Of course. Getting a foreclosure notice feels like the world is closing in, but I'm here to tell you that it's not over. You absolutely have the power to sell your house, even after the foreclosure process has started.

In North Carolina, the law gives you a critical window of time to take back control. This is called the pre-foreclosure period, and it’s your best chance to sell your property, settle the debt with the bank, and walk away without the devastating hit of a public auction on your record. The key is to act decisively and not let the clock run out.

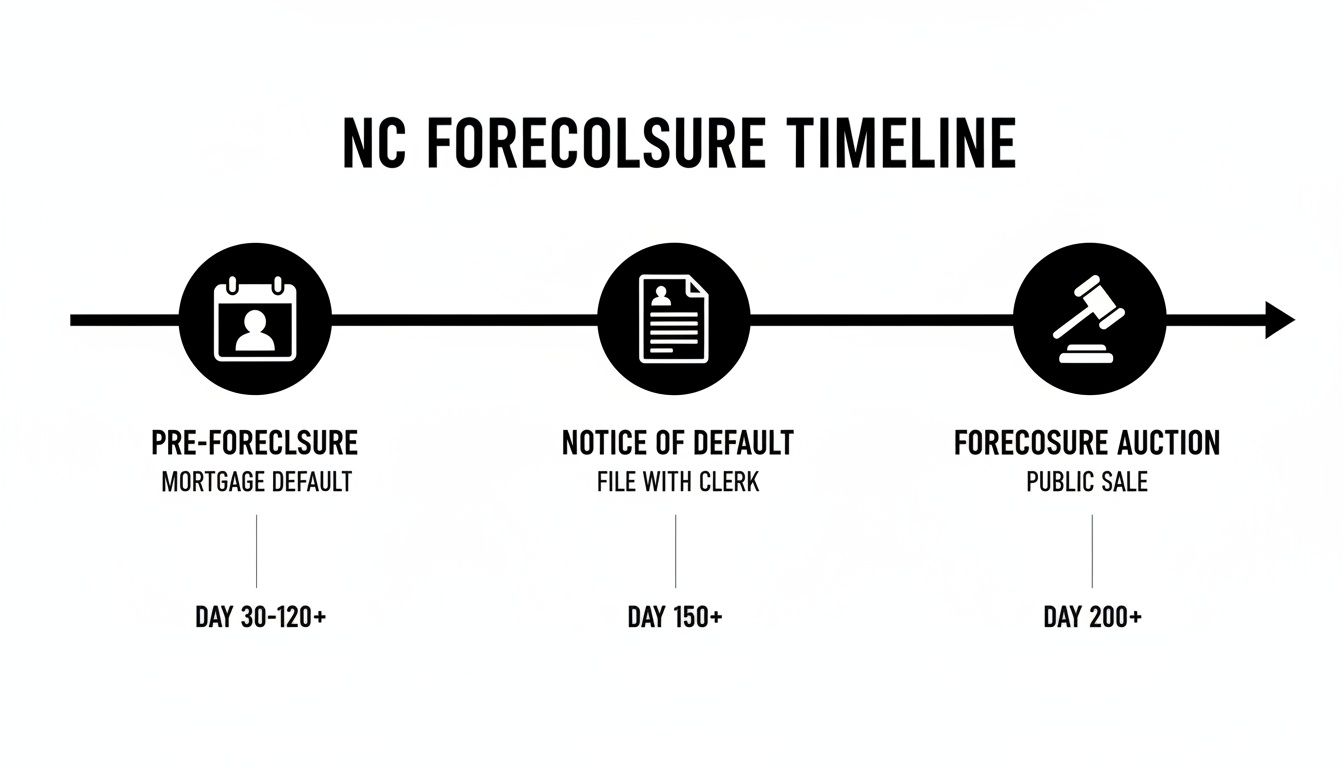

Understanding the North Carolina Foreclosure Timeline

That notice from the bank is designed to be intimidating, making you feel like your time is up. But it’s not an eviction notice. The foreclosure process in North Carolina follows a specific, legally required timeline. It doesn't happen overnight.

Knowing these stages is crucial because it transforms you from someone reacting to bad news into someone making a strategic plan. You have opportunities to get ahead of the situation, but you need to know how the game is played.

Here in North Carolina, most foreclosures are done through a power of sale. This just means the lender can sell the property without a lengthy court battle, as long as that right was included in your original mortgage documents. It’s faster than a judicial foreclosure, which is why understanding the timeline is so important.

The Critical Pre-Foreclosure Period

Before a lender can even start the official foreclosure process, federal law typically requires them to wait until your mortgage is more than 120 days delinquent.

This four-month window is your pre-foreclosure period. It’s not just a countdown to disaster; it is your single biggest opportunity to solve this problem on your own terms.

During these 120 days, you are still the legal owner of your home. You have every right to sell it. This is your prime time to dodge the long-term financial damage a foreclosure leaves behind. Use this period to:

- Get a clear picture: Figure out exactly how much you owe the bank and get a realistic idea of what your house is worth today.

- Look at your real options: Is a traditional market sale possible? Would a short sale work? Or is a fast, no-hassle cash sale your best bet to resolve this quickly?

- Make your move: Don't wait. Contact your lender to let them know your plan and start the process of selling before an official auction date gets slapped on your file.

Your power is at its peak during the pre-foreclosure stage. Once the public notices are filed and an auction date is on the calendar, your options shrink dramatically and the pressure goes way up.

This timeline shows you exactly how things unfold, from the first missed payment all the way to the auction block.

As you can see, the smartest moves—like selling for cash—happen early. The goal is to get this handled long before the auctioneer ever shows up.

When you're facing foreclosure, it can feel like you're cornered. But you're not out of options. The goal is to find a solution that lets you pay off the bank and move on with your life, avoiding the auction entirely.

We've put together a quick comparison to help you see the different paths you can take.

Your Options When Facing Foreclosure in NC

| Option | Typical Timeline | Impact on Credit | Best For |

|---|---|---|---|

| Sell for Cash | 7-21 days | Minimal impact; can prevent foreclosure from being reported | Homeowners who need speed, certainty, and want to avoid repairs or realtor fees. |

| Short Sale | 3-12 months | Significant negative impact, but less than foreclosure | "Underwater" homeowners who owe more than the home is worth (requires lender approval). |

| Deed in Lieu | 30-90 days | Significant negative impact, similar to a foreclosure | Homeowners with no other liens who want to avoid a public auction (requires lender approval). |

| Loan Modification | 1-3 months | Can be neutral or slightly negative if payments are late | Homeowners who have had a temporary setback but can afford new, modified payments. |

Each path has its own pros and cons, but as you can see, some options give you far more control and a much faster resolution than others. The key is choosing the one that best fits your specific situation and timeline.

Exploring Your Options to Sell Before the Auction

So, you know the pre-foreclosure clock is ticking. This is your window of opportunity, and now it's time to get a handle on the actual paths you can take to avoid that auction. Each one has its own timeline, its own headaches, and a different impact on your wallet and credit.

Selling a house in foreclosure is never a one-size-fits-all deal. A military family in Fayetteville getting unexpected PCS orders can’t afford a slow, drawn-out sale. An out-of-state owner who just inherited a house in Hope Mills needs a simple, clean solution, not a logistical mess.

Let’s get real about the most common ways to sell your home before the bank steps in.

The Traditional Real Estate Sale

Your first instinct might be to call a real estate agent. And yes, a traditional sale is definitely possible during pre-foreclosure, if you have enough equity to pay off the mortgage, all the closing costs, and the agent's commission. If you do, this route lets you pocket that leftover equity.

But here’s the catch: time is your worst enemy. The traditional market is a slow dance of staging, showings, back-and-forth negotiations, and waiting on buyer financing and inspections. This process can easily eat up months—time you probably don't have. That looming auction date often forces sellers to take the first lowball offer that comes along, wiping out the very equity you were trying to save.

Pursuing a Lender-Approved Short Sale

What happens if you owe more on your mortgage than the house is worth? When you're "underwater," a traditional sale is off the table. This is where a short sale comes into play.

A short sale is when you convince your lender to accept less than what you owe on the mortgage as payment in full. It sounds good on paper, but the reality is a nightmare of red tape.

- Lender is in Control: You can’t just decide to do a short sale. The lender has to approve everything—the list price, the agent, and especially the final offer.

- It's a Marathon, Not a Sprint: Get ready to wait. Short sales are notoriously slow, taking anywhere from 3 to 12 months because of the mountains of paperwork and bank bureaucracy.

- Serious Credit Damage: While it’s better than a full-blown foreclosure, a short sale still puts a major dent in your credit score and will haunt your credit report for seven years.

For the bank, a short sale is often cheaper than foreclosing. But for a homeowner who needs a quick, guaranteed exit, it’s a massive gamble with no certain outcome.

The Deed in Lieu of Foreclosure Option

Another possibility is a deed in lieu of foreclosure. This is where you basically hand the keys back to the bank. You voluntarily sign over the property’s deed, and in return, the lender agrees to cancel your mortgage debt.

You avoid the public spectacle of an auction, but the downsides are huge. Lenders often refuse to do a deed in lieu, especially if you have a second mortgage or other liens on the property. And the hit to your credit is brutal—credit bureaus see it as nearly as damaging as a completed foreclosure.

A deed in lieu gives you a quiet exit, but that’s about it. You lose the house and still trash your credit, making it a true last-ditch effort.

Don’t be fooled by the quiet of the pandemic-era moratoriums; foreclosures are back. Data from ATTOM showed about 188,000 foreclosure filings in the first half of the year, putting the U.S. on track to blow past the 322,000 filings from the previous year.

The Certainty of a Direct Cash Sale

For many homeowners in Fayetteville and across Cumberland County, the smartest and fastest way to sell a house in foreclosure is a direct cash sale. This option cuts right through the delays, red tape, and uncertainty of every other method. When you work with a local cash buyer like DIL Group Buyers, you get a clear, straightforward path forward.

A cash sale skips the banks, the agents, and the endless waiting. We assess your property as-is and give you a firm, no-obligation offer. If you accept, you can close in days or weeks, not months. That speed is everything when you're racing against a deadline. Our guide on how to stop foreclosure on my home dives even deeper into actionable strategies.

This is the best option for homeowners who need to:

- Move fast for a military relocation or a new job.

- Avoid the stress and expense of fixing up the property.

- Get total certainty with a guaranteed sale price and a closing date you choose.

At the end of the day, selling for cash gives you back control in a situation that feels completely out of your hands. It allows you to pay off the bank, protect what you can of your credit, and finally move on with your life.

How a Cash Sale Works Step by Step

When you're staring down a foreclosure deadline, the last thing you need is the drawn-out, unpredictable process of a traditional home sale. The typical real estate gauntlet—endless showings, nail-biting appraisals, and buyers whose financing could fall through at any moment—is a luxury you simply can't afford.

This is where a cash sale completely changes the game. It cuts right through the noise, offering a direct, predictable, and—most importantly—fast path to resolving your situation.

For homeowners in communities like Hope Mills or Spring Lake, the idea might feel unfamiliar, maybe even a little too good to be true. Let’s pull back the curtain and walk through exactly what to expect when you decide to sell your house in foreclosure for cash. The entire process is built for speed and simplicity, giving you a reliable solution when time is everything.

The Initial Conversation: No Strings Attached

It all starts with a simple phone call. This isn't a commitment; it's just a conversation. When you reach out to a local cash buyer like us at DIL Group Buyers, our first goal is to understand your unique situation.

We'll ask some basic questions to get a clear picture: Is there a looming auction date? What's the general condition of the house? What do you currently owe the lender? This initial chat is always confidential, completely judgment-free, and comes with absolutely no obligation. It’s just about gathering the facts so we can figure out the best way to help.

The Straightforward Property Walkthrough

Next, we'll arrange a quick visit to the property. I know this part can cause a lot of anxiety, especially if the house needs work. You might be worried about that leaky roof, the outdated plumbing, or some foundation cracks you've been meaning to get to.

Let me put your mind at ease. When we say we buy houses "as-is," we mean it.

You don't need to fix a thing. You don't have to clean or haul anything away. Don't spend a single dime on repairs. Our walkthrough is fast—often less than 30 minutes—and its only purpose is for us to assess the property's current state so we can put together a fair, informed offer.

A cash buyer's walkthrough is not a traditional home inspection meant to nitpick every little flaw. Think of it as a practical assessment to understand our repair costs. We factor that into the offer, so you don't have to worry about it.

This single step saves you from the weeks of prep work, stress, and out-of-pocket expenses that come with trying to list a home on the open market. We see the house for what it is, right now.

Calculating and Presenting Your Fair Cash Offer

After the walkthrough, we get down to business on your offer. One of the first questions people ask is, "How do you come up with the price?" It's not a mystery. It's a transparent calculation based on a few key factors:

- After-Repair Value (ARV): First, we figure out what your home would be worth on the market if it were fully renovated, based on recent sales of similar homes in your neighborhood.

- Cost of Repairs: We then estimate the total cost of materials and labor needed to get the property up to that market-ready condition.

- Our Operating Costs: This includes things like taxes, insurance, and utilities while we're renovating, plus the costs of selling the property once it's finished.

- Our Minimum Profit: We're a business, so we have to include a small profit margin to keep the lights on and help the next homeowner.

The offer you receive is simply the ARV minus all those costs. It’s a straightforward formula with no hidden fees or surprise deductions when it's time to close. We present this number to you clearly, and you are always free to accept it or walk away with zero pressure.

What you see is what you get. The offer is a net figure, which means you won't be paying 5-6% in realtor commissions. On a $200,000 sale, that's a direct savings of $10,000-$12,000.

Closing On Your Timeline

If you decide to accept the offer, the final step is closing the deal. This is where the speed of a cash sale truly makes a difference. Since we're not waiting on a bank, we get to skip the entire mortgage underwriting process that can easily take 30 to 60 days—or even longer.

We work with a reputable local title company to handle all the legal paperwork. You sign the documents, the title company wires the payment directly to your mortgage lender to satisfy the loan, and any remaining funds go straight into your bank account. You can learn more about how we sell a home for cash on our detailed guide.

Best of all, you're in control of the closing date. If you need to close in seven days to stop an auction, we can make it happen. If you need a few weeks to get your move organized, that's fine too. The power is back in your hands, giving you the certainty and peace of mind you need to finally move forward.

Know the Paperwork and the Clock: NC Foreclosure Documents and Deadlines

Successfully selling a house in foreclosure isn't just about finding a buyer—it's about mastering the clock. In North Carolina, the foreclosure process is a minefield of legal hurdles and non-negotiable deadlines. If you miss one, it can slam the door on your best options.

That's why you have to understand the paperwork that's coming your way and the dates that absolutely must be circled on your calendar. This isn't just generic legal advice. It's a real-world breakdown of what will land in your mailbox, giving you the power to act strategically instead of just reacting to the bank's next move.

Decoding the Foreclosure Paper Trail

The first signs of serious trouble usually arrive via certified mail. Don't mistake these for junk mail. Every document is a legal signal that the process is escalating, and it's critical to open and understand everything you get from your lender or their attorneys.

You're going to see a few key documents that mark how far along the foreclosure timeline you are. Think of them as your roadmap to what's coming next.

- Notice of Default: This is the official warning shot. After you've missed a few payments, your lender sends this to inform you that you have a specific window of time to "cure the default" (pay what you owe) before they call the entire loan due.

- 45-Day Notice of Intent to Foreclose: This one is a big deal in North Carolina. The lender can't even start foreclosure proceedings without sending you this notice at least 45 days ahead of time. It will spell out exactly what you need to pay to get your loan current.

- Notice of Hearing: This document is your summons for a hearing before the clerk of the superior court. The clerk isn't there to hear your side of the story; their job is simply to confirm the debt is real and the lender has the legal right to foreclose. This is often the last step before an auction date is locked in.

It's also worth remembering that other debts can complicate things. We put together a guide on selling a house with a lien on it that offers some practical insights on handling those issues.

The Deadlines You Absolutely Cannot Afford to Miss

The paperwork tells you what's happening, but the deadlines tell you when you need to act. For anyone trying to sell their home and sidestep an auction, two periods are absolutely critical here in North Carolina.

First is that 45-day window I just mentioned. This is your golden opportunity. The state mandates this buffer to give you a fighting chance to find a solution. It's the perfect time to reach out to a cash buyer like us, get a solid offer, and get the ball rolling on a sale before the foreclosure becomes a public legal filing.

Once the foreclosure is filed and a Notice of Hearing is issued, your situation becomes public record. This often attracts unwanted attention and cranks up the pressure. Acting within that initial 45-day period keeps the process more private and gives you maximum control.

The second critical deadline is the Sale Date itself. Everything you do—every phone call, every decision—should be focused on getting a deal done before this date arrives. A cash sale has to be completely finished, signed, and closed before the auctioneer's gavel falls.

After an auction, North Carolina law does have a 10-day upset bid period where someone else can come in and place a higher bid. While it might sound like a last-ditch chance, relying on it is a huge gamble. By that point, you've lost all control. Your ability to sell the property on your own terms is gone. The real goal is to get a deal done and closed long before the upset bid period even enters the conversation.

Protecting Your Credit and Financial Future

Facing foreclosure is about more than just the stress of losing your home—it’s about the long-term financial shadow that follows you for years. A foreclosure isn't just a bump in the road; it's a financial earthquake. It can haunt you when you try to get a car loan, rent an apartment, or even apply for a simple credit card.

The key to sidestepping that damage is taking control before the bank makes the final call. When you proactively sell your house, you’re no longer a victim of the process. You’re in the driver's seat of your own financial recovery.

Foreclosure vs. Proactive Selling: The Credit Score Impact

Let's be blunt: a foreclosure is one of the worst things that can happen to your credit report. Period. It can slash your score by 100 points or more and stays on your record for a full seven years, screaming "high-risk" to any future lender.

Now, compare that to your other options. A short sale still hurts, but the blow is often less severe than a full-blown foreclosure. But a fast cash sale? That’s your best-case scenario for protecting your credit.

By selling for cash, you can pay off the mortgage before the bank finalizes the foreclosure. This means the foreclosure itself might never even show up on your credit history. Sure, the late payments will still be there, but you dodge the single most devastating entry possible.

The goal is simple: keep the word "foreclosure" off your credit report entirely. Selling your house for cash is the fastest, most certain way to pay the lender, stop the legal clock, and save your ability to rebuild.

Talk to Your Lender—It’s Not as Scary as You Think

One of the most powerful moves you can make is also one of the most overlooked: just talk to your lender. So many homeowners avoid this call out of fear, but a proactive conversation can completely change the game.

Call them up and tell them you intend to sell the property. This shows you’re acting in good faith to handle the debt. Remember, lenders are businesses. Foreclosing is an expensive, drawn-out headache for them. They'd much rather get their money back without a legal battle.

When you make that call, be ready to:

- Be clear about your plan: "I am actively working to sell my home to pay off the loan and avoid foreclosure."

- Show them you’re serious: If you have an offer from a cash buyer like us, mentioning it adds a ton of credibility to your request.

- Ask for a little more time: Lenders will sometimes agree to pause the proceedings if they believe a legitimate sale is right around the corner.

This one phone call can buy you critical time. It proves you're committed to settling up, which is exactly what lenders want to see.

How a Fast Cash Sale Safeguards Your Future

Think of a cash sale as your financial damage control plan. It delivers the immediate funds to satisfy the lender, which is the only thing that will truly stop the foreclosure dead in its tracks.

First, it stops the bleeding. A quick sale prevents more missed mortgage payments from piling up and tanking your credit score. Each missed payment is another black mark, and a cash sale puts a firm end to it.

Second, it gives you a fresh start. Instead of walking away from the situation with nothing, a cash sale can sometimes leave you with leftover equity, especially if the sale price covers more than what you owe. That cash can be the cushion you need to secure a new place to live and begin rebuilding.

Ultimately, selling your house in foreclosure is a strategic decision. It's about looking past the crisis of today and choosing the one path that gives you speed, certainty, and the best shot at protecting your credit for tomorrow.

Got Questions About Selling a House in Foreclosure? You're Not Alone.

When you're facing foreclosure, your head is probably swimming with urgent questions. It's a confusing, stressful time, and it's easy to feel like you're the only one going through it. But trust me, you're not. We get calls every day from homeowners in the Fayetteville area with the exact same concerns.

Let's cut through the noise and get you some straight answers to the most common questions we hear.

Knowledge is power, and right now, you need all the clarity you can get to move forward.

How Late Is Too Late to Sell My House?

This is the big one, the question on everyone's mind. The short answer is simple: it's not too late until the house is officially sold at the foreclosure auction. As long as your name is on that deed, you have the right to sell your home.

But here’s the reality—the closer that auction date looms, the tighter your timeline gets. Trying to pull off a traditional sale with a realtor in the final weeks is nearly impossible. This is exactly why a fast cash sale often becomes the most realistic and powerful tool you have. The absolute key is to make a move before the auctioneer's gavel falls for the last time.

Can I Still Sell If I Owe More Than the House Is Worth?

Yes, you absolutely can. This situation is often called being "underwater," and while it's tough, you still have options. The most well-known path here is a short sale. This is where you work with your lender to get them to agree to accept a sale price that's less than what you owe on the mortgage.

The problem? Short sales are painfully slow. The bank has to approve every single step, and you just might not have that kind of time on your hands. A cash buyer can sometimes step in and negotiate directly with the lender to speed things up, but it’s a complicated dance that needs to start as early as possible.

Selling your house in foreclosure is a race against time. The moment you receive a notice of default, you should be exploring every option. Waiting for the bank to make the next move is the riskiest strategy you can take.

Do I Need to Make Repairs Before Selling?

No way. Especially not when you're working with a cash buyer like us. The whole point of an "as-is" sale is to lift that financial and physical burden right off your shoulders.

We fully expect homes in foreclosure to have some issues—a leaky roof, an old kitchen, maybe even foundation problems. That’s normal. We factor those potential repair costs directly into our cash offer, so you don't have to spend a single dime or lift a hammer. It lets you sell faster and keep your resources for your next chapter.

Will I Owe Taxes After Selling My House in Foreclosure?

This is a tricky one, and it really depends on your specific financial picture. If your lender forgives a chunk of your debt—like in a short sale or a deed in lieu—the IRS might see that forgiven amount as taxable income.

But there are exceptions, like the Mortgage Forgiveness Debt Relief Act, that can protect you. My best advice? Talk to a tax professional. Seriously. They can look at your numbers and tell you exactly what to expect so there are no nasty surprises down the road.

Ready to stop the foreclosure clock for good? The team at DIL Group Buyers gives you a guaranteed cash offer that closes when you need it to. We help you avoid the auction, save your credit, and get a fresh start. See what we can do for you at https://dilgrouphomebuyers.com.