When you’re going through a divorce, figuring out what to do with the house is often the biggest, most emotional hurdle. It's usually your largest shared asset, and the decision can feel overwhelming.

Simply put, you have three main choices: sell the house and split the money, have one spouse buy the other out, or put the sale off until a later date. Each option comes with its own set of financial and personal baggage, so it’s something you both need to think through carefully.

Your Three Paths for Handling the Marital Home

This decision will ripple through your finances, your living situation, and—if you have kids—their sense of stability. Getting a handle on these three core options is the first step to making a clear-headed choice that sets you up for your new life.

Let's break down the strategies we see couples in North Carolina use most often.

Option 1: Sell the House Immediately

For a lot of couples, selling the home and dividing the profits is the cleanest break possible. It turns your biggest asset into cash, giving both of you the funds to start over.

This route cuts all the financial cords tied to the property—no more shared mortgage payments, property taxes, insurance, or arguments over who's paying for a leaky roof. It provides a final, definitive number, allowing both of you to move on without a shared house complicating things. Honestly, it's often the most straightforward path, especially if neither of you can afford to keep the house on your own.

Option 2: One Spouse Buys Out the Other

A buyout is exactly what it sounds like: one of you stays in the house by purchasing the other's share of the equity. This is a popular choice when kids are in the picture, as it keeps them in their familiar home, school, and neighborhood.

But this path is a heavy financial lift. The spouse who wants to stay has to get a brand new mortgage in their name only, which is tough on a single income. The lender will scrutinize your debt-to-income ratio, and you'll need solid credit to even qualify. If you're going this route, you'll need to transfer ownership, and our guide on how to file a quitclaim deed can walk you through one of the key legal steps.

The spouse keeping the home doesn't just need cash for their ex-partner's equity. They have to prove they can single-handedly manage the entire mortgage, property taxes, and insurance. It's a high financial bar to clear right after a divorce.

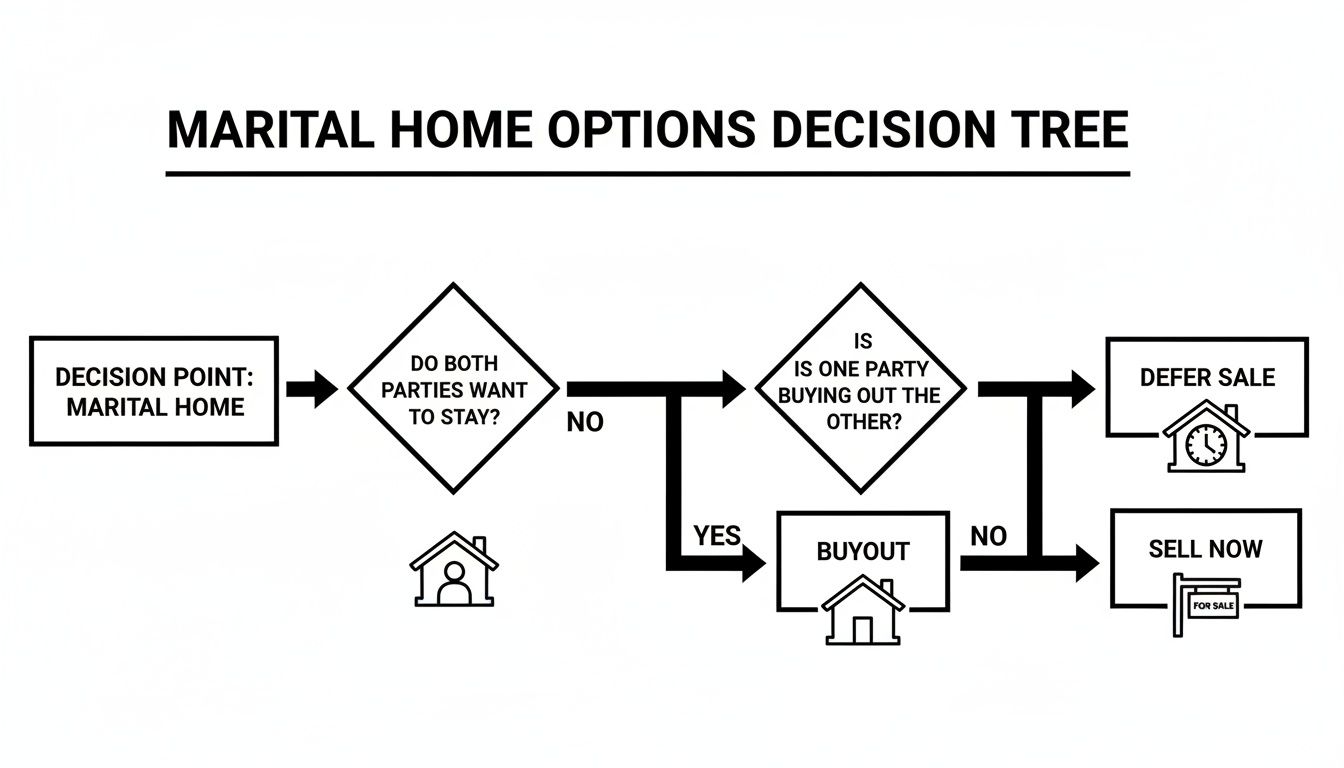

The decision tree below maps out these options and what each one really means for you.

This visual makes it clear: selling now offers a clean break, while buyouts and deferred sales bring a lot more complexity into the mix.

Comparing Your Home Sale Options During a Divorce

When you're staring down these choices, it helps to see them side-by-side. This table breaks down the three main paths to help you quickly weigh the pros and cons of each.

| Option | Best For | Key Challenge | Speed & Simplicity |

|---|---|---|---|

| Sell Immediately | Couples wanting a clean financial break and cash to start over. | Agreeing on a sale price and navigating the traditional market. | Fastest & Simplest. Liquidates the asset and ends shared liability. |

| One Spouse Buys Out | Families wanting to maintain stability for children in the same home. | The remaining spouse must qualify for a new mortgage on a single income. | Moderately Complex. Involves refinancing and legal ownership transfer. |

| Defer the Sale | Co-parenting couples who can cooperate on finances for the kids' sake. | Staying financially entangled; requires a detailed legal agreement. | Slowest & Most Complex. Delays financial separation and requires ongoing communication. |

Each path has its place, but the right one for you depends entirely on your financial situation, your ability to cooperate, and your goals for the future.

Option 3: Defer the Sale Until a Later Date

Sometimes couples choose to postpone the sale, often until a specific event happens, like the youngest child finishing high school. This is sometimes called "nesting," where the kids stay put and the parents rotate in and out of the house.

While it's done with the best of intentions for the children, this arrangement keeps you and your ex financially tied together. You’ll need a rock-solid agreement that spells out:

- Who is paying the mortgage, taxes, and insurance.

- How you'll split the costs of maintenance and surprise repairs.

- Exactly how the profits will be divided when you finally sell.

This requires a level of communication and trust that can be tough to maintain during a divorce. It basically puts your financial independence on hold. It’s a tough reality, but statistics show that 65-70% of all divorces in the U.S. involve sorting out real estate. After a divorce, the homeownership rate plummets from 78.5% for married couples to just 49.7%, because single incomes just can't keep up with today's housing costs.

For homeowners in Cumberland County feeling that pressure, a fast cash offer from a local buyer like DIL Group means you can close on your own schedule and move forward without the stress.

Untangling Your Finances: Mortgage, Liens, and Profits

When you decide to sell a house during a divorce, you're doing much more than just putting a property on the market. You're liquidating what is likely your largest shared financial asset. It’s a process that goes way beyond agreeing on a sale price—it’s about carefully untangling joint debts, clearing any claims against the home, and figuring out exactly how the final check gets split.

The first big hurdle is always the mortgage. Chances are, both of your names are on that loan, which means you're both legally on the hook for the entire debt until it’s paid off. When the house sells, paying off the outstanding mortgage balance is the very first thing that happens with the proceeds.

It's absolutely critical that this debt gets settled completely. You don't want a situation where one spouse's name stays on the mortgage after the divorce (this sometimes comes up in buyout talks). That's a recipe for financial disaster. Plus, most lenders have a "due on sale" clause, which means the loan must be paid in full when the property changes hands anyway.

Clearing the Title: Dealing with Property Liens

Before any buyer can take legal ownership, the property's title has to be crystal clear and free of any liens. A lien is simply a legal claim against your property for a debt that hasn't been paid. These things can pop up when you least expect them and bring a sale to a screeching halt if they aren't handled.

Here are a few common liens that can complicate a divorce sale:

- Mechanic's Liens: Filed by a contractor who did work on the house but never got paid.

- Tax Liens: Placed by the government for unpaid property or income taxes.

- Judgment Liens: These come from a lawsuit where a creditor won a judgment against you or your spouse.

Finding these early is key. A title company will do a search to uncover any liens. If one is found, that debt has to be paid out of the sale proceeds before you and your ex-spouse see a dime of the profits. We go into more detail in our guide on what to do when you need to sell a house with a lien on it.

Calculating and Splitting the Profits

Once the mortgage and any liens are paid off, what's left over is your net profit. This is the money you and your ex-spouse will actually divide. But hold on—before you split it 50/50, a few other costs get taken out first.

These usually include:

- Realtor Commissions: Typically 5-6% of the sale price.

- Closing Costs: This bucket includes title insurance, transfer taxes, and attorney fees, often adding up to 1-3% of the sale price.

- Agreed-Upon Repairs or Credits: Any money you promised the buyer for repairs or other concessions.

It's vital to have a written agreement that spells out exactly how these costs and the final proceeds will be divided. Don't ever rely on a verbal promise. This document protects both of you and prevents ugly arguments at the closing table.

A Real-World Sale Example

Let's walk through how this might look for a hypothetical sale right here in Fayetteville. Imagine your marital home sells for $300,000.

Here’s a quick breakdown of where the money goes:

| Item | Amount | Notes |

|---|---|---|

| Sale Price | $300,000 | The final price you agreed on. |

| Remaining Mortgage | -$180,000 | The amount you still owe the bank. |

| Realtor Commissions (6%) | -$18,000 | Paid to the real estate agents. |

| Seller's Closing Costs (2%) | -$6,000 | Covers taxes, title fees, etc. |

| Net Proceeds | $96,000 | The total profit before you split it. |

| Each Spouse's Share (50%) | $48,000 | The cash each of you walks away with. |

As you can see, the final payout shrinks fast. And this is before even thinking about capital gains tax. If you sell while you're still legally married, you can exclude up to $500,000 of profit from taxes. Once the divorce is final, that individual exemption drops to $250,000. Timing really is everything.

The financial pressure of this process is enormous. It’s no wonder the divorce appraisal service market is projected to hit $2.8 billion by 2032. This reflects just how critical it is to divide assets fairly, especially as post-divorce homeownership drops to 49.7% and single earners face an uphill battle with housing affordability. For folks in NC communities like Raeford or Dunn, a cash buyer can be a lifeline, letting you sidestep the unpredictable open market and close on your own terms.

Navigating the Legal Process and Communication

When you're trying to sell a house during a divorce, the emotional and financial undertow can feel overwhelming. This is where solid legal documents and crystal-clear communication become your lifeline, guiding you through the turbulence to a fair outcome. Without them, you're just asking to get pulled into a whirlpool of misunderstandings and costly court battles.

Think of your divorce decree or separation agreement as the blueprint for the entire sale. This legally binding document is your single source of truth, and it needs to be hammered out before a "For Sale" sign ever hits your lawn. Trust me, trying to sell a house based on a verbal agreement is a recipe for disaster.

Laying the Groundwork with a Solid Legal Agreement

Your agreement has to be painstakingly detailed, leaving zero room for interpretation. The whole point is to anticipate every potential argument and get it down in writing while you're both still in a negotiating mindset—not in the heat of a last-minute crisis.

This essential document should explicitly cover:

- The Listing Price: How will you two agree on the starting price? What's the plan for price reductions if the house sits on the market?

- Agent Selection: Who picks the real estate agent? What happens if you can't agree on one?

- Offer Acceptance: What's the absolute minimum offer you're both willing to take? How will you handle negotiations and counteroffers?

- Covering Costs: Who pays the mortgage, utilities, and insurance while the house is for sale?

- Repair Expenses: How will you fund necessary repairs that come up during an inspection? Will you set a spending limit before needing mutual approval for bigger ticket items?

Having this agreement isn't just a good idea—it's your primary defense against future conflict. It turns the emotionally charged process of selling a shared home into a structured business transaction, which is exactly what you need right now.

You'll also probably hear the term quitclaim deed. This is a legal tool used to transfer one spouse's interest in the property to the other, which is common in a buyout situation. Understanding what it does is crucial for ensuring the property's title is clean before you try to sell.

The Power of Clear and Consistent Communication

Even with the best legal agreement in the world, the day-to-day details of selling a home demand cooperation. Tensions are almost always high during a divorce, which can make a simple conversation feel like walking through a minefield. The key is to set up a communication plan that is professional, respectful, and laser-focused on the task at hand.

Setting clear boundaries is everything. Agree on a specific way you'll communicate and how often. Maybe you decide to only discuss the house sale through a dedicated email thread or a co-parenting app. This creates a written record and stops conversations from spiraling into old arguments.

Try these strategies to keep things moving forward:

- Keep it Business-Like: Treat your ex like a business partner. Keep your conversations brief, factual, and strictly about the sale.

- Use a Mediator: If talking directly is impossible, let your attorneys or a neutral third party relay information and help with decisions.

- Centralize Information: Create a shared Google Drive or Dropbox folder with all the important documents, like offers, inspection reports, and repair quotes.

For instance, when an offer comes in, the process shouldn't involve a tense phone call. It should be simple: your agent emails the offer to both of you. You each review it and reply with your decision—accept, reject, or counter—all based on the terms you already agreed to in your separation agreement.

This structured approach takes the emotion out of the equation. It protects your financial interests and, just as importantly, your own peace of mind. By focusing on a clear legal framework and disciplined communication, you can get through the sale efficiently and start your next chapter with fewer scars.

When you're trying to sell a house during a divorce, the road you take can make all the difference in speed, stress, and what you ultimately walk away with. You really have two main options: listing with a traditional real estate agent or selling directly to a cash home buyer. Each has its place, and the right choice depends entirely on your situation.

The traditional route is what everyone knows. You hire a realtor, scramble to get the house "market-ready," and then deal with a parade of showings, open houses, and negotiations. A cash offer, on the other hand, is a completely different animal—a direct, private sale that skips the open market altogether.

The Traditional Realtor Experience

Hiring a realtor is the default for most people, and it makes sense if you're in a hot market and hoping to get top dollar. A great agent will handle the marketing, schedule all the showings, and go to bat for you during negotiations. The goal is to get multiple buyers interested, maybe even start a bidding war to push up the price.

But—and this is a big but during a divorce—this path demands a serious investment of time, money, and cooperation.

To get a home ready for the market, you're usually looking at a long to-do list:

- Fixing things up: You’ll need to tackle any problems a home inspector might find, from a leaky pipe under the sink to a roof that's seen better days.

- Decluttering and staging: This means packing up personal belongings and arranging furniture to make every room look spacious and inviting.

- Boosting curb appeal: Investing in landscaping, power washing, or a fresh coat of paint is often necessary to make a great first impression.

These jobs are tough for any couple. When you're separating, trying to agree on which repairs to fund and how to split those costs can start a whole new fight. Then there's the constant need to coordinate schedules for showings and keep the house spotless for strangers walking through at all hours.

A traditional sale is a marathon, not a sprint. The average time to close with a buyer who needs a mortgage is 30 to 45 days after you've already accepted their offer. And finding that buyer? That can take weeks, if not months, dragging out the process and your financial entanglement.

The Fast Cash Offer Alternative

A fast cash offer completely flips the script. Instead of you preparing the house for buyers, the buyer comes prepared to take the house exactly as it is. This is an absolute game-changer when you're already dealing with the emotional and financial weight of a divorce.

Companies like DIL Group Home Buyers specialize in buying homes directly from the owners. The entire transaction is straightforward, with no commissions. The biggest wins here are speed, certainty, and simplicity.

Think about a military couple stationed at Fort Bragg. They get unexpected PCS orders right as their separation is being finalized. They don't have months to list their home, wait for offers, and cross their fingers that the buyer's loan gets approved. They need a guaranteed sale on a clear timeline. A cash buyer can put an offer in their hands within days and close the deal in as little as a week or two. You can learn more about how to sell your home for cash and see what the process looks like.

This route also cuts out the biggest sources of conflict in a divorce sale:

- No Repairs Needed: You sell the house "as-is." That means zero arguments over who pays for a new HVAC system or how to fund a kitchen remodel.

- No Showings: The sale is private. You can skip the stress and invasion of privacy that comes with endless tours.

- No Financing Drama: The number one reason traditional sales fall apart is the buyer's financing getting denied. A cash offer is a sure thing.

Making The Right Choice For Your Situation

So, which path is better? There's no single right answer. It all comes down to your priorities and how well you and your ex-spouse are able to work together. Seeing the two options side-by-side can help make the decision a lot clearer.

Realtor Sale vs Cash Buyer During Divorce

Here’s a quick breakdown to help you compare the key differences between selling with a traditional agent and working with a direct cash home buyer.

| Factor | Traditional Realtor Sale | Cash Buyer (e.g., DIL Group) |

|---|---|---|

| Sale Price | Potentially higher, but reduced by commissions, repairs, and closing costs. | A fair cash offer with zero commissions or repair costs. |

| Timeline | Weeks or months to find a buyer, plus a 30-45 day closing. | Offer in days, close in as little as 1-2 weeks. |

| Certainty | Sale can fall through due to financing issues or inspection problems. | Guaranteed sale. The offer is firm and the closing date is fixed. |

| Convenience | Requires repairs, staging, constant cleaning, and disruptive showings. | Sell "as-is" with no repairs and no public showings. |

| Best For | Couples who can cooperate, have time and money for repairs, and want to maximize the potential sale price. | Couples needing a fast, certain, and conflict-free sale to move on. |

If you and your ex are on good terms and have the emotional energy and financial cushion to navigate a traditional sale, you might end up with a higher price on paper. But for many people, especially in contentious divorces or when time is a major factor, the net benefit of a fast, guaranteed cash sale is priceless. It provides peace of mind, allowing both of you to get your money quickly and finally make a clean break.

A Local Solution for Fayetteville Homeowners

If you're trying to sell a house during a divorce in Fayetteville, Hope Mills, or around the Fort Bragg area, you know the local market has its own unique pressures. The constant cycle of military PCS moves often forces a sale on an already tight and emotional timeline. When you add that to the stress of a divorce, trying to sell your home the traditional way can feel downright impossible.

This is where a dedicated, local solution really makes a difference. You don't have to deal with the uncertainty of showings, haggling over repairs, or waiting on a buyer's financing to get approved. There's a much simpler way. For folks in Cumberland County, DIL Group Home Buyers offers a direct path forward because we get the specific challenges local families are up against.

How a Local Cash Buyer Solves Divorce-Related Problems

Working with a local cash buyer like us cuts right through the biggest headaches of a divorce sale. The entire point is to get rid of conflict and complications so both of you can move on, financially and emotionally.

The process is built on certainty and control—two things that are often in short supply during a separation.

- Guaranteed Closing Date: You get a firm closing date you can count on. This is huge for military families who have to relocate or for anyone who needs to finalize their divorce settlement.

- No Repairs Needed: We buy your house "as-is." This immediately stops any arguments over who’s going to pay for a new roof or fix that leaky faucet—common sticking points that can derail the whole process.

- Complete Privacy: You get to skip the invasive parade of strangers walking through your home for showings and open houses. Your sale is a private matter between you and us.

- No Commissions or Fees: The cash offer we give you is what you get. No realtor commissions or hidden fees will pop up at the last minute and eat into your proceeds.

Selling to a trusted local buyer can turn a messy, months-long ordeal into a simple, predictable transaction. You get to sidestep the market's unpredictability and start focusing on your future.

The DIL Group Home Buyers Approach

Our whole approach is designed to be fast and totally transparent because we know you need a clear solution, not more stress. We've simplified it down to three easy steps that put you in control.

First, just reach out with your property details. Give us a quick call or fill out the online form—whatever works for you. There's zero obligation. It’s just a conversation to learn about your situation.

Next, our team will quickly evaluate your home and present a fair, all-cash offer. This offer is guaranteed and won't suddenly change before closing. It’s based on the home’s current condition, so you won’t have to spend a single penny on improvements.

Finally, if you like the offer, you pick the closing date. Need to close in ten days to meet a PCS deadline? No problem. Need a month to line up with your divorce finalization? We work on your schedule. The entire process is handled professionally to make sure closing is smooth and completely stress-free.

For homeowners in Fayetteville and Cumberland County, that local expertise is everything. DIL Group Home Buyers provides a reliable exit strategy, helping you close this chapter and start the next one with confidence.

Your Top Questions About Selling a House During a Divorce

Selling a home during a divorce is already tough. Add in all the questions and "what-ifs," and it can feel completely overwhelming. You're not just dealing with a property transaction; you're untangling a shared life, and every decision feels heavy.

Getting straight answers is the first step to taking back control. Let's break down the questions we hear most often from homeowners right here in North Carolina.

What if My Spouse Won't Agree to Sell the House?

This is probably the most common and maddening problem we see. If your spouse is refusing to cooperate, you can't force them to sign a listing agreement or a sales contract. Plain and simple, the property can only be sold if both owners agree or if a judge orders it.

If you can't work it out through mediation or with your attorneys, the court will have to step in. The final divorce decree will usually force the sale and lay out exactly how it has to happen.

What happens if one person still refuses to cooperate, even with a court order? A judge can appoint someone else—like a real estate commissioner—to take over, manage the sale, and sign the documents for the uncooperative spouse.

This is the last resort. It's an expensive, slow process that takes all control out of your hands. It's always, always better to find some common ground before things get to this point.

Who Pays the Mortgage and Repairs While We're Trying to Sell?

This is a huge detail that absolutely must be spelled out in your separation agreement. Relying on a verbal "we'll figure it out" is a recipe for disaster.

Here are a few ways couples usually handle these costs:

- Split Everything 50/50: Many couples agree to split the mortgage, insurance, taxes, and any necessary repair costs right down the middle. They often get reimbursed for their share from the proceeds at closing.

- The Person Living There Pays: Sometimes, the spouse who stays in the home during the sale process agrees to cover all the ongoing expenses. In exchange, they might negotiate to receive a bigger piece of the final profit to make up for it.

Of course, there's a much simpler way to handle this. When you sell your house "as-is" to a cash buyer, you take repairs completely off the table. This gets rid of a massive source of conflict and makes the whole process smoother.

Can We Sell Our House if There's a Lien on It?

Yes, you absolutely can. Selling a home with a lien is more common than you'd think. A lien is just a legal claim against the property for an unpaid debt, and it has to be paid off before the house can be sold to a new owner.

Experienced cash home buyers deal with this all the time. We frequently buy properties with liens from unpaid property taxes, contractors (called a mechanic's lien), or court judgments. The process is straightforward: the title company pays the debt directly out of your sale proceeds at closing. A good buyer will handle all the coordination to make sure the debts are cleared, giving you and your ex a clean slate.

How Do We Deal With Capital Gains Tax?

This is a big one. Understanding capital gains tax is key to keeping more of your money. Right now, the IRS allows a married couple filing a joint tax return to exclude up to $500,000 in profit from the sale of their main home.

To get this break, you must have owned the home and lived in it for at least two out of the five years before you sell. But here’s the catch: once your divorce is final, that tax advantage gets cut in half. As single individuals, you can each only exclude up to $250,000.

When you finalize your divorce can have a huge impact on your bottom line. We always recommend talking to a tax professional who can look at your specific numbers and help you make the smartest decision.

Trying to figure all this out is stressful, but you don't have to go it alone. If you're in the Fayetteville area and need a fast, guaranteed, and conflict-free way to sell, DIL Group Home Buyers can give you a fair cash offer and close whenever you're ready. See how simple our process is at https://dilgrouphomebuyers.com.