Yes, you can absolutely sell your house while it's in foreclosure.

Your Options When Facing Foreclosure in Fayetteville

If you're facing foreclosure, it’s easy to feel backed into a corner. But I want you to know you have more control than you think. You have options right here in Fayetteville and Cumberland County, and selling your house is often the smartest move you can make to protect your finances and get back on your feet.

You don't have to go through this alone. The most important thing is to act before the bank finalizes the foreclosure process. Let's look at the paths you can take:

- Loan Modification: You can try to work with your lender to change your mortgage terms. This might lower your payments, but it's not always approved.

- Short Sale: This involves selling your home for less than you owe, but you'll need the lender's permission, and it can be a long, complicated process.

- Deed in Lieu of Foreclosure: Here, you voluntarily hand the property title over to the lender to avoid foreclosure.

- Cash Sale: This is where you sell your property fast to a local cash buyer, usually "as-is," with no repairs needed.

Don't Wait—Take Action Now

The minute you get that notice of default, the clock starts ticking. The absolute worst thing you can do is ignore it. That path leads straight to a public auction and removes all your choices. By taking action now, you stay in the driver's seat. You get to manage the outcome and minimize the damage to your credit.

This is more urgent now than ever. Foreclosure filings have shot up nationwide, seeing a massive 57 percent increase compared to last year. Economic pressures are hitting homeowners hard. This isn't just a statistic; it's a reality for many families, and it shows why exploring every alternative—especially a quick cash sale—is so critical. You can explore the data behind these national foreclosure trends to see how the landscape is changing.

Your biggest advantage right now is time. North Carolina's pre-foreclosure period is your window of opportunity. You still own the property, and you can legally sell it, pay off the lender, and stop the foreclosure completely.

Why Selling Can Be Your Best Move

Selling your house before the auction isn't just about avoiding a worst-case scenario; it's about protecting your future. When you sell, you satisfy the debt with your lender. This is far better for your credit than a foreclosure, which can haunt your financial record for seven long years.

Selling also means you control the process. You negotiate the price and the timeline. At an auction, you have zero say. And if you have any equity built up in your home, selling is the only way you might get to walk away with that cash.

For many homeowners here in Fayetteville, a fast, no-fee cash sale provides the clearest path to resolving the situation with certainty and dignity. You can also review our detailed guide on how to stop foreclosure on my home for more in-depth strategies.

Navigating the North Carolina Foreclosure Timeline

When you're trying to stop a foreclosure in North Carolina, time is everything. It's not just a single event; it's a process with distinct phases. Understanding exactly where you stand in that process is the key to taking back control. It allows you to make smart, proactive decisions—like selling your house—instead of just reacting to what the bank does next.

The whole thing usually starts quietly, with a letter. After a few missed mortgage payments, your lender will send out a Notice of Default. This is the first official warning shot. Seeing that letter can be terrifying, but it's not the end of the road. It’s simply the starting gun, and it means the clock is now officially ticking.

This letter kicks off what we call the pre-foreclosure period. Honestly, this is the most important window of time you have. During this stage, which can last anywhere from 30 to 120 days, the house is still yours. You hold the title, and you have the legal right to sell it, refinance, or work out a deal with your lender. It's your single best opportunity to sell the house on your terms.

The Pre-Foreclosure Window: Your Chance to Act

Think of pre-foreclosure as the grace period you have to find a real solution before the problem gets out of hand. For any homeowner here in Cumberland County, this is your time to list the property, find an investor, or explore other options. The absolute worst thing you can do is ignore the notices. Once this window closes, your options shrink dramatically.

This is often an emotional rollercoaster, but knowing the steps can help you feel less overwhelmed and more in control.

The takeaway here is simple: information empowers you to act, and action is what puts you back in the driver's seat.

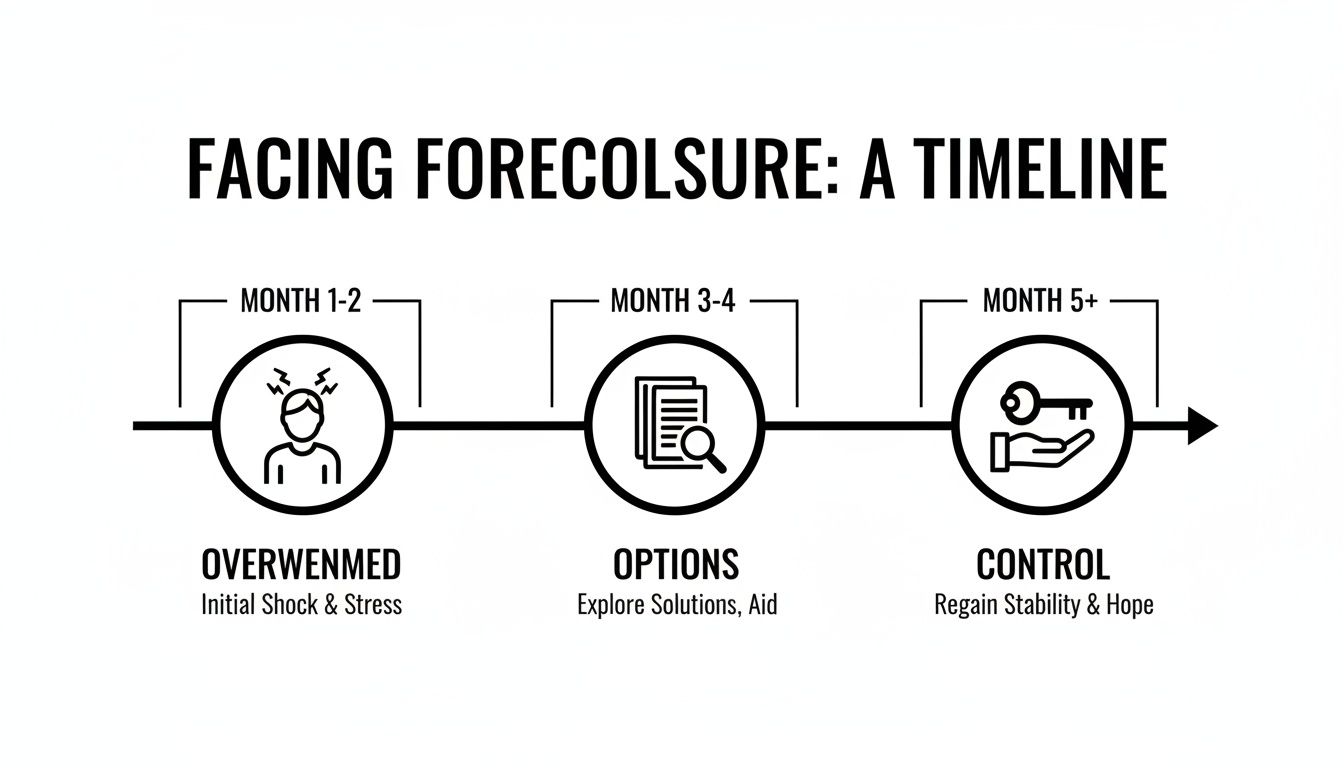

Let's look at a real-world example. Imagine a homeowner in Fayetteville we'll call Sarah. She gets a Notice of Default and knows she has about 90 days to figure things out.

- Month 1: Sarah calls her lender to get the exact payoff amount and confirm her deadline. At the same time, she calls a local cash buyer like us for a no-pressure offer, just to see what her baseline number is.

- Month 2: She looks into a loan modification, but it becomes clear it won't be approved quickly enough. That cash offer is now looking like her best bet for a guaranteed, fast closing.

- Month 3: Sarah accepts the offer. We schedule the closing well before the bank can take the next step. She successfully stops the foreclosure, protects her credit, and walks away with cash.

The Notice of Sale and The Public Auction

If you can't find a solution during pre-foreclosure, things escalate. The lender will go to court and get a Notice of Sale. This is a public announcement stating that your home will be sold at a foreclosure auction on a specific date, right here at the county courthouse.

The minute that notice goes up, the pressure is on. You can still sell your house, but the sale must be completely finished before the auction date. This is where a quick cash sale is a lifesaver. A traditional sale, with all its inspections, appraisals, and bank loan approvals, is almost always too slow to beat that deadline.

The foreclosure auction is truly the point of no return. Once your property is sold there, you lose all rights and control. Any equity you had is probably gone, and the hit to your credit is devastating and lasts for years.

What Happens After the Auction?

North Carolina does have what's called an "upset bid period" after the auction. This gives other buyers a 10-day window to come in and place a higher bid on the property. If they do, the 10-day clock starts all over again.

But don't get confused—this is not a redemption period for you, the original homeowner. You can't just show up with the money after the auction and get your house back. Your ability to solve this on your own terms ends the second that gavel falls. That’s why taking decisive action during pre-foreclosure is the only reliable way to get a positive outcome.

Comparing Your Foreclosure Avoidance Strategies

When that foreclosure notice hits, it’s easy to feel like your options have vanished. But that’s just not true. You actually have several different ways to handle this, and each one has its own impact on your credit, timeline, and whether you get to keep your home. The key is to be brutally honest with yourself about your goals and what your finances can realistically support.

Selling your house is a powerful way out, but it’s just one of the tools in the toolbox. Let’s break down the most common strategies so you can see how they stack up against each other.

Can You Work Things Out with Your Lender?

Your first thought might be to call the bank. Sometimes, this works. Lenders often don't want to foreclose—it’s an expensive headache for them, too. They usually have two main lifelines to offer: loan modifications and forbearance agreements.

A loan modification isn’t just a temporary fix; it permanently rewrites the rules of your mortgage. The bank might agree to lower your interest rate, stretch out the loan over more years, or even knock down the principal balance. The whole point is to get your monthly payment to a number you can actually handle.

A forbearance agreement, on the other hand, is like hitting the pause button. Your lender agrees to temporarily reduce or suspend your payments altogether. This is designed for people who've hit a short-term rough patch—like a layoff or a medical emergency—and just need a few months to get back on their feet.

Here’s the catch: You have to get the lender to say yes, and that’s never a sure thing. You’ll be drowning in paperwork, and the approval process can drag on for months. When you've got an auction date breathing down your neck, time is a luxury you just don't have.

Alternatives When Keeping the Home Isn't an Option

If you know staying in the house isn’t in the cards, you still have moves to make before the auction. A short sale or a deed in lieu of foreclosure are two common paths, but both require the lender to play ball.

Short Sale: This is exactly what it sounds like—you sell the house for less than you owe on the mortgage. To do this, you have to prove to the lender that you're in real financial trouble, and they have to agree to take the loss. A short sale will stop the foreclosure, but it’s a marathon, not a sprint. It can easily take 6 to 12 months and it will still wreck your credit.

Deed in Lieu of Foreclosure: With this option, you’re essentially handing the keys back to the bank. You sign over the deed to the property, and in return, the lender cancels your debt. It’s often the last stop before the auction, but you walk away with nothing—no equity, no control.

While these options are better than a full-blown foreclosure, the lender holds all the cards. You’re playing by their rules and on their timeline.

The Power of a Fast Cash Sale

Selling your property directly to a cash buyer like DIL Group is a totally different ballgame. It puts you back in the driver's seat. This path is all about speed, certainty, and control.

Instead of waiting months for a lender’s approval, a cash sale works on your schedule. You get a fair offer, pay off the mortgage, and stop the foreclosure dead in its tracks. It’s a clean break.

This is the go-to solution for homeowners in Cumberland County who need a guaranteed escape before the auction date arrives. You get to skip all the usual real estate headaches—no repairs, no showings, no worrying about a buyer’s loan falling through. You get a firm offer and can close the deal in as little as a week.

While foreclosure filings are up, it’s important to see the whole picture. Nationally, the rate is still below 0.25%, which is a far cry from the last housing crisis. Waiting for the market to save you isn’t a strategy. You can see more data on these national foreclosure rates to understand the broader trends, but what matters is your situation right now. In Fayetteville, a fast, guaranteed cash sale is often the smartest move you can make to protect whatever equity you have and start fresh.

To make it even clearer, here’s a direct comparison of your main choices.

Foreclosure Avoidance Options Head-to-Head

When you're under pressure, it can be tough to weigh the pros and cons of each path. This table cuts through the noise and lays it all out, comparing the options based on the things that matter most: your credit, your timeline, and the final outcome.

| Option | Impact on Credit Score | Typical Timeline | Potential to Keep Home | Best For |

|---|---|---|---|---|

| Loan Modification | Minimal to moderate negative impact. | 3-6 months | High | Homeowners with a temporary setback and a stable income source. |

| Short Sale | Significant negative impact, similar to foreclosure. | 6-12 months | None | Homeowners who are underwater on their mortgage with no equity. |

| Deed in Lieu | Significant negative impact. | 2-4 months | None | Homeowners with no equity who want to avoid a public auction. |

| Cash Sale | Minimal long-term impact beyond missed payments. | 1-4 weeks | None | Homeowners needing a fast, certain exit to protect equity and credit. |

Looking at them side-by-side, it's clear that if your goal is a fast, clean exit that salvages your credit as much as possible, a cash sale offers a level of certainty and control that the other options simply can't match.

How to Sell Your House for Cash and Stop Foreclosure

If you’ve decided selling for cash is your best move to stop foreclosure, here’s your playbook. This isn't just theory—it's a real-world guide to navigating the process right here in Fayetteville with confidence and, most importantly, speed. The whole point is to get you from a place of stress to a successful closing, pay off the bank, and let you move on with your life.

This process is built to be fast because time is a luxury you just don't have. A traditional sale can drag on for months. A cash sale is designed to get you ahead of the auctioneer's gavel.

Let’s walk through what this actually looks like.

Gathering Your Essential Documents

Before you can get a solid cash offer, you need to get your key paperwork together. It's not complicated, but having these items ready makes everything move so much faster. It shows a buyer you’re serious and lets them give you a concrete offer you can actually count on.

Here’s what you’ll want to pull together:

- Your Latest Mortgage Statement: This shows the current balance, interest rate, and exactly how much is past due. A buyer needs this to calculate the precise payoff amount to clear your debt.

- The Notice of Default: This is the official letter from your lender that started the foreclosure clock. It contains critical dates and contact info for their legal department.

- Property Tax Information: A recent property tax bill shows the assessed value and confirms you're the owner.

- HOA Info (if applicable): If you're in an HOA, find any recent statements or contact details. They might have a lien on the property for unpaid dues that needs to be settled.

Having these documents on hand allows a cash buyer like DIL Group Home Buyers to quickly verify the details and present you with a firm offer.

Requesting and Evaluating a No-Obligation Offer

Once your documents are in order, it’s time to ask for an offer. Reputable cash buyers make this part simple. You give them your property address and a few basics about its condition. In many cases, you can get a preliminary offer within 24 hours.

That first offer is a starting point, based on public records and what you've told them. The buyer will then need to schedule a quick, in-person visit to the property to see things for themselves and finalize the numbers.

Key takeaway: A legitimate cash offer is always free and comes with zero obligation. You should never, ever pay a fee to find out what someone is willing to pay for your home. This is your chance to see if the numbers work without any pressure.

When you get the offer, it will likely be less than the "Zestimate" you see online for a perfect, move-in-ready house. That's because a cash offer reflects a few key things:

- The "As-Is" Condition: The price accounts for every single repair needed, whether it's a leaky roof or an ancient kitchen. The buyer takes on the full cost and headache of fixing it all.

- Speed and Convenience: You're paying for certainty and ease. There are no realtor commissions (usually 5-6%), no closing costs for you to pay, and no haggling over seller concessions.

- Holding Costs: The buyer has to factor in the property taxes, insurance, and utilities they'll be paying while they renovate and eventually resell the home.

Negotiating and Closing the Deal Fast

After the quick walkthrough, you'll get a final, written cash offer. This is a real number you can take to the bank. If you like the offer and want to move forward, you’ll sign a straightforward purchase agreement.

This is where the power of a cash sale truly shines. There are no banks on the buyer's side, which means no agonizingly slow appraisal or underwriting process. The buyer has the cash ready to go. You can also get more information about how to sell your home for cash and what to expect.

The closing itself is handled by a local attorney or title company, just like any other real estate deal. They prepare the paperwork, contact your lender for the final payoff amount, and make sure any other liens are cleared.

The best part? You get to pick the closing date. If the auction is in ten days, a professional cash buyer can often close in seven. Need a few weeks to pack and sort things out? They can work with that, too.

On closing day, the title company wires the payoff amount directly to your lender, which officially stops the foreclosure in its tracks. Any money left over—your equity—is then wired straight to your bank account. You walk away with the debt settled, your credit saved from a foreclosure, and a clean slate.

Why a Local Fayetteville Buyer Makes All the Difference

When you're fighting to stop a foreclosure, who you work with can be the single most important decision you make. You'll see plenty of national "we buy houses" companies online, but there's a huge, real-world advantage to partnering with a local Fayetteville buyer—someone who actually lives and invests right here in Cumberland County.

This isn't just about finding any buyer. It's about finding an expert who genuinely gets our local market.

A local buyer knows the neighborhoods, from Hope Mills all the way to Fort Liberty. They understand property values here not from a spreadsheet, but from being on the ground, day in and day out. That deep market knowledge means they can make you a fair, accurate offer fast, without the long delays you get from out-of-state investors who have to do all their research from a distance.

Speed and Certainty That Only Comes From Local Expertise

Think about this real-life scenario: a military family at Fort Liberty gets hit with unexpected PCS (Permanent Change of Station) orders just as they're falling behind on their mortgage. They have to sell now, before the foreclosure process gets any further. A national buyer might drag their feet, unsure about local demand or how much repairs might cost.

A local buyer, on the other hand, already has a team of local contractors, attorneys, and title companies ready to spring into action. They can walk through your property within hours, make a solid cash offer based on what they already know about the area, and close the deal in days. That kind of speed is absolutely essential when you're selling a house in foreclosure and the clock is ticking toward an auction date.

The single biggest advantage a local buyer offers is accountability. You're not just a number in a corporate system or talking to a call center a thousand miles away. You're working with a neighbor—someone you can meet face-to-face who has a reputation to protect right here in our community.

A Straightforward Process with No Hidden Junk Fees

One of the worst parts of selling a house the old way is getting hit with surprise costs. A reputable local cash buyer cuts through all that by being totally transparent from day one.

Here’s what that actually means for your wallet:

- No Realtor Commissions: You keep the 5-6% commission fee. That’s thousands of dollars that stay in your pocket.

- No Seller Closing Costs: A dedicated local buyer covers all closing costs, like attorney fees and title insurance.

- No Repair Credits: The offer you get is for your house exactly as it is. You won’t be asked to shell out money for a new roof or fix the plumbing.

- No Hidden Service Fees: The offer you accept is the cash you get at closing, minus your mortgage payoff. No last-minute deductions, ever.

This no-nonsense approach gives you financial certainty right when you need it most.

Real Solutions for Fayetteville Homeowners

Here’s another situation we see all the time. A landlord in Hope Mills has a rental where the tenants stopped paying and trashed the place. Now he's facing foreclosure on that second mortgage and doesn't have the cash for repairs or a long, expensive eviction.

For him, a local cash buyer is the perfect out. We can buy the house with the problem tenants still inside and take on the entire eviction process ourselves after the sale closes. This lets the landlord walk away fast, pay off the bank, and avoid the credit catastrophe of a foreclosure. A traditional buyer who needs a bank loan could never make that happen.

Working with a company that handles these tough situations is key. To see how we do it, you can learn more about how we buy houses in Fayetteville NC with a simple, no-pressure process.

At the end of the day, choosing a local buyer means choosing a partner who is invested in our community and truly understands the challenges Fayetteville homeowners face. It’s more than a transaction—it’s about finding a fair, fast, and stress-free way forward so you can finally put the threat of foreclosure behind you for good.

Your Top Foreclosure Questions Answered

When you're staring down a foreclosure, your head is probably spinning with a million questions. It’s an overwhelming spot to be in, and getting straight answers is the first real step toward finding your way out. We’ve pulled together the most common questions we hear from Fayetteville homeowners to give you some clarity.

Can I Sell My House if It's Already in Foreclosure?

Yes, absolutely. Here in North Carolina, you have the legal right to sell your home right up until the foreclosure auction is finalized. The whole pre-foreclosure window is designed to give you that chance.

Selling to a cash buyer is usually the fastest, most direct way to pay off what you owe the bank, stop the legal process cold, and avoid the auction completely. The most important thing is to move quickly—that window of opportunity doesn't stay open forever.

Will Selling My Home During Foreclosure Destroy My Credit?

Actually, selling your house before the foreclosure goes through is one of the smartest things you can do to protect your credit. While missed mortgage payments have probably already dinged your score, a full-blown foreclosure is a much bigger financial hit.

A foreclosure can haunt your credit report for seven years. That makes getting loans, new credit cards, or even renting an apartment incredibly tough down the road.

When you sell the house and pay off the loan, you’re taking control and settling the debt yourself. Credit bureaus see that in a much better light than a bank having to repossess your home. A clean cash sale that covers the mortgage can drastically limit the long-term damage to your credit.

What if My House Is in Bad Shape and Needs a Ton of Repairs?

This is a huge worry for a lot of homeowners, and it’s exactly why a cash sale makes so much sense. A legitimate cash buyer, like us at DIL Group, buys properties "as-is." That means you don't have to fix, update, or even clean a single thing.

We look at your home in its current state and make a fair offer based on that reality. All the risk and expense of repairs become our problem after the sale is done. This lets you get out from under the property fast without sinking money you don't have into a house you're about to lose.

How Quickly Can I Get an Offer and Close This Deal?

The whole process is built for speed, which is critical when you're up against a foreclosure deadline. Typically, you can get a no-pressure cash offer within 24 hours after you reach out and give us the details of your property.

If the offer works for you, we can often close the sale in as little as 7 to 14 days. We're flexible and can work around your timeline, too. That kind of speed is what allows you to beat the auction date, pay off the bank, and walk away on your own terms.

Ready to end the stress and get a guaranteed cash offer for your home? The team at DIL Group Home Buyers is here to give you a fast, fair, and respectful solution. Contact us today for your free, no-obligation offer and take that first step toward a fresh start.