner a way to sell quickly, avoid listing headaches, and move on with more control.

For many sellers, the appeal is practical:

- No lender approval gamble: You're not waiting to see if the bank accepts a voluntary transfer.

- No repairs: Distressed houses, inherited houses, and problem rentals can often be sold as-is.

- No showings or listing prep: That's a major relief for occupied or damaged homes.

- A closing date you can work with: That matters for military PCS moves and out-of-state owners.

Why certainty can matter more than theory

A deed in lieu may reduce credit damage compared with foreclosure, but it still requires lender cooperation and may still affect future borrowing. A direct sale may offer a cleaner path if the primary goal is to stop the spiral before it gets worse.

That is especially true for homeowners dealing with:

- Major repairs

- Code violations

- Liens

- Bad tenants

- Vacancy

- Inheritance complications

- Out-of-state ownership

In those situations, a homeowner often doesn't need a complex loss-mitigation file. They need an actual buyer.

A practical example

Take a homeowner who has already moved for work and left a Fayetteville property behind. The house needs work. Payments are behind. The lender wants documents, the property isn't in ideal condition, and there may be a second obstacle on title. A deed in lieu might still be possible, but every one of those facts raises rejection risk.

A direct as-is sale is often simpler. The owner gets an offer, picks a timeline, and exits without waiting for the lender to approve a special exception.

What to compare before choosing

If you're deciding between asking for a deed in lieu and selling directly, compare these points side by side:

- Certainty of outcome

- How fast you need to be done

- Whether the house needs repairs

- Whether title or occupancy issues exist

- How much more credit damage you can afford to risk

For homeowners who need speed and a cleaner exit, an as-is home sale option can be easier to execute than a lender-controlled process.

Frequently Asked Questions About Deeds in Lieu

What happens if I have a second mortgage or HOA lien

A deed in lieu usually works best when the lender would receive clean title. If a second mortgage, tax lien, HOA lien, or judgment is attached to the property, the first lender may refuse the transfer because it does not want to inherit someone else's claim.

That issue trips up a lot of North Carolina homeowners. It also affects military families who moved quickly after PCS orders and later discover an old HOA balance, a contractor lien, or another title problem still tied to the house.

Start by finding out exactly what is attached to the property. A deed in lieu can stall out for reasons that have nothing to do with your willingness to cooperate. Sometimes the more realistic path is a direct sale that deals with the title problems head-on.

Can I get a deed in lieu if my house needs major repairs

Possibly, but condition matters.

A lender reviewing a deed in lieu is deciding whether it wants the house back in its current state. A property with roof damage, water issues, code violations, stripped interiors, or unsafe conditions can look like a liability instead of a solution. The harder the home will be to resell, the more likely the lender is to reject the request or drag out the review.

A rough house does not automatically rule you out. It does mean you should avoid counting on lender approval until you have it in writing.

Will a deed in lieu stop foreclosure immediately

No. A deed in lieu request does not automatically freeze the foreclosure timeline.

It works more like submitting an application than pressing an emergency stop button. Until the lender approves the deal and the transfer documents are signed, the loan is still in default. Hearings, notices, and deadlines may keep moving.

Ask the lender, in writing, whether foreclosure activity will pause during review. If you need a certain closing date because of relocation, job transfer, or military orders, that uncertainty matters a lot.

Will I still owe money after a deed in lieu

You might.

The answer depends on the written agreement, not on a phone call or a general promise from a servicer. You want clear language stating that the lender accepts the property in full satisfaction of the debt, or that it is waiving any deficiency balance after the transfer.

A simple question can clear up a lot of confusion: "Does this agreement fully release me from any remaining mortgage debt after title transfers?" If the documents do not answer that directly, ask again before signing.

Are there tax consequences

There can be. If a lender forgives part of the mortgage debt, that forgiven amount may have tax consequences depending on your situation.

This is one of those areas where legal and financial language gets confusing fast. The transfer of the house may solve one problem while creating a tax issue later. A short review with a CPA or tax attorney can save you from an unpleasant surprise.

Can I do a deed in lieu if tenants still live in the property

Maybe, but tenant occupancy often makes approval harder.

Many lenders want the property delivered vacant before they will finalize a deed in lieu. If tenants are still in place, especially if they are behind on rent, damaging the property, or refusing access, the lender may decide the file is too complicated. For out-of-state owners and military families who cannot easily return to manage the property, that can become a major obstacle.

Ask early whether vacancy is required. If it is, be realistic about whether you can get the property empty in time.

Is a deed in lieu better for military families

Sometimes, but not always.

For military homeowners, the biggest question is often certainty. A deed in lieu may help avoid a completed foreclosure, but it still depends on lender approval, property condition, title status, vacancy, and timing. Those are real hurdles for a family dealing with PCS orders, deployment, or an unwanted rental left behind in Fayetteville or near Fort Liberty.

If your main goal is to protect your credit as much as possible, close on a known timeline, and sell the house as-is, a direct cash sale is often the more predictable option. That does not make a deed in lieu wrong. It means military families should compare the risk of lender rejection against the peace of mind of a sale they can schedule.

If you're in Fayetteville, Hope Mills, Spring Lake, Raeford, Dunn, or nearby North Carolina communities and need a fast, certain way out of a distressed property, DIL Group Buyers buys houses as-is for cash. They work with foreclosure situations, inherited homes, repairs, liens, bad tenants, military PCS moves, and out-of-state owners, and they let sellers choose a closing timeline that fits real life.