The call usually comes when life is already sideways. A missed mortgage payment turns into a stack of notices. A tenant leaves the house trashed and stops answering. A sibling inherits a property in Cumberland County and nobody wants to manage the cleanup from another state. A military family gets PCS orders and suddenly has a house to deal with on a deadline.

That is a common point where individuals start looking up we buy houses charlotte. Not because selling for cash sounds trendy, but because they need a clean answer to a messy problem.

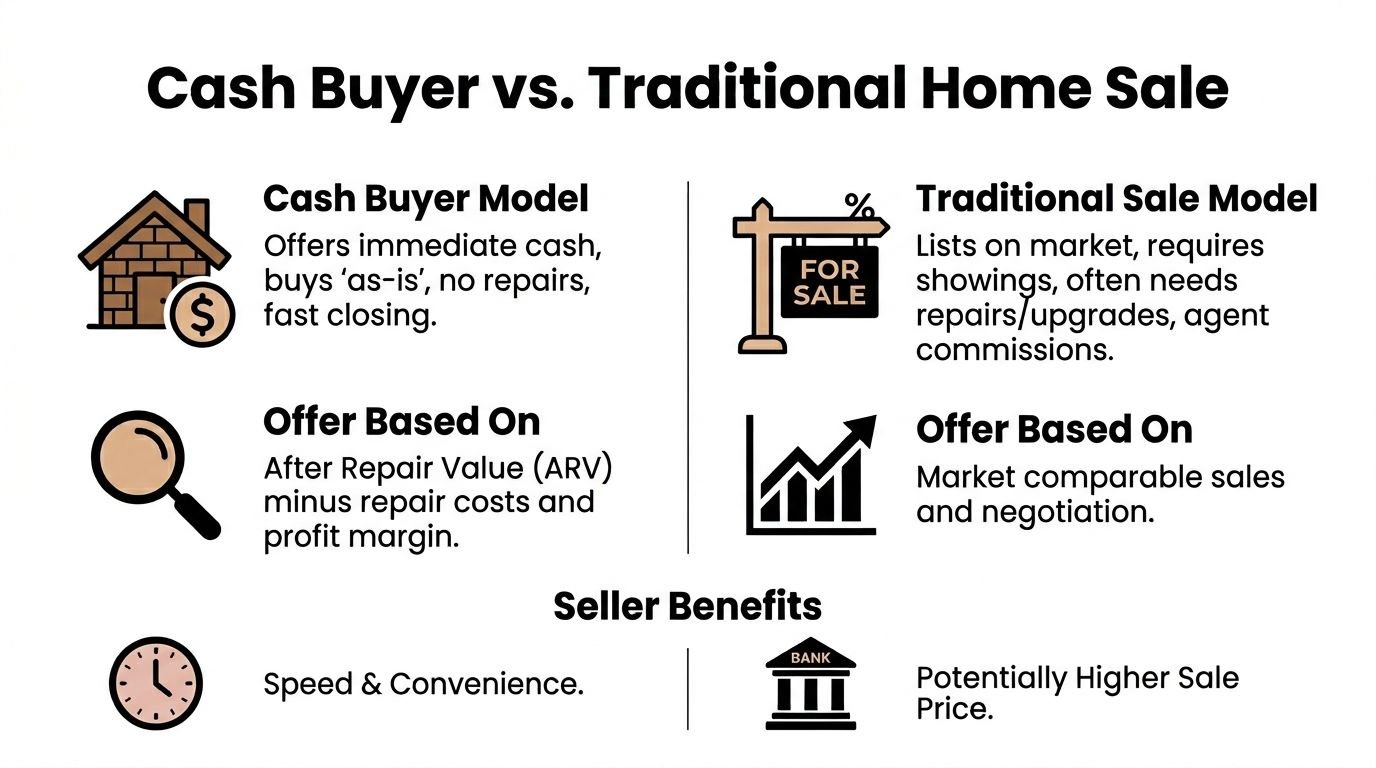

In this part of North Carolina, that need did not come out of nowhere. In Charlotte, the market conditions that made cash buyers more relevant were already visible years ago. In 2018, the typical Charlotte buyer was 49 years old, had a median income of $93,600, and 78% of purchases were for previously owned homes, according to the Charlotte home buyers and sellers report. Sellers with houses that needed work, or sellers who needed speed more than retail exposure, were often at a disadvantage.

Is Selling Your Charlotte House for Cash Right for You

A cash sale makes sense when the main problem is not marketing. It is time, condition, certainty, or stress.

If your house is clean, updated, vacant, and you have room to wait through showings and negotiation, listing on the open market may be the better path. If the property has major deferred maintenance, title issues to sort through, family conflict, bad tenants, or a hard deadline, a direct sale becomes a practical option fast.

The sellers who usually benefit most

Some situations show up again and again in Charlotte, Fayetteville, Hope Mills, Spring Lake, and the surrounding area.

- Behind on payments: You need a firm closing date more than you need a bidding war.

- Inherited property: You do not want to clean out years of belongings, make repairs, and manage contractors.

- Absentee ownership: You live in another city or state and cannot keep driving back for appointments.

- Military relocation: PCS orders do not care whether the roof leaks or the house is show-ready.

- Landlord fatigue: The property may still have tenants, damage, code issues, or unpaid utility balances.

What you give up and what you get

Here is the key trade-off. A cash buyer is not paying for your house the same way a retail buyer does. A retail buyer is often shopping for a finished home they can move into. A cash investor is buying a project, a problem, or a timeline.

In exchange for that lower top-line offer, the seller usually gets:

- No repair work

- No open houses or repeated showings

- No agent commissions in the usual sense

- No waiting on buyer financing

- A closing date built around the seller’s situation

A cash sale is usually strongest when certainty matters more than squeezing out the last possible dollar.

A simple way to decide

Ask one question first. What is causing the pain right now?

If the answer is “I want the absolute highest price,” a traditional listing is worth serious consideration.

If the answer is “I need this handled without fixing it, cleaning it, or waiting around,” then a cash offer deserves a close look. That is especially true for people dealing with foreclosure pressure, inherited houses, remote ownership, or a job or military move that does not leave room for delays.

How We Buy Houses Companies Work

Most sellers hear “cash buyer” and assume it means somebody glances at the house and throws out a random number. A genuine investor typically works backward from the property’s likely value after repairs, then subtracts repairs, holding costs, and the margin needed to make the deal work. There is a method behind the offer.

The basic cash buying process

A typical direct-sale process looks like this:

- Initial contact

You call, text, or fill out a form. The buyer asks about the property, condition, occupancy, timeline, and known issues. - Property review

The buyer looks at photos, public records, comparable sales, and the likely scope of repairs. In some cases the walkthrough is in person. In remote sales it may be virtual. - Offer calculation

A genuine investor typically works backward from the property’s likely value after repairs, then subtracts repairs, holding costs, and the margin needed to make the deal work. - Contract and closing setup

If the seller accepts, the buyer sends a purchase agreement and opens the file with a North Carolina closing attorney. - Title work and closing

Liens, payoff amounts, deed issues, and other paperwork get cleared up. Then the sale closes on the agreed date.

What ARV means in plain English

You will hear the term ARV, or After Repair Value. That means what the house could reasonably sell for after the needed work is done.

Professional cash buyers often use the 70% rule. They estimate the ARV, take about 70% of that amount, and then subtract repair costs. One example used in Charlotte investing is a house with a $300,000 ARV and $50,000 in repairs, which points to a maximum offer of about $160,000. That same Charlotte investing guidance also notes that overestimating ARV is a major mistake and says 32% of flips fail when investors misjudge value or comps, according to this Charlotte house flipping analysis.

That formula helps sellers in two ways. It shows why investor offers are lower than cleaned-up retail prices, and it gives you a way to test whether an offer is grounded in reality.

Cash sale versus MLS sale

A direct cash sale is not “better” in every case. It solves a different problem than a traditional listing.

| Factor | Traditional MLS Listing | Cash Sale (e.g., DIL Group Buyers) |

|—|—|

| Home condition | Usually benefits from repairs, cleanup, and prep | Bought as-is |

| Showings | Multiple showings and buyer traffic are common | Usually limited to one walkthrough or virtual review |

| Financing risk | Buyer loan approval can affect closing | No lender approval in the usual sense |

| Timeline | Depends on market response, inspections, and financing | Built around a shorter, more controlled closing |

| Seller costs | May include commissions, repair requests, concessions, and carrying costs | Often structured to reduce seller effort and out-of-pocket costs |

| Best fit | Sellers maximizing market exposure | Sellers prioritizing speed, certainty, and simplicity |

Why this matters more in a slower market

In a fast market, almost any house gets attention. In a more balanced market, rough houses sit longer and sellers face more second-guessing.

By mid-2025, Charlotte had active listings above 5,300, average days on market had stretched to 32 days, and 33.4% of homes were seeing price drops, according to this Charlotte buyers market update. That does not mean traditional selling stopped working. It means uncertainty grew.

For a seller with a deadline, uncertainty is expensive. Extra mortgage payments, utility bills, cleanup, lawn service, and repair surprises add up quickly.

The strongest cash buyers are not selling speed alone. They are selling fewer moving parts.

What works and what does not

What works:

- Asking how the buyer arrived at the number

- Getting the exact closing terms in writing

- Comparing the net result, not just the gross offer

- Reviewing how companies that buy houses for cash structure deals at this overview of cash-buying companies

What does not:

- Focusing only on the highest first number

- Assuming every “cash” company is the buyer

- Ignoring title, lien, or occupancy issues until late in the process

Identifying and Engaging Legitimate Charlotte Buyers

Some buyers are real operators with local knowledge and funds to close. Others are marketers who put houses under contract and then try to assign the deal to someone else. That is not automatically wrong, but sellers need to know which kind of company they are dealing with.

A legitimate buyer should be easy to verify. If you cannot figure out who they are, where they operate, and how they close, slow the process down.

Green flags that matter

Look for signals that show the buyer is organized, local, and prepared.

- Clear local presence: A real phone number, a real service area, and language that reflects Charlotte, Cumberland County, Fayetteville, Hope Mills, Spring Lake, and nearby communities.

- Straight answers: They explain their process without dancing around repairs, liens, tenants, or probate.

- Proof of funds: If requested, they can show that they have the ability to close.

- Real closing process: They mention the closing attorney, title work, payoff requests, and document signing.

- Consistent communication: They return calls and emails without changing the story every time.

Red flags sellers miss

The biggest warning signs usually show up early.

They avoid specifics

If you ask how they price offers and the answer is all sales language, be careful. A serious buyer should be able to discuss local comps, repairs, resale strategy, and the reason your property fits their model.

They rush you before due diligence

A professional can move fast without being sloppy. Pressure tactics are different. If someone demands an immediate signature before you understand the terms, pause.

They cannot explain the closing path

In North Carolina, the deal runs through an attorney-led closing. If a buyer talks vaguely about “their office handling everything” but cannot explain title work and attorney coordination, that is a problem.

Questions worth asking on the first call

You do not need to interrogate anyone. Just ask practical questions.

- Are you buying this property yourself or assigning the contract?

- How do you decide your offer amount?

- Who handles closing in North Carolina?

- Do you buy tenant-occupied, inherited, or lien-heavy houses?

- Can I choose the closing date?

- Will I need to clean out the house first?

- What could cause your offer to change later?

Those answers tell you a lot. Good buyers do not mind them.

If a buyer gets irritated by basic due-diligence questions, that is useful information. Better to find out on day one than the day before closing.

Local knowledge matters more than most sellers think

A buyer who knows this region will understand the difference between a straightforward suburban resale and a rough inherited house in a pocket where condition changes street by street. They will know that remote sellers often need mobile notary options, attorney coordination, and help handling utility shutoffs or municipal notices without being physically present.

That is also why broad national scripts can fall flat. A seller in Ballantyne has different concerns than an absentee owner dealing with a distressed rental near Fayetteville. The process may look similar on paper, but the obstacles are not the same.

A practical vetting checklist

Before signing anything, confirm these items:

- Company identity: Full business name and contact information

- Purchase method: Direct buyer or wholesaler

- Earnest money: Whether the contract includes it and how it is handled

- Inspection terms: Whether they plan one walkthrough or broad open-ended access

- Closing attorney: Name of the attorney or process for selecting one

- Seller obligations: Cleanout, occupancy, utilities, and personal property terms

- Cancellation language: What lets either side back out

Sellers get into trouble when they rely on vibes instead of documents. Friendly matters. Clear matters more.

Deciphering and Comparing Your Cash Offers

A seller in Charlotte gets three cash offers on Monday. One is the highest. By Friday, that same buyer is asking for a price cut after a long inspection, wants the house emptied, and cannot give a firm closing date. The best-looking number can turn into the weakest deal fast.

Cash offers need to be judged on net proceeds, contract strength, and how much work stays on your plate. That matters even more for sellers dealing with a military move, an inherited property, or a rental house in Cumberland County that has been hard to manage from out of town.

Start with how the buyer reached the number

A real buyer should be able to explain the offer in plain English. Usually that means discussing the home’s after-repair value, the condition issues that affect resale, the cost of repairs, holding costs, and the margin they need for the deal to make sense.

If they cannot explain their math, the offer is harder to trust.

Sellers who want a clearer sense of how investors usually calculate offers can review this breakdown of cash offer math. You do not need to agree with every formula. You do need to know whether the buyer is using a consistent method or just throwing out a low number to test your urgency.

In Charlotte and nearby markets, the same square footage can produce very different offer ranges based on location, layout, deferred maintenance, and resale demand. The gap gets wider with older houses, inherited homes, and rentals that have been patched over for years. A house near Pineville with mostly cosmetic work is priced differently than a vacant property near Fayetteville with roof issues, old HVAC, and city notices.

Compare what you keep

Put every offer on one page and compare the terms line by line.

| Item to compare | What to check |

|---|---|

| Offer amount | The contract price before any deductions |

| Closing costs | Which costs the buyer is paying and which are still yours |

| Earnest money | Whether the buyer put up a meaningful deposit |

| Repair credits | Whether they can ask for a discount later |

| Property condition | Whether the sale is as-is |

| Cleanout | Whether you can leave unwanted furniture, trash, or tenant items |

| Closing timeline | Whether the date works for your move, probate schedule, or tenant situation |

| Post-closing possession | Whether you get extra time in the house after closing if needed |

That side-by-side review often shows the best option.

A lower offer can still leave you with more money and fewer problems if the buyer covers closing costs, buys as-is, handles the cleanout, and closes on the date you need. I see this often with absentee landlords and Fort Bragg PCS sellers. The sale price matters, but so does avoiding another month of mortgage payments, utilities, vacancy, travel, or contractor coordination.

Watch for terms that create room for a retrade

The weak point in many cash offers is not the number. It is the contract language that lets the buyer come back later and chip away at it.

Pay close attention to these problem areas:

- Open-ended inspection periods that give the buyer too much time to look for reasons to renegotiate

- Vague as-is language that sounds clean but still leaves room for repair demands

- No clear cleanout terms if the house has leftover belongings, old appliances, or tenant debris

- Tiny or missing earnest money which can signal a buyer with little commitment

- Loose assignment language if you thought you were dealing with a direct buyer

- Unclear closing dates that depend on the buyer finding funds or another end buyer

Sellers often lose ground at this stage. A contract can say cash and still be full of exits.

A practical way to separate strong offers from weak ones

Ask each buyer four direct questions and write down the answers:

- What is my net amount at closing after all fees and credits?

- What, if anything, do I need to remove or repair before closing?

- What can cause you to cancel or lower the price?

- Who is handling the closing, and how soon can we get on the attorney’s calendar?

Serious buyers answer quickly and specifically. Weak buyers stay general.

For military families working under hard move dates, or heirs trying to sell a house from another state, certainty often matters more than squeezing out the last few thousand dollars. The right offer solves the problem in front of you. It gives you a clear closing date, fewer obligations, and fewer chances for the deal to change after you sign.

From Offer Acceptance to Closing Day in NC

Once you sign, most sellers want one thing. A predictable path from contract to money in the bank.

North Carolina closings are attorney-driven, which is good for sellers because there is a formal process to follow and a closing professional overseeing the paperwork.

What happens right after you accept

After the contract is signed, the buyer usually sends it to the closing attorney. The attorney’s office then begins collecting the documents needed to transfer ownership cleanly.

That usually includes:

- the signed purchase agreement

- title search work

- mortgage payoff information if there is a loan

- lien and judgment review

- deed preparation

- final closing figures

For sellers, this stage is mostly about responding quickly when the attorney requests documents or signatures.

The attorney’s role in North Carolina

In NC, the closing attorney is central to the deal. That office handles title review, prepares the legal paperwork, receives funds, and coordinates the actual closing.

If there is a problem, this is often where it surfaces. Common examples include old liens, estate issues, unreleased deeds of trust, or name mismatches on title documents.

A clean cash deal feels easy because the legal work is being handled correctly behind the scenes.

Typical issues that slow closings

Not every delay comes from the buyer. Often the title file reveals a problem the seller did not know existed.

Liens and judgments

Tax liens, contractor claims, old utility balances, and court judgments can all attach to the property or seller. These need to be addressed before transfer.

Probate and inherited ownership

If the property came through an estate, the attorney may need letters, death certificates, probate filings, or signatures from multiple heirs.

Tenant occupancy

If there are tenants in place, the contract needs to spell out whether the buyer is taking the property occupied or whether possession must be delivered vacant.

Here is a useful overview of the closing flow:

What sellers should prepare

You do not need to overcomplicate this. Gather the basics early.

- Photo ID: Current and valid

- Mortgage info: Latest statement if the property has a loan

- HOA details: If the property is in an association

- Estate paperwork: If inherited

- Lease documents: If tenants are involved

- Utility or code notices: If there are open violations

Remote closings are common

Sellers often assume they must appear in person. Many do not. If you are out of town or out of state, the attorney can often coordinate mail-away documents, remote notarization where appropriate, or signing through a local notary.

That matters for military families, inherited property owners, and landlords who no longer live near the house.

What closing day looks like

Closing day is usually straightforward. The attorney confirms signed documents, receives the buyer’s funds, pays off any liens or mortgage balances that must be cleared, records the deed, and then disburses the seller’s proceeds.

For the seller, the practical questions are simple:

- Have I signed everything?

- Have I removed what I want to keep?

- Do I know when funds will be sent?

- Have I confirmed utility handling and possession terms?

If those boxes are checked, closing day tends to be calm.

Essential Advice for Military, Inherited, and Out-of-State Sales

Generic cash-buyer content often fails people in this area. It talks about “fast closings” in broad terms and skips the headaches that show up in real sales.

In this region, those headaches often involve military relocation, inherited property, remote ownership, or foreclosure pressure. Each one needs a slightly different approach.

Military PCS moves near Fort Bragg

PCS moves create a deadline that does not bend. If the house needs work or the owner has already moved, the traditional listing route can turn into a long-distance project nobody wants.

The biggest advantage of a cash sale in a PCS situation is not just speed. It is the ability to set a dependable closing date and sell the property in its current condition.

A military seller should focus on these points:

- Certainty of close: Ask whether the buyer can perform on your timeline.

- Remote document handling: Confirm how the attorney will coordinate signatures if you have already reported elsewhere.

- Personal property terms: Make sure the contract addresses what can remain in the house.

- Occupancy details: If family is still in the property, align move-out timing with orders.

Out-of-state owners need a different process

This is one of the most overlooked seller categories. Many absentee owners are dealing with problem houses from a distance, and general articles barely address the logistics.

Guidance for remote owners matters because many sellers in the Cumberland County area are absentee owners or military families selling from afar. Those situations often require virtual walkthroughs and remote closings handled through a power of attorney, according to this discussion of remote seller needs in the Charlotte cash-buying market.

That means a practical buyer should be ready to work through:

- video walkthroughs

- photo documentation

- lockbox or access coordination

- attorney communication by phone and email

- power of attorney when appropriate

- lien or violation research without requiring the owner to travel back

If you are selling from another state, the right question is not “Can this be done remotely?” It is “Who is coordinating each remote step so nothing stalls?”

Inherited houses need clarity more than speed

Families often think the biggest issue is the property condition. Usually it is not. The bigger issue is getting everyone aligned.

Inherited houses create decision friction. One heir wants to list. Another wants to keep it. A third does not want to spend money on cleanup. Meanwhile the grass is growing, the taxes are still due, and the property may be sitting vacant.

A direct cash sale can help when the heirs agree that liquidation is the cleanest outcome. It avoids repair debates and turns the property into cash that can be divided according to the estate process.

If probate is involved, get the legal authority confirmed early. If you need help understanding the process around inherited real estate, this overview of probate property sales in North Carolina gives a useful starting point.

Landlords with bad tenants need contract precision

Rental property sales are never just about price. They are about possession, damage, lease status, and whether the seller wants to keep managing the problem while the property is marketed.

For landlords, the strongest cash deals usually share a few traits:

- the buyer is willing to review the lease and rent history

- the buyer states clearly whether they will buy with tenants in place

- the contract addresses any remaining personal property

- the seller is not asked to renovate a house they are already tired of managing

This matters even more when the owner lives elsewhere. A local issue becomes much bigger when every contractor call, inspection, and cleanup decision has to happen across state lines.

Foreclosure pressure changes the decision

When foreclosure is a real possibility, time matters more than theory.

For homeowners facing foreclosure in Mecklenburg or Cumberland Counties, a cash sale can prevent the 7-year credit damage tied to foreclosure, preserve any remaining equity, and help landlords avoid major eviction-related expenses, according to this foreclosure-focused Charlotte cash sale guide.

That is why sellers behind on payments should stop thinking in terms of “perfect deal” and start thinking in terms of “workable timeline.”

A few practical moves help:

- Open every lender notice

Sellers lose time by avoiding the mail. - Request payoff information early

Your closing attorney and buyer need accurate numbers. - Disclose any bankruptcy, lien, or court issue up front

Hidden problems do not disappear. They delay closings. - Choose buyers who understand distressed timelines

Not every buyer is built for foreclosure situations.

What works best in these special cases

Across military moves, inherited homes, and out-of-state ownership, the pattern is the same. The winning process is organized, document-heavy, and calm.

The losing process is vague. It depends on “we’ll figure it out later,” which usually means delays, renegotiation, or extra stress.

If your situation is unusual, that is not a reason to avoid a cash sale. It is a reason to make sure the buyer and attorney can handle the details that a generic script ignores.

Making Your Final Decision with Confidence

A final decision usually comes down to fit, not pitch.

In Charlotte, Fayetteville, and the smaller Cumberland County communities around them, I have seen sellers get stuck because they keep comparing selling paths as if every house has the same timeline and the same risk. They do not. A clean ranch in a stable neighborhood, with no title issues and no tenant problems, deserves a different decision process than a rental with deferred maintenance, an inherited house with several heirs, or a PCS move that gives you a narrow window to get the property off your plate.

The right question is simple: which option gives you the best outcome for your situation, after costs, delays, and stress are fully considered?

For some owners, that is listing with an agent. For others, a cash offer is the practical choice because it removes repairs, showings, buyer financing risk, and a long back-and-forth over inspection items.

Before you sign anything, make one last comparison on paper. Write down the expected sale price, repair cost, holding cost, closing timeline, and the chance the deal falls apart. That exercise clears up a lot of confusion. Sellers dealing with out-of-state ownership, military relocation orders, or inherited property usually benefit from certainty more than from chasing a higher number that may never make it to the closing table.

Confidence comes from clear terms.

If the buyer explained the process plainly, gave you enough time to review the contract, and answered hard questions about title work, proof of funds, closing costs, and possession, you are probably dealing with a serious operator. If the offer still feels vague at the end, keep looking.

If you need a practical, no-pressure cash offer in Cumberland County or nearby communities, DIL Group Buyers is a local option worth considering. They buy houses as-is, work with inherited properties, foreclosure situations, military PCS moves, bad tenants, and out-of-state owners, and they can walk you through a straightforward closing timeline without commissions, repairs, or hidden costs.