When you’re facing the threat of foreclosure in North Carolina, the most important thing to know is this: time is your greatest asset. Acting quickly and decisively is the key to stopping the process and keeping your home. The minute you even think you might miss a payment, that’s your cue to start exploring your options.

What To Do Immediately To Stop Foreclosure In North Carolina

Getting that first formal notice from your lender is a gut punch. It’s easy to feel overwhelmed, even paralyzed. But letting fear take over is the worst thing you can do right now. The most powerful moves you can make happen in the first 48 hours after you realize there’s a problem.

Don't wait for an official default notice to land in your mailbox. Being proactive is your best defense.

Your first phone call needs to be to your mortgage servicer. I know this is the call nobody wants to make. It’s easy to feel embarrassed or scared, but trust me on this: lenders are more willing to work with you than you’d expect. Foreclosure is a massive, expensive headache for them, too. They’d almost always rather find a solution that keeps you in your home and making payments.

Your First Call To The Lender

When you pick up the phone, you need a plan. Simply saying, "I can't pay" isn't enough. You need to have an honest, clear conversation about what's going on.

- Explain Your Hardship: Tell them exactly why you’re having trouble. Was it a sudden job loss? An unexpected medical bill? A divorce? Be specific.

- Have Your Documents Ready: Before you call, gather your recent pay stubs, bank statements, and a simple list of your monthly bills. This shows you’re serious and helps them see what you might qualify for.

- Ask for the "Loss Mitigation" Department: This is the team trained specifically for these situations. Using that term signals that you’ve done your homework and mean business.

Key Insight: Your lender isn't your enemy; they're a business. They want to avoid the massive costs and red tape of foreclosure. When you approach them with a clear story and the right paperwork, you make it easy for them to say "yes" to a solution like a temporary forbearance or a loan modification.

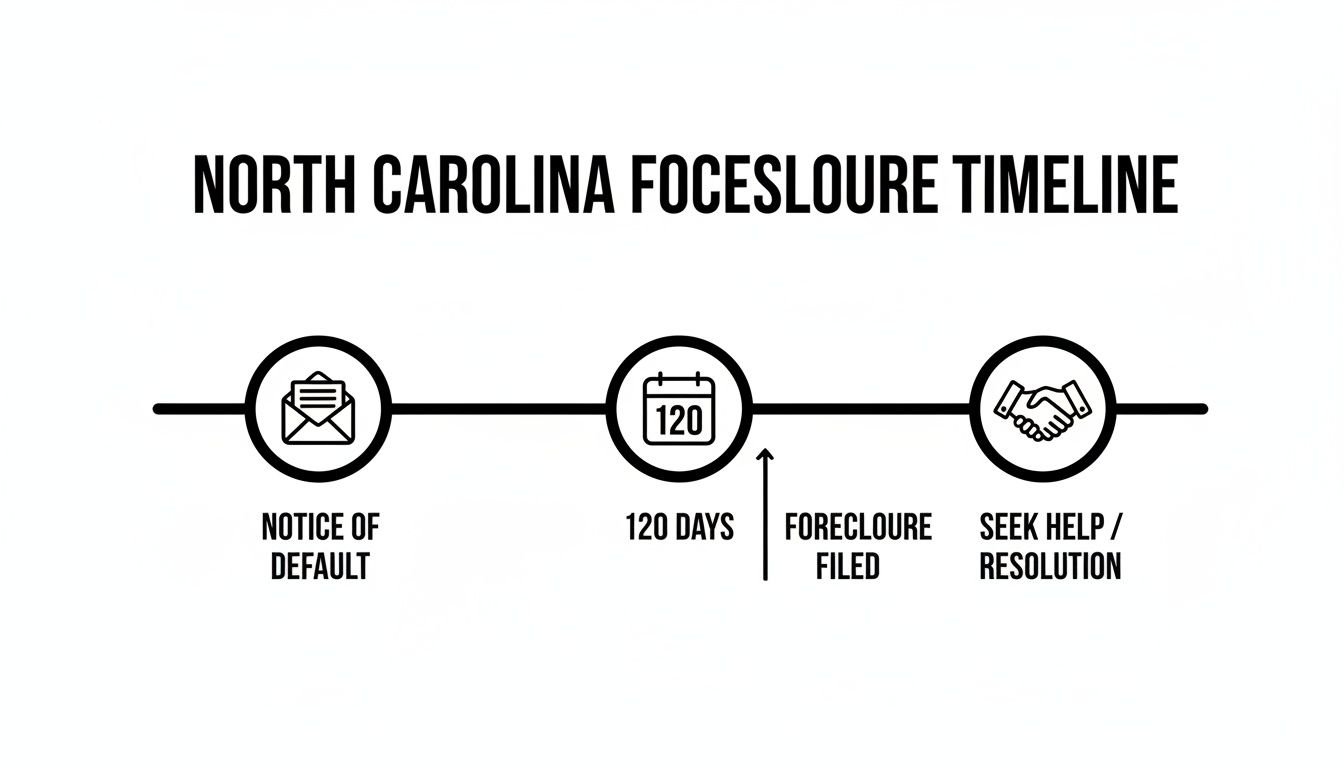

Understand North Carolina’s Protective Timeline

North Carolina law gives you a critical window of time to fight back. Once you get a "Notice of Default," a 120-day pre-foreclosure period officially starts. Your lender cannot file for foreclosure during this time.

This isn’t a grace period to ignore the problem—it’s your time to act.

This is your window to negotiate with the bank, apply for assistance programs, and talk to housing counselors. You might also receive something called a "Lis Pendens" notice, which is a public filing that a lawsuit involving your property is underway. It’s vital to understand what these documents mean.

Understanding the key phases of the North Carolina foreclosure process helps you know how much time you have to act. The clock is ticking, but you have more control than you think if you use this time wisely.

NC Foreclosure Timeline An Overview

| Phase | Typical Duration | What It Means for You |

|---|---|---|

| Pre-Foreclosure | 120 days | This is your critical action period. Your lender has sent a notice but cannot file yet. Use this time to negotiate or find an alternative. |

| Foreclosure Filing | 20-30 days | The lender files with the court. You'll receive a Notice of Hearing. You must respond if you intend to contest it. |

| Foreclosure Hearing | Variable | A Clerk of Superior Court hears the case. If the lender's case is approved, they can schedule a sale. |

| Notice of Sale | 20+ days | The sale date is posted publicly at the courthouse and in a local paper. You still have options, but they are narrowing. |

| Upset Bid Period | 10 days | After the auction, there's a 10-day period where others can place a higher ("upset") bid. This can extend if more bids come in. |

| Redemption Period | Ends at Upset Bid Expiration | This is your final chance to pay the full loan balance plus costs to "redeem" the property and stop the sale. |

This timeline shows that while the process feels fast, there are built-in periods where you can take control. The key is to never wait for the next phase to begin.

Tap Into Free, Expert Help

You absolutely do not have to go through this alone. North Carolina has some fantastic, free resources designed to help homeowners just like you.

The State Home Foreclosure Prevention Project (SHFPP) connects you with HUD-approved housing counselors who can act as an expert negotiator with your lender, and it won't cost you a dime. This program was born out of the 2008 housing crisis and has an incredible track record, providing counseling to over 20,000 homeowners and stopping thousands of foreclosures in their tracks.

Working Directly With Your Lender to Find a Solution

Picking up the phone to call your mortgage company can be one of the hardest things you do. I get it. But trust me, it's often the most direct way to get a handle on this situation.

Here's something most people don't realize: lenders aren't in the real estate business. They don't want to own your house. Foreclosing is a messy, expensive headache for them. This means they're usually very motivated to find a way to keep you in your home and get payments flowing again, even if it’s on new terms.

Don't go into that call asking for a handout. Go in prepared to negotiate. You need to show them you have a plan and you're serious about fixing this.

Preparing for the Call

Before you even think about dialing that number, you need to get your ducks in a row. Walking into this conversation prepared makes all the difference.

Get this stuff together:

- Your Mortgage Account Number: Don't waste time fumbling for it. Have it front and center.

- A Clear Story: What happened? Job loss, medical bills, cut hours? Be ready to explain it simply and honestly.

- Financial Proof: You'll need recent pay stubs and a basic rundown of your monthly income versus your essential bills.

- Your Goal: Make it clear. You want to keep your home and you want to start paying again.

Think of it like a business deal. You're bringing them a problem, but you're also there to help find the solution.

Common Lender Solutions You Can Request

When you get to their loss mitigation department (that's the team that handles these situations), it's a huge advantage if you know what to ask for. The main options they'll consider are loan modifications, repayment plans, and forbearance.

A loan modification is a permanent change to your loan. This isn't a new loan, but a rewrite of your current one to make the payments affordable. Maybe your interest rate gets lowered, or they extend the loan from 30 to 40 years. For someone in Cumberland County on a new, permanently fixed income, this can be a lifesaver.

Real-World Scenario: We knew a homeowner in Fayetteville whose hours at the local plant were cut for good. Their income dropped by $800 a month. They got a loan modification that stretched their loan term out by another ten years. It dropped their payment by $350—enough to make it work.

A repayment plan is for when you've hit a temporary rough patch but are back on your feet. You've missed a few payments, but now you can afford your regular payment plus a little extra to catch up over a few months.

Think about a family in Hope Mills who got hit with a massive, unexpected car repair bill and fell three months behind. Their income is back to normal. The bank might let them pay their mortgage plus half a missed payment for six months straight until they're all caught up.

Finally, there's a forbearance agreement. This lets you hit the pause button. You can temporarily stop or just reduce your payments for a set amount of time. This is perfect for short-term crises.

- Example: A military family at Fort Bragg gets PCS orders. Between moving costs and a spouse needing to find a new job, cash gets tight. A three-month forbearance gives them breathing room to get settled without the stress of the mortgage payment looming over them.

Knowing which one fits your problem—temporary or permanent—is everything. Digging into the different mortgage payment assistance programs gives you the power to ask for exactly what you need. That turns a scary phone call into a real plan to save your home.

Tapping Into North Carolina's State Assistance Programs

While talking to your lender is a vital first move, you have another powerful ally that many North Carolina homeowners completely overlook: the state itself. There are specific, state-run programs designed to be a lifeline, offering real financial help to get you caught up and keep you in your home.

These aren't just vague funds. They're targeted resources created to tackle the real reasons people face foreclosure, like a sudden job loss or a cut in income. For many families, tapping into this support is the critical turning point that saves their home.

The trick is knowing how to get this help. These programs work through a network of local partners right here in our communities, so you can get one-on-one assistance whether you’re in Fayetteville, Raleigh, or anywhere across the state.

Your Strongest Ally: The NC Foreclosure Prevention Fund

If there's one resource you need to know about, it's the NC Foreclosure Prevention Fund. This is the big one. It's managed by the North Carolina Housing Finance Agency (NCHFA) and was built from the ground up to help homeowners struggling with financial problems they didn't cause, like getting laid off.

So what makes this program a game-changer? It offers a zero-interest, deferred loan for up to $36,000 to cover your mortgage payments. This isn't a typical loan you have to start paying back right away. It's designed to give you the breathing room you desperately need to get back on your feet.

This fund has saved thousands of North Carolina homes. Since it started, the NC Foreclosure Prevention Fund has helped over 12,000 families, protecting $1.8 billion in home values from foreclosure and stabilizing local neighborhoods. The program can cover your mortgage for up to 36 months while you search for a new job or get training. You can see the incredible impact it's had over on the Housing Builds NC website.

Here's the most important part: the loan is often forgiven. If you get assistance and stay in your home for ten years after the help ends, you don't have to pay it back. It’s an unbelievable resource for creating long-term stability.

Who Qualifies and How to Apply

To be clear, the NC Foreclosure Prevention Fund has specific rules. It’s mainly for homeowners who have recently lost their job or had their income reduced through no fault of their own. It’s not a fit for every situation, but for those it’s meant for, it’s a true lifesaver.

Generally, you'll need to meet these key requirements:

- Job Loss: You must have been laid off or had your income cut involuntarily.

- Property Type: The house must be your primary residence, right here in North Carolina.

- Loan Status: You need to have an existing mortgage on the property.

You do not have to be behind on your payments to apply. This is a critical point. If you see a layoff coming or your hours have been cut and you know you're going to struggle, you can—and should—apply now. Being proactive is your best strategy.

Taking the First Step

You don't apply for this program directly with the state. The process is smarter than that. It's handled by a network of about 40 HUD-approved housing counseling agencies across North Carolina. This is done on purpose to ensure you get free, personal guidance from an expert every step of the way.

Your first move is to find a participating counseling agency in your area. These counselors are your guide. They will:

- Help you figure out if you're likely to qualify.

- Walk you through gathering all the right paperwork.

- Talk to your mortgage company for you.

- Help you find other options if this fund isn't the right fit.

This setup gives you a support system, taking the stress and confusion out of dealing with a government program on your own. It puts you in touch with a local expert whose only job is to help you keep your home.

What to Do When the Bank Won't Budge

So you've done everything right. You've called the lender, sent the paperwork, and tried to negotiate. But sometimes, it just doesn't work out. They might deny your loan modification, or the new payment they offer is still way more than you can handle.

It’s a gut punch, I know. But this is not the end of the line—not even close. It just means it's time to shift gears and look at other ways to avoid foreclosure in NC and protect your family's future.

When talking to the bank hits a wall, we pivot. The next set of options might mean leaving the home, but they're designed to give you control over the situation and minimize the financial damage. Think of them not as failures, but as smart, strategic moves. The main paths forward are a short sale, a deed-in-lieu of foreclosure, or, in some situations, bankruptcy.

The Short Sale: Selling for Less Than You Owe

A short sale is pretty much what it sounds like. You get your lender’s permission to sell your house for less than the total mortgage balance. The bank agrees to take the money from the sale and call it even, even though it's "short."

Why would they ever agree to take a loss? It's simple math for them. A foreclosure is a long, expensive legal mess. A short sale gets the property off their books quickly and saves them a ton in legal fees and upkeep costs on a vacant house.

Here's a real-world example: We worked with a family in Raeford who inherited a house, but the mortgage was upside down. They lived out of state and couldn't make the payments. A short sale let them find a buyer, satisfy the bank, and walk away without a foreclosure ever staining their credit.

For you, the biggest win is dodging the devastating credit hit of a full foreclosure. A short sale isn't a walk in the park for your credit score, but it's much, much better. Lenders often see it as you taking responsibility in a tough spot.

The Deed-in-Lieu: Handing Back the Keys

Another route is a deed-in-lieu of foreclosure. This is a straightforward exchange: you voluntarily sign the property deed over to the lender. In return, they agree to cancel the rest of your loan. You hand them the keys, and you walk away clean.

It sounds simple, and sometimes it is. But lenders can be picky about this one. If you have a second mortgage, a tax lien, or other judgments against the property, they'll almost always say no. Why? Because they would have to take on those debts themselves.

For a deed-in-lieu to be an option, the house typically needs to be in decent shape with a clean title. It’s a cleaner exit than a short sale, but the bank holds all the cards.

Bankruptcy: The "Automatic Stay" Power Move

When the foreclosure auction is already on the calendar and you're out of time, bankruptcy can be a game-changer. Filing for Chapter 13 bankruptcy triggers what's called an "automatic stay."

This is a powerful legal order that instantly freezes all collection activities. The foreclosure sale stops, dead in its tracks.

The automatic stay gives you critical breathing room. Your debt isn't gone, but it forces the lender to back off while you regroup. Under Chapter 13, you create a repayment plan to catch up on missed payments over 3 to 5 years, all while making your current mortgage payments. It’s a structured way to force your way back onto solid ground.

A word of caution: Bankruptcy is serious business with major, long-term financial fallout. This is not something to try on your own. The rules around how to use bankruptcy to avoid foreclosure in NC are complex. You absolutely need an experienced bankruptcy attorney to guide you and make sure it's done right.

Each of these paths impacts your finances and credit differently. Knowing the pros and cons is key to making the best decision.

Comparing Foreclosure Alternatives: Credit & Financial Impact

Every choice you make from here on out has a different set of consequences. This table breaks down what you can generally expect from each option in terms of your credit, your risk of being sued for the remaining debt, and how long it might take to get back on your feet.

| Option | Credit Score Impact | Deficiency Judgment Risk (in NC) | Time to Recover |

|---|---|---|---|

| Loan Modification | Minimal to moderate drop initially, but improves with on-time payments. | None, as you are fulfilling a new loan agreement. | 12-24 months to qualify for new loans. |

| Short Sale | Significant drop (often 85-160+ points). Less severe than foreclosure. | Low. NC law often protects against this on primary residences, but get it in writing. | 2-4 years to qualify for a new mortgage. |

| Deed-in-Lieu | Significant drop, very similar to a short sale. | Low. Typically waived by the lender as part of the agreement. | 2-4 years to qualify for a new mortgage. |

| Chapter 13 Bankruptcy | Severe drop (130-240+ points). Stays on your record for 7 years. | None for discharged debts, including mortgage deficiencies. | 1-3 years after discharge to potentially qualify for a mortgage. |

| Foreclosure | Most severe drop (200-300+ points). Stays on your record for 7 years. | High. Lenders can pursue you for the difference in many cases. | 7+ years to qualify for a conventional mortgage. |

Understanding these trade-offs is crucial. While options like a short sale or deed-in-lieu hurt your credit, they are far less damaging and offer a much faster recovery period than letting the home go to foreclosure.

Selling Your House for Cash to Avoid Foreclosure

When you’re running out of time and the bank isn’t working with you, the stress can be overwhelming. For many homeowners I’ve worked with in Cumberland County, the fastest and most certain way to avoid foreclosure in NC is to sell the house directly for cash.

This isn’t about giving up. It’s a powerful move to take back control, protect your credit, and walk away with money in your pocket instead of a foreclosure on your record. A cash sale provides a clean break and a guaranteed finish line.

You’re not putting a sign in the yard and hoping for the best. A cash sale means you skip the realtors, the endless showings, and the nail-biting wait for a buyer’s loan to clear. You work directly with a local company—like us—that buys your house as-is, right now.

How a Cash Sale Stops Foreclosure

The real power here is speed. Once that foreclosure notice hits, the clock is ticking on a legal timeline. We know how to work inside that window and can often close the sale long before the auction date arrives.

A cash sale cuts through all the typical home-selling headaches:

- No Repairs Needed. Don't fix a thing. We buy your house exactly as it is today. That leaky faucet or old roof? Not your problem anymore.

- No Realtor Commissions. That 6% commission stays with you. When every dollar counts, this is a huge deal.

- No Showings or Strangers. Your privacy is everything. No open houses, no cleaning up for strangers on a Saturday.

- No Buyer Financing Problems. This is the biggest deal-killer in a traditional sale. Our cash offers are guaranteed. The deal won't fall apart at the last minute.

You get to call the shots on the closing date. If you need to sell in 7 days to stop the auction, we can make it happen. If you need a few weeks to get your affairs in order, we can work with that, too.

A Strategic Exit: Look at it from the bank's perspective. They just want their money back. A fast, guaranteed cash sale gives them exactly what they want and stops the foreclosure dead in its tracks. It's the most effective way to protect your credit from the hit of a full foreclosure.

Real Scenarios Where a Cash Sale Makes Sense

I see this all the time, especially around Fayetteville and Fort Bragg. A quick cash sale provides a solid way out when other options just won't work.

Think about a military family at Fort Bragg getting unexpected PCS orders. They’re underwater on their mortgage and have weeks, not months, to move. They can't afford to let the house sit empty while a realtor tries to find a buyer. A cash sale lets them close fast, get paid, and move on to their next duty station without a foreclosure hanging over them.

Another common one is inheriting a house in Stedman or Hope Mills while living out of state. The property needs work, and you can’t manage a renovation from hundreds of miles away. Selling for cash lets you settle the estate quickly, pay off the mortgage, and avoid a complicated legal mess.

It’s a straightforward solution. If you want to see how it works, you can learn the simple steps to sell your home for cash on our site. It’s all about replacing a stressful, unpredictable problem with a simple, guaranteed transaction that lets you get on with your life.

Here are the answers to the questions that are probably keeping you up at night. When you’re facing foreclosure, the legal talk is confusing and everything feels like it’s moving too fast.

Let's cut through the noise and get you some straight answers.

Can I Stop a Foreclosure Sale That Is Already Scheduled?

Yes, but you have to move like lightning. Even with a sale date on the calendar, you have options.

The biggest hammer you have is filing for Chapter 13 bankruptcy. The second you file, the court issues an "automatic stay." This is a legal order that stops all collection activities dead in their tracks, including the foreclosure sale.

This doesn't make the debt vanish, but it slams the brakes on the auction. It gives you breathing room—three to five years, typically—to work with the court and create a plan to catch up on what you owe. Think of it as a legal timeout.

Another route, though it’s a long shot, is a last-minute deal with your lender or finding a cash buyer who can close before the auction date. The bottom line is, you have to take action. The sale won't stop on its own.

How Long Does Foreclosure Take in North Carolina?

The timeline can shift, but North Carolina law sets some firm deadlines. The most critical one for you is the 120-day pre-foreclosure period. Lenders can't even start the process until you're officially 120 days late.

Once that clock runs out, the lender can file a Notice of Hearing. You’ll get at least 10 days' notice of that hearing. If the clerk gives them the green light, they have to post a Notice of Sale at the courthouse for at least 20 days before the auction.

Even after the auction, it's not over. There’s a 10-day "upset bid" period where someone else can offer a higher price. This is also your absolute last chance to redeem the property by paying off the entire loan balance plus all the costs.

All told, the process can drag out for six months to a year, but it can also happen much faster if you don't fight back.

The Hard Truth: The process has rules, but it moves fast once the ball gets rolling. That 120-day window before things get official is your best and most important chance to negotiate, get help, or find a way out to avoid foreclosure in NC.

Will I Owe Money After a Foreclosure?

It's a definite risk. If the auction price for your home doesn't cover the total amount you owe, that leftover amount is called a "deficiency." In North Carolina, the lender can come after you for it by filing a lawsuit for a deficiency judgment.

But, you have a defense. If the lender themselves buys the property at auction—which happens all the time—you can argue in court that the home's real market value was higher than their lowball bid. A judge might agree, which could slash or even wipe out what you owe.

This is a huge gamble, though, and one of the biggest dangers of letting the foreclosure go through. A short sale or a deed-in-lieu is often negotiated specifically to make the lender waive their right to a deficiency, giving you a clean break and peace of mind.

When the clock is ticking and you're out of good options, you need a guaranteed solution that brings immediate relief. If selling fast is the only thing that will stop the process and save your financial future, DIL Group Home Buyers is your answer.

We buy houses for cash right here in Cumberland County and the surrounding area, closing on your schedule. Get your fair, no-obligation cash offer today by visiting https://dilgrouphomebuyers.com.