When that envelope shows up from your lender, the reaction is often the same. They open it, skim a few lines, feel their stomach drop, and then set it on the counter because they don’t know what to do next.

If that’s where you are right now in Fayetteville, Hope Mills, Spring Lake, or anywhere around Cumberland County, you’re not alone. I’ve seen homeowners freeze because the language feels legal, the timeline feels unclear, and every option sounds expensive or humiliating. The worst move is silence. Banks keep moving whether you act or not.

You need a straight answer on how foreclosure affects your credit score, what happens next in North Carolina, and what option protects you before significant damage hits. That’s what this article is about.

That Official Letter Has Arrived What Happens Now

A lot of homeowners think the first letter is just another warning. It isn’t. It’s the point where the problem stops being private and starts moving toward a formal process.

Maybe you missed payments after a job change. Maybe you’re going through divorce. Maybe you own a rental in Fayetteville and the house became a money pit. Maybe you got military orders and the mortgage on the old place didn’t get paid the way you planned. However it happened, the feeling is usually the same. Fear, embarrassment, and a strong urge to wait one more week.

Waiting is what gets people hurt.

What that letter really means

That notice usually means your lender is documenting the default and building the file needed to push the matter forward. It doesn’t mean your house disappears tomorrow. It does mean the window to protect yourself is open right now, not later.

If you’re unsure what mortgage default triggers, read this explanation of what happens when you default on a mortgage. It lays out the sequence in plain English.

Practical rule: The earlier you act, the more choices you keep. Once missed payments pile up and formal filings begin, your options narrow fast.

The mistake I see most often

People spend weeks trying to “catch up” with money they don’t have. They drain savings, borrow from family, skip other bills, and still can’t solve the mortgage problem. By then, they’ve lost time and added stress.

Start with clarity instead:

- Read every page: Don’t guess what the notice says.

- Check the dates: Deadlines matter.

- Stop avoiding the numbers: You need to know whether keeping the house is realistic.

- Look at exit options early: If the loan can’t be saved, the property still can be sold before foreclosure finishes.

You don’t need to like the situation. You do need to deal with it directly.

Understanding the Foreclosure Process in North Carolina

North Carolina foreclosure can feel confusing because homeowners often hear mixed advice from neighbors, lenders, and people online. Strip away the noise and the process becomes easier to understand. Missed payments lead to default. Default can lead to formal notice. If nothing changes, the lender pushes toward a sale.

That sequence matters because your best choices usually exist before the final stages.

The process starts before the courthouse

Foreclosure doesn’t begin the day of sale. It begins much earlier, when mortgage payments stop being made and the loan falls behind.

During that pre-foreclosure period, homeowners often still have room to act. That can mean trying to bring the loan current, discussing loss mitigation with the lender, or deciding to sell before the case gets further along. If you want a plain-language overview of those paths, this guide on how to avoid foreclosure in NC is a useful starting point.

What matters most is this. The bank follows a process. You should too.

Key stages homeowners need to understand

Here’s the version I give people locally when they want the plain truth.

You miss payments

The lender starts sending notices and late statements. This is the earliest warning sign, and it’s the stage too many people waste.The loan is treated as seriously delinquent

By this point, the lender is no longer looking at the issue as temporary unless you show a real plan.Formal foreclosure steps begin

Notices are issued, documents are prepared, and the matter starts moving through the legal system.The property is scheduled for sale

Once that happens, the pressure jumps. Deadlines get tighter and buyers, lenders, and attorneys all move on their own schedule.

Terms that scare people more than they should

A lot of the stress comes from legal wording. Most of it sounds worse than it is, but you still need to know what it means.

- Default: You failed to meet the mortgage terms, usually by missing payments.

- Notice: The lender’s formal communication that the loan is in trouble and action may follow.

- Foreclosure sale: The property is sold through the foreclosure process.

- Deficiency balance: In some situations, the money from the sale doesn’t cover what’s owed.

A notice is not the end of the road. It’s a warning that your decision window is shrinking.

Where homeowners still have leverage

You have the greatest advantage before the process reaches the end. That’s when you still control timing, paperwork, and how the property leaves your hands.

The people who do best in this situation usually make one hard decision early. They stop asking, “Can I somehow delay this?” and start asking, “What outcome protects me the most?” That’s a much better question.

In practical terms, that means looking at the house as an asset that can be used to avoid a far worse financial event. If keeping it isn’t realistic, then preserving your future matters more than preserving pride.

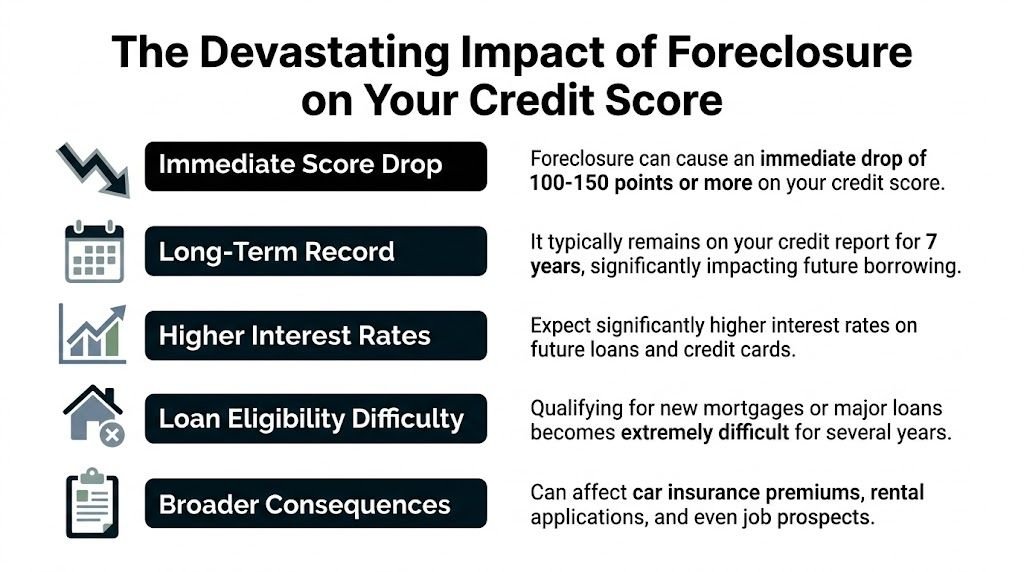

The Devastating Impact of Foreclosure on Your Credit Score

You can miss a few bills and still recover. A foreclosure is different. Once that mark hits your credit file, it can drag down a score you spent years building, and the people with the best credit often watch it fall the farthest.

That catches Fayetteville homeowners off guard. They assume a long history of on-time payments will soften the hit. It usually does the opposite. A cleaner file gives the credit scoring system more room to drop.

How hard the score can fall

According to FICO foreclosure impact data summarized by Nolo, a borrower starting at 680 can lose 85 to 105 points after foreclosure, while a borrower starting at 780 can lose 140 to 160 points. Nolo also reports that foreclosure can push some score drops into the 200 to 300 point range.

That kind of drop changes everyday life. Credit cards get more expensive. Car loans get harder. Renting another home can become a fight.

Why strong borrowers often get punished harder

Foreclosure signals a severe breakdown in payment history, and payment history carries the most weight in common credit scoring models. Experian’s breakdown of FICO scoring factors explains why a major mortgage default hits so hard. The scoring model is measuring how far your behavior fell from what it expected.

So yes, the homeowner who spent years doing things right can see the sharpest visible drop. That is one of the cruelest parts of foreclosure.

Good credit is worth protecting early, because once foreclosure is reported, the fall is steep.

The score usually starts dropping before the foreclosure is final

Auction day is not the beginning of the damage. The damage starts with the late payments that lead up to it.

Thirty-day lates hurt. Sixty-day lates hurt more. Ninety-day lates and a mortgage in serious default tell future lenders that this was not a one-time slip. By the time the foreclosure itself is reported, your credit has often already taken several hits in a row.

That matters because waiting too long costs you twice. You lose time, and you lose score.

Recovery takes time you may not have

Nolo’s summary of FICO research also notes that recovery was slow for many borrowers, especially those who entered foreclosure with stronger credit profiles. That matches what I see in real situations. People expect the pain to end when the house is gone. It does not.

The credit effect hangs around long after the move-out, the sale, and the paperwork. Lenders, landlords, insurers, and sometimes employers can all see some version of the financial trouble you went through.

The practical lesson

If you are already behind, stop treating foreclosure like a future problem. It is a current credit problem.

The smart move is to protect your file before the foreclosure is completed. In many cases, the cleanest exit is a fast cash sale before the lender finishes the process. You may still have some late-payment damage, but that is far easier to recover from than a completed foreclosure sitting on your report for years.

Foreclosure vs Alternatives What Appears on Your Credit Report

A Fayetteville homeowner gets offered three exits by the bank or by circumstance. Let the foreclosure finish. Try a short sale. Hand the property back through a deed-in-lieu. On paper, those can sound like reasonable alternatives. On a credit report, they do not look the same, and none of them should be confused with a clean sale before foreclosure is completed.

What future lenders actually see

Lenders are not reading your story. They are reading the reporting.

A completed foreclosure stands out because it shows the loan ended in a forced loss of the property. Short sales and deed-in-lieu agreements can avoid that exact label, but they still signal distress. The account may be reported in a way that shows the debt was not paid as originally agreed, which still raises concerns for future lenders, landlords, and underwriters.

That is the part homeowners often miss. The bank may present a short sale or deed-in-lieu as a cooperative solution. Cooperative does not mean harmless.

Comparing the main options

| Option | What may appear on your credit report | Credit impact in plain English | Key takeaway |

|---|---|---|---|

| Foreclosure | A foreclosure-related negative entry tied to the mortgage | Usually the most damaging outcome in this group | Worst choice if protecting future borrowing matters |

| Short sale | Negative mortgage reporting, often showing the debt was resolved for less than originally owed | Usually less harmful than foreclosure, but still serious | Damage control, not credit protection |

| Deed-in-lieu | Negative mortgage reporting showing the property was surrendered to satisfy the debt | Often viewed similarly to a distressed mortgage resolution | Better than letting foreclosure run, but still a major credit event |

| Direct sale before foreclosure | No foreclosure entry if the sale closes before the process finishes | Often the cleanest result available once you know you cannot keep the house | Best option if your goal is to limit long-term credit damage |

Short sale and deed-in-lieu are not clean exits

I want to be blunt here. A short sale is not a credit-saving strategy. A deed-in-lieu is not a fresh start button.

Both can be useful if foreclosure is closing in and you have no better option. Both can also be better than letting the lender complete the foreclosure. But if your goal is to preserve as much of your credit file as possible, the stronger move is usually to sell the house before the foreclosure is finished, preferably for cash if time is tight and the property needs work.

That difference matters because the credit report reflects the outcome, not your intentions.

The practical decision rule

Use this standard.

- Keep the house only if you can afford to keep it.

- Use a short sale or deed-in-lieu only if a regular or cash sale is no longer realistic.

- Treat foreclosure as the last outcome to avoid, not one more option on the list.

- If speed is the issue, sell before the lender finishes the process.

Homeowners in Fayetteville get hurt when they wait for the lender to suggest a path. That is backwards. Decide based on what will show up on your report and what gives you the best chance to protect your next rental, next loan, and next home purchase.

If you cannot save the house, save your credit from a completed foreclosure. That is usually the smarter win.

The Long Shadow Financial Consequences Beyond Your Credit Score

A foreclosure isn’t just about a three-digit score. That score gets the attention, but the true damage shows up later when you try to rent a place, buy a car, qualify for a mortgage, or explain your financial history to someone reviewing an application.

That’s why I push homeowners to think bigger than “How many points will I lose?” The better question is, “What doors will close if this goes through?”

Borrowing gets harder long after the event

Future lenders don’t review your file in a vacuum. They look at the score, the mortgage history, the public record issues tied to the property, and the overall picture of financial stress.

That can affect:

- Mortgage applications: A new home purchase gets harder because the past housing event carries extra weight.

- Car loans and credit cards: Approval may still happen, but on worse terms.

- Refinancing options later: Even after the crisis passes, the old event can follow you into future financing conversations.

The consequences spread into everyday life

People often learn this the hard way. They think the problem ends once they leave the house. Then they apply for a rental, or a lender asks deeper questions, or a background review pulls records that force an awkward explanation.

A foreclosure can also create stress around insurance pricing, employment reviews in some fields, and any process where someone is judging financial reliability. The score is only one piece of the file.

A foreclosure rarely stays contained. It tends to show up again when you least want to talk about it.

The emotional cost is real too

I don’t mean that in a soft, motivational way. I mean it in a practical way. Financial damage creates decision fatigue. People avoid checking credit, avoid opening mail, avoid applying for opportunities, and delay rebuilding because they’re embarrassed.

That hesitation costs more than is generally understood.

Here’s what I want homeowners in Fayetteville to understand. Preserving your credit isn’t vanity. It’s influence. It affects where you live next, what you pay next, and how quickly you can recover.

Why avoiding foreclosure matters more than recovering from it

Once the event is on your report, the conversation changes. You’re no longer preventing damage. You’re managing fallout.

That’s a much weaker position. You can rebuild from it, yes. People do. But if you still have a path to avoid the foreclosure itself, that path deserves serious attention before you surrender to “I’ll just fix it later.”

Your Best Defense Avoiding Foreclosure with a Proactive Sale

You miss a few payments, the letters pile up, and every week you wait gives the lender more control. That is the moment to make a clean decision. If keeping the house is no longer realistic, sell before foreclosure is completed.

That is usually the strongest move for your credit and your options afterward.

Why selling early works better

A completed foreclosure leaves a serious negative mark on your credit report. A short sale or deed-in-lieu may reduce some of the fallout, but those are still distressed outcomes. A direct sale before the foreclosure finishes does something more important. It stops the foreclosure event itself from being added to your report.

Be clear about what that means. Selling the house does not erase damage from missed mortgage payments you have already made. Those late payments may still hurt your score. What it can do is prevent the much heavier foreclosure entry that makes recovery harder and longer.

That is a significant advantage. You are cutting off further damage before it gets worse.

Why this matters in Fayetteville

I see the same pattern across Fayetteville and Cumberland County. Owners wait because they are hoping for a perfect fix, and the clock keeps running.

A normal listing can be fine if the home is in good condition, the mortgage is current, and you have time to deal with repairs, showings, inspections, and buyer financing. Foreclosure cases usually do not look like that. They look like job changes, PCS orders, inherited properties, vacancy, deferred maintenance, and owners who are already short on cash.

In that situation, speed matters more than squeezing out every last dollar on paper.

What a proactive sale actually protects

A fast sale is not about panic. It is about protecting what you still can.

When you sell before the foreclosure process is finished, you can often avoid:

- Additional late payments: Every extra month behind can add more damage.

- The foreclosure mark itself: That is usually the hardest hit to recover from.

- Delays tied to repairs or financing: Distressed houses often struggle in the traditional market.

- Loss of control over timing: Once the bank pushes deeper into the process, your choices shrink fast.

The smart move is usually the early move.

When a cash buyer makes sense

A cash buyer is not the right fit for every homeowner. It is a strong fit when time is short, the property needs work, the mortgage is behind, or the seller cannot deal with the uncertainty of a traditional listing.

If that sounds like your situation, read can I sell my house while in foreclosure. In many cases, yes, you can. The earlier you act, the more you can protect.

Here is the practical comparison:

| Path | Best when | Main risk |

|---|---|---|

| Traditional listing | House is in good shape, time is available, payments are manageable | Delays, inspections, financing fallout |

| Short sale | Owe more than the house can sell for, lender must approve | Credit damage still follows |

| Waiting on the lender | Rarely a strong choice | Loss of control |

| Direct as-is cash sale | Need speed, certainty, fewer obstacles, and a chance to avoid the foreclosure event on your credit report | Offer may prioritize convenience over listing upside |

My recommendation

If the payment problem is not temporary, stop treating delay like a strategy. It is not. It usually means more missed payments, more stress, and less room to protect your credit.

Sell while you still have control of the timeline.

Do not accept a weak offer just because you feel cornered. Compare your real options quickly, ask direct questions, and choose the exit that protects your finances, your housing options, and your next chapter. In foreclosure situations, decisive action beats wishful thinking every time.

Taking Control of Your Future and Protecting Your Credit

Foreclosure feels personal, but the solution has to be practical. Your lender is looking at a file. You need to look at consequences.

If foreclosure goes through, the credit damage can be severe. Other “alternatives” like short sale or deed-in-lieu may reduce the sting somewhat, but they still leave real scars on your report. If you can exit before the process finishes, that’s usually the stronger move.

What to do today

Don’t overcomplicate this. Start with action.

- Gather the mortgage paperwork: Know what stage you’re in.

- Be honest about affordability: If the payment problem isn’t temporary, admit it.

- Check whether the house can be sold quickly: Time matters.

- Protect your credit before the final event hits: That’s the smart play, not the desperate one.

The choice is clearer than most people think

You’re choosing between two broad paths.

One path is delay, stress, more missed payments, and a formal foreclosure mark that can follow you long after you leave the property.

The other path is taking control early, selling before the process finishes, and preserving as much of your financial footing as possible.

You do not need to wait for the bank to decide how this ends.

That’s the part I want you to hold onto. This situation is serious, but it isn’t hopeless. Plenty of homeowners make a clean exit once they stop avoiding the issue and start dealing with it directly.

My blunt advice

If you’re still asking how foreclosure affects your credit score, you’re asking the right question. But don’t stop there. Ask the better question too. “What can I do today to keep foreclosure off my credit in the first place?”

That question leads to solutions. The first one leads mostly to regret if you ask it too late.

Take the next step while you still have an advantage.

If you’re behind on payments in Fayetteville or anywhere in Cumberland County and want a direct, confidential option, contact DIL Group Buyers. You can request a no-obligation cash offer, sell the house as-is, choose a closing timeline that works for you, and avoid the delays that often push homeowners deeper into foreclosure trouble.