You got the offer. Instead of feeling relieved, you may be staring at your phone thinking, “Now what?” That is normal.

A lot of Fayetteville homeowners know how to list a house, negotiate a price, and sign a contract. What throws them is the word closing. It sounds technical, expensive, and easy to mess up. If you are behind on payments, dealing with a military move, handling an inherited property, or trying to sell from out of state, that uncertainty gets worse fast.

Here’s the plain-English answer to what does closing on a house mean: it is the final step where the sale becomes official. The paperwork gets signed, the money gets sent where it needs to go, and ownership transfers from seller to buyer.

That sounds simple. Sometimes it is. Sometimes it turns into a slow grind full of inspections, lender demands, title issues, and last-minute delays. The path matters just as much as the closing day itself.

Your Offer Was Accepted What Happens Now?

You accept an an offer on your house in Fayetteville. Maybe you are already packing for a PCS move. Maybe the property needs repairs you cannot afford. Maybe you inherited the house and live in another state. The contract is signed, but instead of peace of mind, you feel pressure.

That pressure usually comes from not knowing what closing involves.

Closing is the finish line. It is the point where the legal documents are completed, the money is disbursed, and the property officially changes hands. Until that happens, you do not have a completed sale. You have a deal in progress.

That distinction matters.

A traditional sale can feel like you are carrying the house across the finish line while other people inspect it, appraise it, question it, and delay it. A cash sale is usually much more direct. There are fewer moving parts, fewer people involved, and fewer chances for the deal to fall apart.

If you are in a stressful situation, do not treat every closing the same. They are not.

The two paths sellers usually face

- Traditional closing: More paperwork, more conditions, more waiting, and more opportunities for bad news.

- Cash closing: Fewer hurdles, a shorter path, and a lot less dependence on a lender’s timeline.

If your life is already messy, do not choose a sale process that makes it messier.

Most stressed sellers do not need more “options.” They need a clear path. Closing is not mysterious once you understand who is involved, what gets signed, and where deals usually get stuck.

The Final Handshake What Closing on a House Really Is

Think of closing like the final checkout on a major purchase. You have already agreed on the item. Now the transaction has to be finalized properly so nobody can come back later and say the transfer was incomplete.

In real estate, closing on a house means the final legal and financial step where ownership transfers. In a traditional sale, that usually happens several weeks after the purchase contract is signed, and buyers commonly face closing costs averaging 3% to 6% of the loan amount nationwide, as explained in Bank of America’s overview of what happens at closing.

For a seller, the core issue is simple. You are not just “selling” when you sign the contract. You are selling when the closing is completed and the deed is transferred.

What happens at closing

Several things happen in a short window:

- Documents are signed: The deed and other closing papers are completed.

- Funds are distributed: Existing loans, fees, and seller proceeds are handled.

- Ownership transfers: The buyer becomes the legal owner.

- The transaction gets recorded: The transfer is made part of the public record.

In North Carolina, the closing attorney plays a major role in getting this done correctly. That matters because this is not just a handshake and a key exchange. It is a legal transfer.

The main people involved

Seller

Your job is to sign the required documents, provide accurate information, and make sure any agreed terms are met before closing.

Buyer

The buyer brings funds, signs their side of the paperwork, and completes any final conditions tied to the contract.

Closing attorney

In North Carolina, the attorney handles the legal side of the closing, coordinates the paperwork, and helps make sure title issues are addressed before the transfer.

Title company or title professionals

They help confirm the property can be transferred with clear ownership. If you want a plain-English breakdown of that part, this guide on what is a title search for property is worth reading.

A lot of seller stress comes from treating closing like one event. It is better to think of it as a legal checkpoint. If everything is clear, you move through it. If something is not clear, the sale slows down until someone fixes it.

The Traditional Closing Timeline A 45-Day Marathon

Traditional closings wear sellers down because the closing day is only the end of a much longer process. The contract gets signed, and then waiting begins.

The broader closing process in a financed sale typically lasts several weeks or more from contract to keys, and the disclosure rules shaped by RESPA in 1974 and refined by TRID in 2015 added transparency but also more procedural steps, as noted in this summary of the home closing process).

What happens after the contract is signed

The typical sequence looks straightforward on paper.

- The contract is opened and shared with the professionals involved

- Title work begins

- The buyer schedules inspections

- The lender orders an appraisal

- The lender reviews the buyer’s file

- Conditions get issued and cleared

- A final walkthrough happens

- Closing day arrives

In practice, each one of those steps can trigger delay.

Where sellers usually get blindsided

Inspections create new negotiations

The buyer may accept your price and still come back asking for repairs, credits, or concessions after the inspection. If the house has deferred maintenance, that phase can become a second negotiation.

Appraisals can change the deal

If the property does not appraise the way the lender wants, the buyer may try to renegotiate. That is one of the most frustrating parts of a financed sale because the seller has little control over it.

Lender underwriting drags everything out

The lender may ask the buyer for more documents, then more documents again. You are waiting while someone else proves they can close.

A signed contract does not guarantee a closed sale. In a traditional deal, it often means the uncertainty has just moved to a different stage.

Why the marathon feels so draining

Traditional closings demand patience from sellers who often do not have any left. If you are behind on payments, managing a vacant house, or trying to relocate on orders, a long timeline is not just annoying. It can be a financial and emotional problem.

This short video gives a useful overview of the moving parts involved in the process.

The practical reality for Fayetteville sellers

A house near Fort Bragg can attract interest fast, but that does not mean a financed buyer can perform fast. The more layers you add, the more likely the closing date shifts.

For stressed sellers, the biggest mistake is assuming “under contract” means “done.” It does not. Traditional closing is a chain. One weak link slows everything down.

Decoding the Paperwork and Costs for Sellers

Most sellers do not fear the signature itself. They fear the pile of paperwork and the shrinking number at the bottom of the closing statement.

That fear is justified. A traditional closing has real costs, and they are not always obvious when you first accept an offer.

The documents that matter most

You do not need to memorize every page. You do need to know what the important documents are doing.

The deed

This is the document that transfers ownership from you to the buyer. If the deed is not handled correctly, the sale is not clean.

The closing disclosure or settlement paperwork

This shows where the money is going. It lays out payoffs, fees, credits, and the amount you will receive.

Title-related documents

If there is an old lien, judgment, ownership issue, or recording problem, it shows up here. Those problems are not minor administrative details. They can stop the sale.

Why title issues matter so much

In a traditional sale, seller closing costs can be significant, and title defects are a major problem. According to Rocket Mortgage’s explanation of closing on a house, title defects cause 80% to 90% of closing delays in major U.S. markets, and the costs are detailed on the TRID-compliant Closing Disclosure provided 3 business days before closing.

That is one reason distressed properties create extra friction. Older payoff issues, inherited ownership, code problems, or unresolved paperwork can all make the final review harder.

The seller costs that cut into your proceeds

Here is the blunt version. The sale price is not the number you keep.

| Cost area | What it usually means for the seller |

|---|---|

| Agent commissions | A large share of your proceeds may go to listing and buyer-agent commissions in a traditional sale |

| Repair concessions | Buyers often ask for credits or repairs after inspections |

| Title cleanup | Old issues may need to be resolved before closing |

| Prorations and adjustments | Taxes and other items may be split at closing |

| Attorney and transaction fees | Standard transaction costs can reduce your net further |

If you want a closer look at how these expenses are usually handled in this state, this breakdown of who pays closing costs in North Carolina gives useful local context.

The seller mistake I see most often

Sellers focus on sale price and ignore net proceeds.

A higher offer with repair requests, delays, commission costs, and title headaches can leave you in worse shape than a lower but cleaner deal. That is not theory. That is how a lot of closings disappoint people.

Do not judge an offer by the top-line number alone. Judge it by what reaches your bank account and how much risk you carry until closing.

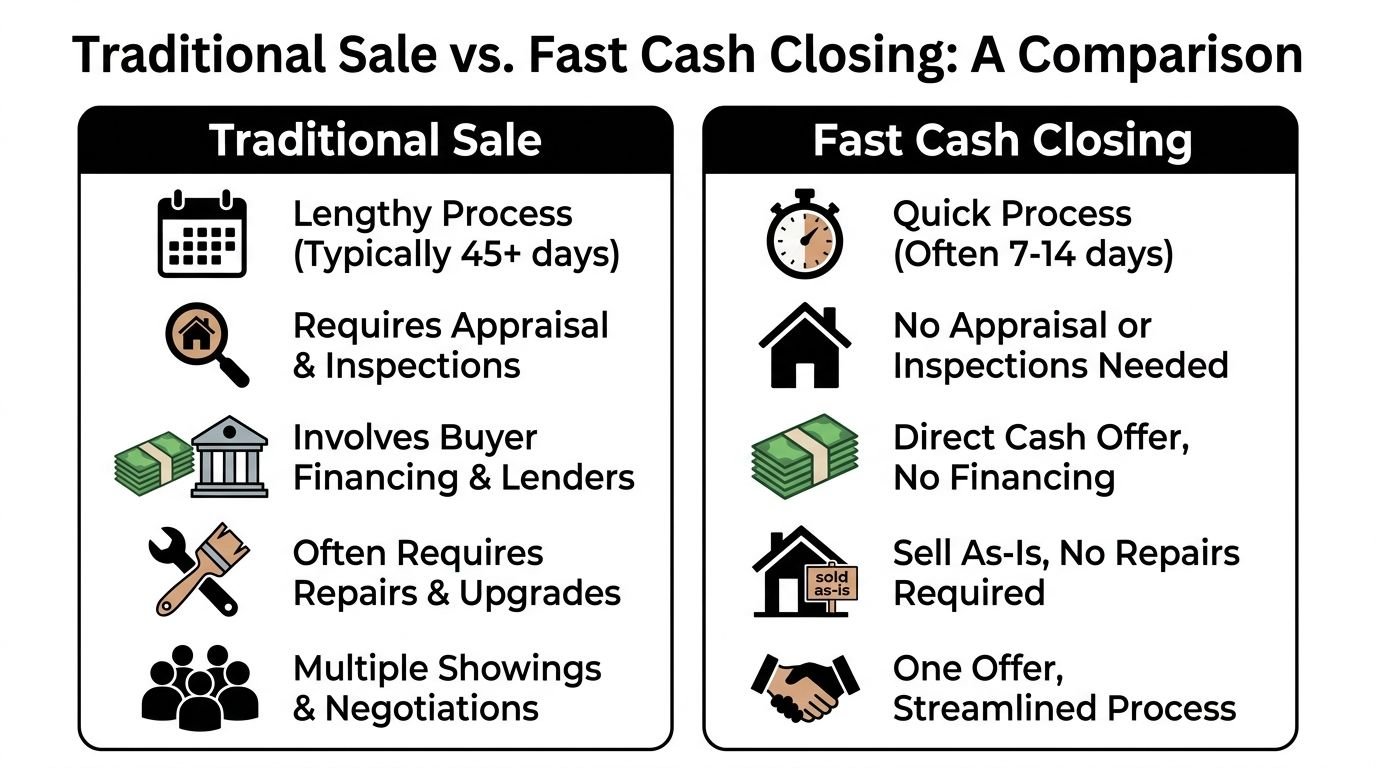

Traditional Sale vs Fast Cash Closing A Comparison

For a distressed seller, this is the only comparison that matters. Not “Which option sounds nicer?” The question is, “Which option gives me the cleanest exit with the least risk?”

For military PCS or foreclosure situations, quick-cash closings can avoid extended traditional timelines and remove the risk of the sale collapsing over appraisal or financing issues, which happens in up to 30% of financed deals, because cash buyers bypass lender underwriting, according to MilitaryByOwner’s guidance on the seller closing process.

Traditional Closing vs DIL Group Cash Closing

| Factor | Traditional Sale | DIL Group Cash Closing |

|---|---|---|

| Timeline | Often measured in weeks and can stretch much longer | Often a week to two weeks |

| Financing risk | Buyer depends on lender approval | No lender underwriting |

| Inspection pressure | Commonly leads to repair demands or credits | Usually sold as-is |

| Appraisal risk | Low appraisal can disrupt the deal | No appraisal dependency |

| Fees and commissions | Seller often pays multiple transaction costs | No realtor commissions, no attorney fees, no hidden costs |

| Showings and prep | Usually requires cleaning, access, and repeated showings | Efficient process with one direct offer |

| Certainty | More chances for delays and renegotiation | Simpler path to the closing table |

What the table means in real life

Traditional sales reward houses that are easy to sell

If the house is updated, empty, clean, and free of complications, the traditional market can work fine. However, that is not the situation for many owners in Cumberland County.

If you are dealing with tenant damage, inherited title complications, foreclosure pressure, or major repairs, the traditional process often punishes you twice. First with delay. Then with deductions.

Cash closings reduce moving parts

The biggest advantage is not just speed. It is certainty.

A cash buyer is not waiting for a lender, not worried about an appraisal gap, and usually not using an inspection report to reopen the deal. That changes the entire tone of the transaction.

If you want the basics of that type of sale, this explanation of what is a cash offer on a house breaks it down clearly.

My direct recommendation

If your property is distressed or your timeline is tight, stop chasing the “perfect” traditional buyer. That route often works best for houses that look easy on paper.

Choose the process that matches your situation. If your priority is speed, simplicity, privacy, and fewer ways for the sale to fail, cash is usually the better tool.

Your Closing Day Checklist for a Smooth Sale

Closing day should feel boring. That is the goal. No drama, no confusion, no missing paperwork.

The best way to get that result is to prepare for a short list of practical tasks and handle them early.

What to bring

- Government-issued ID: The closing attorney will need to verify who you are.

- House keys and access items: Bring keys, garage remotes, gate fobs, and alarm information if required.

- Any documents you were asked to provide: If the attorney or title side requested something, do not assume they can work around it.

- Your wiring instructions if needed: Confirm them carefully and directly with the closing office.

What to expect at the appointment

The attorney or closing professional will walk you through the seller documents. Read what you sign. Ask questions if a charge or payoff looks wrong.

Expect the meeting to focus on signatures, final confirmation of amounts, and transfer details. If the property had any special issue during the process, ensure it was handled the way you were promised.

Review your final figures before you sign. Closing day is the worst time to discover you misunderstood your net proceeds.

What to handle right after closing

- Cancel or transfer utilities: Do not keep paying for a house you no longer own.

- Forward your mail: Especially important for out-of-state owners and inherited property sales.

- Keep copies of signed documents: Save digital and printed copies if possible.

- Confirm proceeds arrived: Make sure funds were sent the way you expected.

A smooth closing is rarely about luck. It comes from simple preparation and clear communication.

Answers to Your Top Closing Questions

Can I still sell if I am behind on mortgage payments or facing foreclosure

Yes, in many cases you can still sell before the foreclosure process reaches the point where your options disappear. The key is speed. Waiting usually makes the problem worse because fees, deadlines, and pressure keep building.

If time is short, a slow traditional sale may not fit your specific situation.

Do I have to come back to Fayetteville if I live out of state

Not always. Many sellers handle document signing remotely through the professionals involved in the transaction. That is especially common with inherited properties, absentee owners, and military families who have already relocated.

The important part is coordination. Do not wait until the last minute to ask how your signing will be handled.

What happens if the title search finds a problem

The sale pauses until the problem is resolved or the parties decide not to proceed. Sometimes the issue is simple. Sometimes it is not.

Common examples include old liens, ownership questions, payoff issues, or paperwork errors. This is one of the clearest reasons distressed sellers benefit from addressing problems early instead of hoping they disappear.

Can a buyer back out before closing

Yes, if the contract gives them ways to do that. In a traditional sale, contingencies can give buyers room to exit or renegotiate based on financing, inspections, or appraisal issues.

That is why a signed offer is never the whole story.

What if my house needs major repairs

You can still sell it. The question is which type of buyer you are trying to attract. A retail buyer usually wants condition, lender approval, and fewer complications. A cash buyer is often a better fit for a house that needs work.

How do I know which closing path is right for me

Use a blunt test. If you need maximum price and have time, patience, and a house in solid shape, the traditional route may work. If you need certainty, speed, less exposure, and fewer demands, a cash sale is usually the smarter move.

Take Control of Your Home Sale and Move Forward

Closing on a house is not complicated once you strip away the jargon. It is the moment the sale becomes official. The deed is signed, the money is distributed, and ownership transfers.

What makes sellers anxious is not the definition. It is the path to get there.

A traditional closing can work, but it asks a lot from a stressed homeowner. It demands time, patience, flexibility, and a tolerance for delays. If the buyer’s financing stumbles, the appraisal comes in low, or title issues surface late, your “done deal” can stop feeling done very quickly.

A fast cash closing is different because it cuts out many of the failure points that drag traditional sales off course. For homeowners in Fayetteville, Hope Mills, Spring Lake, and surrounding areas dealing with foreclosure pressure, repairs, inherited property problems, bad tenants, or an urgent move, that simplicity matters.

You do not need more confusion. You need a path that fits your situation and lets you move on with your life.

If you want a straightforward option, DIL Group Buyers buys houses in Fayetteville-area communities as-is, with no realtor commissions, no attorney fees, no hidden costs, and a closing date that fits your timeline. Reach out for a no-obligation cash offer and get a clear, stress-free path forward.