You’re probably here because the numbers are starting to blur together.

You got an offer on a house in Fayetteville, Hope Mills, Spring Lake, or somewhere else in Cumberland County. Maybe the property needs work. Maybe you already moved. Maybe you’re dealing with tenants, probate, missed payments, or PCS orders. Then the closing statement shows up and suddenly the sale price is not the amount you take home.

That shock is common. It is also avoidable if you know who pays what before you sign anything.

In North Carolina, both the buyer and the seller pay closing costs, but they do not pay the same kinds of costs. The split matters. It affects your net proceeds, your timeline, and your ability to get out of a hard situation cleanly.

If you want the short version of who pays closing costs in north carolina, here it is: buyers usually carry the financing-related costs, and sellers usually carry the transfer tax and several sale-related deductions. In distressed sales, things can get messier fast.

Decoding the Final Bill in Your NC Home Sale

You accept an offer, start planning your move, and then the settlement statement shows up packed with fees you did not budget for. That moment hits hard if you are already dealing with missed payments, a probate property, tenants, or PCS orders out of Fort Liberty.

A closing cost covers the legal and administrative work required to transfer ownership of a house. In North Carolina, that usually includes attorney handling, deed preparation, recording, title review, tax adjustments, and payoff coordination. These steps are required in a normal sale.

For a stable seller with time, those charges are frustrating but manageable. For a distressed seller in Cumberland County, they can wreck the plan. If you are out of state, helping family sell an inherited house in Fayetteville, or trying to unload a property before a military relocation, every fee cuts into the cash you expected to walk away with.

What buyers and sellers usually pay

In a standard North Carolina sale, both sides pay closing costs. Buyers usually get hit with the loan-related charges. Sellers usually see their costs deducted from the sale proceeds, along with any mortgage payoff, tax proration, and other sale-related charges.

That structure creates a real problem for sellers under pressure.

You may not write a separate check for every item, but the result is the same. Your net shrinks. If the house needs repairs, has a lien issue, or sits vacant while you live in another state, the traditional process gets expensive fast.

Why North Carolina closings feel more complicated

North Carolina closings are more involved because attorneys are central to the process, title issues have to be cleared before transfer, and the settlement statement stacks several line items into one final calculation. Sellers often underestimate that complexity until they are already committed.

That is a mistake.

If the property has heirship questions, code violations, old judgments, unpaid taxes, or a messy payoff situation, ask for a draft estimate early. Do not wait until the week of closing to learn what the deal puts in your pocket.

One document tells the truth

The settlement statement is the number that matters. It shows the sale price, every deduction, and what you receive at the end.

If you need a clearer understanding of the title portion of that process, read this guide on what a title search is for property. It helps explain why a simple sale can turn into a delay for military sellers, heirs, and absentee owners.

For many Cumberland County homeowners, the key decision is not whether closing costs exist. They do. The decision is whether a traditional sale still makes sense after the fees, delays, repair requests, and uncertainty are added in, or whether a direct cash sale solves the problem with fewer deductions and less risk.

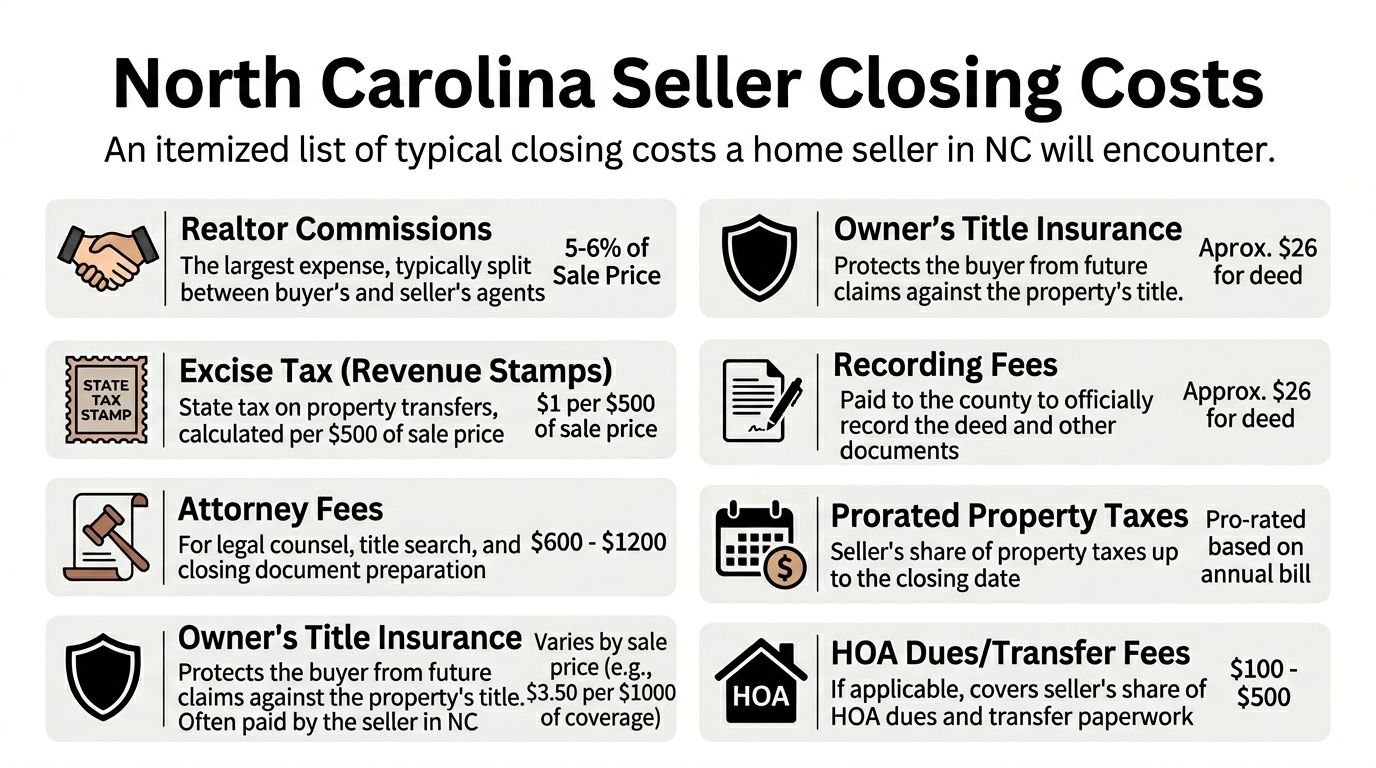

The Seller's Ledger Typical Closing Costs You Will Pay

A Fayetteville seller can accept what looks like a solid offer, then watch the check shrink fast at closing.

That problem hits harder if you are selling from out of state, dealing with a military move, handling an inherited house, or trying to unload a property that needs work. Traditional closings in North Carolina come with a seller ledger, and every line on it cuts into your net.

The standard line item

In North Carolina, sellers are almost always responsible for the state transfer tax, also called excise tax or revenue stamps, and it is charged at a fixed rate of $1.00 per $500 of the property’s sale value. On a $320,000 home, that equals exactly $640, as explained in Aspyre Realty Group’s NC closing cost guide.

Start your math there. Then keep going, because that tax is only one deduction.

What usually comes out of the seller’s side

In a traditional North Carolina sale, sellers commonly pay for items like these:

- Transfer tax: A standard seller charge in most normal transactions.

- Attorney-related closing charges: Deed prep and seller-side legal closing work are common.

- Prorated property taxes: You owe your share through the closing date.

- HOA charges: Transfer fees, resale documents, and unpaid dues can all show up.

- Agent commissions: This is often the largest deduction in a listed sale.

- Repair credits or concessions: These are common after inspections, especially with older or distressed homes.

Many sellers focus on the sale price and ignore the deductions, which is a mistake.

What this means in real life

Seller closing costs in North Carolina usually include the standard items above, then grow when the deal gets messy. That is the part stressed sellers in Cumberland County need to respect.

A military owner with PCS orders may not have time for repair negotiations. An out-of-state heir may not even know an old tax bill, lien, or HOA balance is still attached to the property. A distressed seller in Fayetteville may get hit from both sides. Lower offers because of condition, then more deductions at closing.

That is how a decent contract turns into a disappointing net.

A blunt recommendation for stressed sellers

If the house is updated, vacant, easy to show, and unlikely to trigger repair demands, listing can still work.

If the property has deferred maintenance, tenant issues, title complications, probate questions, or you need certainty more than exposure, compare your traditional net against a direct sale before you sign anything. Review a real sell home for cash option in Fayetteville and compare what lands in your pocket after fees, credits, and delays.

Key takeaway: The seller does pay closing costs in North Carolina. Beyond the obvious costs, sellers should be aware of the extra deductions that can accumulate when a deal gets complicated.

The Buyer's Checklist Costs Paid by the Home Purchaser

A financed buyer does not show up with just an offer. They show up with lender rules, cash-to-close pressure, inspections, underwriting, and a long list of expenses on their side of the table.

That matters to you because buyer costs often turn into seller requests.

The buyer's costs create pressure fast

In a traditional North Carolina sale, buyers commonly pay for loan fees, appraisal, inspections, title charges, homeowner's insurance, and prepaid escrow items. Some of those bills hit before closing. Others are due at the closing table.

That cash requirement is why buyers ask for help so often, especially first-time buyers, military families trying to time a PCS move, and households already stretching to cover a down payment.

Here are the charges that usually drive those conversations:

- Lender fees: Processing, underwriting, and other mortgage charges.

- Appraisal and inspections: The buyer pays to confirm value and condition.

- Title and closing charges: Costs tied to ownership records and lender protection.

- Prepaid items: Insurance premiums and escrow deposits that must be funded up front.

None of that makes the buyer unreasonable. It does mean their budget can tighten quickly.

What sellers in Cumberland County should pay attention to

If your property is clean, updated, and easy to finance, a buyer asking for closing cost help may be nothing more than a routine negotiation.

If the house has deferred maintenance, tenant issues, title problems, or occupancy complications, the buyer's side gets harder. The lender may raise concerns. The appraisal may come in soft. The inspection report may trigger repair requests. Then the buyer asks for seller-paid closing costs on top of everything else.

This process often wears down sellers in rough situations.

That pressure hits hardest in Cumberland County sellers with the least room for delay. A service member leaving Fort Liberty on orders may not have time for another round of paperwork. An out-of-state heir may not want to manage contractors, inspections, and lender conditions from several states away. A distressed owner in Fayetteville may need the sale proceeds to solve a problem now, not after weeks of back-and-forth.

Implications for Sellers in Difficult Situations

You should treat buyer closing costs as part of the full deal, not as a small side issue. A strong offer with heavy concession requests can leave you with less than a lower, cleaner offer.

That is why cash matters. A direct buyer usually removes the lender, cuts out many buyer-side costs that trigger negotiations, and reduces the odds of last-minute concessions. If you want the plain version, read this explanation of what a cash offer on a house means.

Seller perspective: A financed buyer adds more than purchase money. They add another approval process, more conditions, and more chances for the numbers to change before closing.

If certainty matters more than squeezing for a higher contract price, keep that front and center.

Exceptions and Curveballs Closing Costs in Special Situations

Standard closings are one thing. Tough sales are another.

In Cumberland County, the sellers who get hurt most by closing-cost confusion are not the people selling a polished house in a calm market. It is the family handling probate from another state. It is the landlord with a damaged rental. It is the military household trying to leave on orders. It is the owner already in default.

A PCS move with no time for surprises

A military family gets orders and needs the house sold fast. They do the normal thing. Clean it up, list it, wait for a financed buyer.

Then the requests start. Repairs. credits. timing changes. lender conditions. Even when the original deal looks fine, the transaction gets crowded with moving parts. For a family trying to coordinate housing, school, and travel, that uncertainty is often worse than the cost itself.

An inherited house with old problems attached

An out-of-state heir inherits a Fayetteville property. The house has deferred maintenance, old personal property inside, and paperwork nobody has touched in years.

Sellers often get blindsided at this stage. The issue is not just normal closing costs. The issue is whether the title is clean, whether unpaid items exist, and whether the buyer will stay in the deal once the file gets messy.

A foreclosure or short sale can break the normal rules

For distressed properties in Southeastern NC, including Fayetteville and Hope Mills, foreclosure and short sale closing costs are often unpredictable, because banks may dictate terms and shift costs for unpaid liens or code violations to sellers beyond the standard 1% to 3%, according to Matheson Attorneys’ discussion of who pays for closing costs in North Carolina.

That is the key point. In a distressed sale, the normal script can stop applying.

A bank can impose terms. A lien can surface late. A city issue can delay closing. A buyer can use every one of those problems to renegotiate.

What changes in these sales

In special situations, these are the usual pressure points:

- Liens and code issues: They can become seller problems before the sale can close.

- Bank control: In foreclosure-related deals, the lender’s requirements can override expectations.

- Remote ownership: Out-of-state sellers struggle because every document, repair, and decision takes longer.

- Condition problems: Distressed houses trigger more scrutiny in traditional sales.

My advice if you are in one of these situations

Do not judge your sale by “typical” closing-cost articles alone.

Those articles assume a normal transaction. A distressed Cumberland County property is not normal. If there is foreclosure pressure, inherited title confusion, code enforcement, or serious repairs, ask one hard question first: “Can this sale become more expensive after I accept the offer?”

If the answer is yes, certainty matters more than theory.

Negotiating Closing Costs in a Traditional Sale

Yes, closing costs are negotiable in many traditional deals.

No, that does not mean negotiation will help you.

That is the part sellers need to hear more often.

Seller concessions are real, but they cost you

A concession is when the seller agrees to cover some of the buyer’s costs to keep the deal alive or make the offer more attractive.

This can work if your house is clean, the market is strong, and you have options. It works a lot less well when you are selling from a weak position.

If you are behind on payments, dealing with damage, or trying to move fast, the buyer usually knows it. Once they know it, the negotiation changes.

Sellers with urgent timelines have less negotiating power

A buyer can smell urgency.

If you need to sell before foreclosure gets worse, before a court deadline, before a deployment-related move, or before another mortgage payment hits, your negotiating power shrinks. The buyer may ask for credits, repairs, or extra time because they believe you cannot afford to walk away.

That is not personal. It is how deals work.

A simple decision filter

Use this test before agreeing to concessions:

| Situation | Traditional negotiation risk |

|---|---|

| Updated home, no pressure, easy financing | Lower |

| Inherited home, remote owner, outdated condition | Higher |

| Foreclosure pressure or missed payments | High |

| Tenant damage, code issues, major repairs | High |

| Tight military relocation timeline | High |

If your sale falls into the higher-risk side of that table, do not assume negotiating is harmless. Every concession reduces your net. Every delay creates more room for new demands.

Straight advice: If you already need speed and certainty, a deal that depends on ongoing negotiation is usually the wrong deal.

The hidden cost is not always a fee

Sellers focus on line items. They should also focus on friction.

A traditional sale can cost you through delay, re-inspection, repair requests, financing fallout, and renegotiation after you are emotionally committed. Those costs may not appear neatly on the first page, but they still come out of your pocket one way or another.

The Cumberland County Solution Avoiding Closing Costs

Most advice about who pays closing costs in north carolina assumes you want the traditional path.

List it. Clean it. Show it. Negotiate. Wait. Hope the buyer’s financing holds together. Hope no new issue shows up before closing.

That path works for some houses. It is a poor fit for many Cumberland County sellers.

When the traditional model stops making sense

If you are selling from out of state, dealing with probate, trying to stop a foreclosure, or moving because of military orders, the usual process creates too many chances for the deal to go sideways.

The problems stack up fast:

- Commissions reduce your net

- Seller closing costs still apply

- Repairs and credits can grow after inspection

- Remote coordination slows everything down

- Financed deals create more failure points

A direct cash sale strips a lot of that out.

What sellers are really buying with a simple sale

The value is not just speed. It is fewer decisions and fewer points of failure.

You are not managing showings. You are not arguing over repair requests. You are not waiting on underwriting. You are not gambling on a buyer who still has to satisfy a lender.

For many distressed sellers, that simplicity is more important than squeezing for a number that may never survive to the closing table.

Here is a quick overview from a local buyer perspective:

My recommendation for Fayetteville-area sellers

If your house is straightforward and you have time, compare both routes.

If your house is distressed, inherited, vacant, tenant-occupied, tied to liens, or you need to sell from outside North Carolina, lean toward certainty. In those cases, avoiding commissions, avoiding repair negotiations, and avoiding seller-paid process headaches usually matters more than chasing a best-case list price that may never become a real check.

That is especially true in Cumberland County, where military moves, absentee ownership, and problem properties are common enough that speed and clarity are not luxuries. They are practical needs.

Frequently Asked Questions About NC Closing Costs

Do I still pay closing costs if my mortgage is paid off

Yes. Paying off your mortgage does not erase normal seller closing costs. It removes the mortgage payoff from the transaction. You can still face transfer tax, attorney-related seller charges, prorations, and any negotiated credits.

Are seller closing costs paid upfront

Usually, many seller costs are deducted from your proceeds at closing instead of being paid out of pocket beforehand. That helps cash flow, but it still lowers what you take home.

Can closing costs change in a distressed sale

Yes. Distressed sales can become less predictable because liens, code issues, and lender-imposed terms can alter the normal cost structure. That is one reason these sales need a tighter review before you sign.

Can a buyer ask me to pay some of their costs

Yes. In a traditional sale, buyers often ask for concessions. You do not have to agree. Whether you should depends on your negotiating position, your timeline, and the condition of the property.

If you need to sell a house in Fayetteville, Hope Mills, Spring Lake, Raeford, Dunn, or nearby areas and you want a simple way out, DIL Group Buyers is built for exactly that. They buy houses as-is, handle difficult situations like foreclosure, liens, inherited properties, bad tenants, and military PCS moves, and keep the process straightforward for local and out-of-state owners. You can reach out for a cash offer, pick a closing date that works for you, and skip the usual listing stress, repair demands, and back-and-forth.