When you inherit a house, your mind immediately jumps to a hundred different questions, and most of them probably have a dollar sign attached. But I've got some good news: the initial tax hit is usually far less scary than people think. In most cases, you won't owe a dime just for receiving the property. The real tax conversation starts when you decide what to do with it, especially if you plan to sell.

Your First Guide to Inherited House Taxes

Trying to get your arms around the financial side of an inheritance is tough enough, especially when you're already dealing with a loss. Then you start hearing words like "estate tax," "inheritance tax," and "capital gains," and it's easy to feel completely overwhelmed.

Let’s cut through the noise. This guide is your starting point—a way to understand the core concepts without getting lost in the jargon. We'll break down the tax implications you need to know right now, so you can build a solid foundation before you make any big moves with the property.

Federal Estate vs. State Inheritance Tax

First things first, let's clear up two terms that often get tangled together: estate tax and inheritance tax. They sound similar, but they work very differently.

The federal estate tax is a tax on the entire value of a deceased person's estate before anything is handed out to the heirs. Honestly? This is a "millionaire's tax" and doesn't apply to most people.

An inheritance tax, on the other hand, is paid by the person receiving the inheritance. Here’s the key takeaway: there is no federal inheritance tax in the U.S., and even better, North Carolina doesn't have one either.

The federal government only taxes an estate if its value is incredibly high—we're talking an exemption of nearly $15 million per person for 2026. And since North Carolina is one of the many states with no state-level estate or inheritance tax, most heirs here are in the clear. Only a handful of states still have an inheritance tax. You can always get the latest on federal tax laws from leading estate planning experts.

For the vast majority of people inheriting a home in North Carolina, neither of these big taxes will ever be a factor. That simplifies things a lot right out of the gate.

To help you keep these straight, here is a quick cheat sheet on the main tax concepts you might hear about.

Key Tax Concepts for Inherited Property at a Glance

This table breaks down the different taxes you might encounter. It's a quick way to see what's what and, more importantly, what actually applies here in North Carolina.

| Tax Type | Who Pays It? | Does It Apply in North Carolina? |

|---|---|---|

| Federal Estate Tax | The deceased's estate (before distribution) | Only for estates over the $15 million exemption. |

| NC Estate Tax | The deceased's estate | No. North Carolina does not have an estate tax. |

| NC Inheritance Tax | The heir (after receiving the property) | No. North Carolina does not have an inheritance tax. |

| Capital Gains Tax | The heir (only when the property is sold) | Yes, but only on the profit made after inheritance. |

As you can see, the main one to focus on is capital gains tax, and that only comes into play if you sell the property.

The Most Important Tax Advantage You Have

If you remember just one thing from this guide, make it this: the "step-up in basis." This is your single most powerful financial tool as an heir.

Think of it as a giant reset button for the property's value. For tax purposes, the home's cost basis is "stepped up" to its fair market value on the date the original owner passed away.

This means all the appreciation—every dollar the house gained in value while your loved one owned it—is completely wiped clean from a tax standpoint. We’ll dig into exactly how this magic works in the next section, but just know that this concept is your best friend for minimizing or even eliminating taxes if you choose to sell.

How the "Step-Up in Basis" Can Wipe Out Decades of Taxes

If there's one single concept you need to grasp about inheriting a house, it's the step-up in basis. This isn't just some minor tax loophole; it's the single most powerful financial advantage you have as an heir, and it can literally save you tens or even hundreds of thousands of dollars.

Think of it as hitting a giant reset button on the property's value for tax purposes. When you inherit a home, the IRS doesn't care what the original owner paid for it. Instead, its value is "stepped up" to whatever it was worth—its fair market value—on the day the person passed away.

This one move effectively erases all the appreciation the property gained over the years. The slate is wiped clean for you.

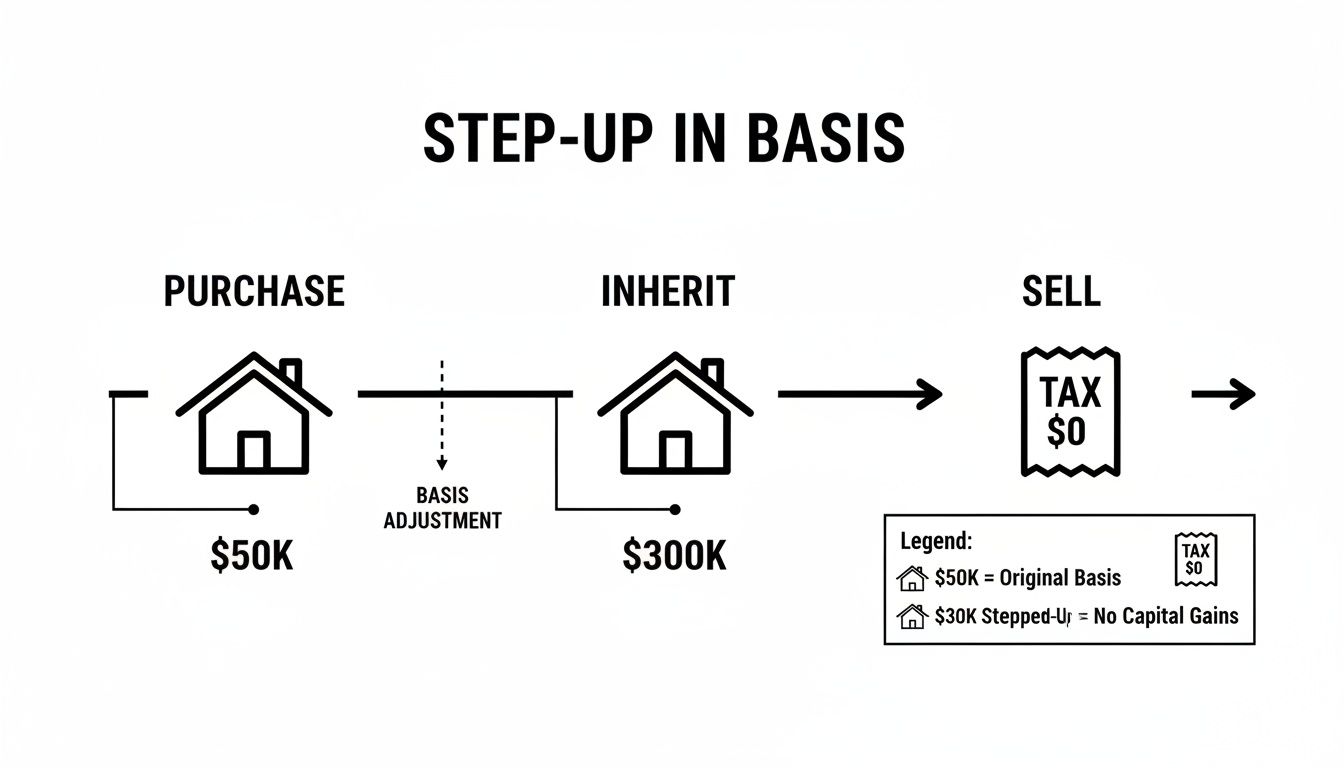

A Real-World Step-Up Example

Let's put this into real numbers. Say your mother bought her house in Fayetteville back in 1985 for $50,000. She lived there for nearly four decades, and the property's value shot up. When you inherit it this year, a professional appraisal confirms its fair market value is now $300,000.

Thanks to the step-up in basis, your new cost basis for that house is $300,000, not the original $50,000 she paid. That massive $250,000 increase in value that happened during her lifetime? It's now completely shielded from federal capital gains tax.

The step-up in basis is a fundamental part of U.S. tax law for inherited property. It's designed to ensure that you, the heir, aren't hit with a massive tax bill for gains you never personally benefited from. It gives you a fresh start.

So, what happens when you go to sell? If you turn around and sell the house immediately for its appraised value of $300,000, your taxable gain is zero. You sold it for $300,000, and your new basis is $300,000. That means $0 in profit, and you owe nothing in federal capital gains tax.

How Capital Gains Tax Works After You Inherit

Now, this doesn't mean you get a permanent "get out of tax free" card. The step-up rule just means you're only on the hook for any appreciation that happens after you inherit the property. The clock on your ownership starts ticking from that day forward.

Let's stick with the example. If your grandmother bought her Spring Lake home for $50,000 back in 1980 and it's worth $300,000 when she passes, your basis steps up to that $300,000. But let's say you decide to hold onto it for a year. The market gets hot, and you end up selling it for $360,000.

You will owe capital gains tax, but only on the $60,000 profit you made while you owned it. You can understand the latest on inheritance tax regulations to see how this fits into the bigger picture of wealth transfers.

This powerful provision gives you three clear advantages:

- Wipes Out Past Appreciation: You aren't taxed for decades of market growth that happened before you ever owned the home.

- Reduces or Eliminates Your Tax Bill: If you sell the property quickly, you’ll likely owe very little, or even nothing at all, in capital gains tax.

- Gives You Financial Clarity: It establishes a clean, simple starting point for calculating any future gains, making your financial planning much easier.

Understanding Estate Tax vs. Inheritance Tax

Let's cut through the confusion right away. When you inherit property, you'll hear two terms thrown around that sound almost the same: estate tax and inheritance tax. Knowing the difference is your first step to getting a clear picture of the financial road ahead.

Here’s the simplest way to think about it:

- An estate tax is a tax paid by the deceased person's estate before you, the heir, see a dime.

- An inheritance tax is a tax paid by you after you've received the property.

The good news? For most people, neither of these is going to be a problem.

The Federal Estate Tax Hurdle

The federal estate tax is really only a concern for the ultra-wealthy. The government sets a very high bar—an exemption amount so large that over 99% of estates in the United States never pay a penny.

This tax is tallied up based on the estate's total value—cash, property, investments, the whole lot. It’s the estate's job to settle that bill before anything gets passed down to the heirs.

But frankly, what often matters more is a huge tax advantage you do get, called the "step-up in basis."

This rule is a game-changer. It means the property's value for tax purposes resets to whatever it was worth on the day you inherited it. Thanks to this, you can often sell an inherited home right away and owe little to nothing in capital gains tax.

State-Level Taxes: The North Carolina Advantage

While the feds have their rules, each state gets to make its own. This is where things can get tricky, as the laws are all over the map.

But if you're inheriting property in North Carolina, you can breathe a sigh of relief. The state keeps it simple.

North Carolina has no estate tax and no inheritance tax. When you inherit a house here, the state government doesn't take a slice from the estate or from your inheritance.

This is a massive advantage. However, if you live in another state, you need to check your own state's rules, as a handful of them do collect one or both of these taxes.

For out-of-state owners, knowing your local tax situation is critical. The landscape can vary significantly from North Carolina's straightforward approach.

Here’s a quick look at how different states handle these taxes:

State Estate and Inheritance Tax Overview

| State | Has Estate Tax? | Has Inheritance Tax? |

|---|---|---|

| Connecticut | Yes | No |

| Hawaii | Yes | No |

| Illinois | Yes | No |

| Iowa | No | Yes |

| Kentucky | No | Yes |

| Maine | Yes | No |

| Maryland | Yes | Yes |

| Massachusetts | Yes | No |

| Minnesota | Yes | No |

| Nebraska | No | Yes |

| New Jersey | No | Yes |

| New York | Yes | No |

| Oregon | Yes | No |

| Pennsylvania | No | Yes |

| Rhode Island | Yes | No |

| Vermont | Yes | No |

| Washington | Yes | No |

| Washington D.C. | Yes | No |

As you can see, only a minority of states impose these taxes, but if you happen to live in one of them, it’s something you need to plan for.

If you'd like to dive deeper, you can learn more about how North Carolina's lack of inheritance tax benefits heirs in our detailed article. This clear advantage makes managing an inherited property in NC much more straightforward.

Deciding Your Next Move: Keep, Rent, or Sell

Once you've wrapped your head around the tax side of things, the big question hits: what are you actually going to do with the house? This isn't just a numbers game; it's tangled up in memories, emotions, and what you want for your own future.

There’s no single right answer, and each path—keeping, renting, or selling—comes with its own financial reality and lifestyle changes. Let's walk through the three main options so you can figure out what makes the most sense for you.

Option 1: Keeping the Property

Holding onto the house is often the first instinct, especially if it was a home filled with family memories. It can feel like you're preserving a part of your loved one's legacy. But before you get too far down that road, you have to be brutally honest about the costs.

You're not just inheriting a house; you're inheriting all of its bills. These aren't one-and-done expenses, either. They're a constant part of homeownership.

- Property Taxes: These come around every year, and depending on the home’s value, they can be a significant hit to your budget.

- Homeowner's Insurance: This is non-negotiable. You have to protect the property, and that adds another recurring expense.

- Maintenance and Repairs: Houses always need something. One day it's a leaky faucet, the next it could be a new roof that costs thousands. These surprises are guaranteed to happen.

- Utilities: Even if nobody is living there, you’ll still be paying for electricity, water, and maybe gas just to keep the place in working order.

Keeping an inherited house means you are adopting a second set of bills. Before committing, create a detailed budget of all potential holding costs to ensure it’s financially sustainable for you.

Option 2: Renting It Out

Renting out the property can look like the perfect compromise. You keep a valuable asset in the family and it generates a steady paycheck every month. If the house is in a great area, this can be a fantastic long-term investment.

But don't fool yourself—being a landlord is a job, not a hobby. It takes real time, a lot of patience, and a thick skin. And if you live out of state? The headaches multiply fast.

You’re the one responsible for finding good tenants, chasing down late rent, and answering that 2 AM call about a broken water heater. You can hire a property manager to handle the day-to-day, but they’ll take a cut, usually 8-12% of the monthly rent, which eats directly into your profit. On top of that, you have to learn the local landlord-tenant laws, which can be a minefield.

Option 3: Selling the House

For a lot of people, selling is simply the cleanest, most practical way forward. It turns a complicated asset into cash—money you can use to pay off your own mortgage, invest for retirement, or just put in the bank for a rainy day.

Selling right away also cuts you loose from all the ongoing costs and worries of being a property owner. No more property tax bills, no more insurance premiums, and no more sleepless nights wondering when the furnace will finally give out.

Plus, thanks to that "step-up in basis" we talked about, the tax hit from selling is often surprisingly small, especially if you sell soon after inheriting. Our guide on how to sell inherited property breaks down the exact steps to make this process smooth.

Ultimately, selling brings closure. It frees you from the responsibility of a property you might not have the time, money, or desire to manage.

How to Manage an Inherited House from Out of State

Inheriting a house is a big deal. But when that house is hundreds of miles away, the stress multiplies overnight. Suddenly, you're not just an heir—you’re a long-distance landlord with a second set of responsibilities you never asked for.

This distance turns simple problems into logistical nightmares. A task that a local owner could handle in an afternoon becomes a week-long headache for you. The challenges pile up fast, turning what should be a blessing into a source of non-stop anxiety and bills.

The Headaches of Remote Ownership

Being an out-of-state heir means you're hit with problems local owners never even think about. And every single one of them costs you money, time, and peace of mind.

Here are just a few of the remote management challenges you'll face:

- Coordinating Repairs: Trying to find a trustworthy plumber or electrician from another state is a total gamble. You're stuck relying on online reviews, hoping you don't get ripped off.

- Property Security: An empty house is a target. Vandalism, break-ins, squatters—you name it. You can't just swing by to check on the place, leaving it vulnerable and adding to your stress.

- Constant Travel: Every time there's an emergency, like a burst pipe or a meeting with a contractor, it could mean an expensive, last-minute flight and time off work.

- Navigating Local Laws: You have to deal with local probate courts, like those in Cumberland County, which have their own specific rules. Handling that from a distance is a major obstacle.

These aren't just little annoyances. They are real, ongoing problems. The cost of flights, emergency fixes, and constant maintenance can drain the value of your inheritance before you know it.

The Practical Solution for Out of State Heirs

All the constant worry and surprise expenses lead most out-of-state owners to one simple conclusion: they need a clean, fast exit. The burden of managing a property from afar is just too much. This is where selling directly to a trusted, local cash buyer becomes the smartest path forward.

Selling for cash wipes out every single one of those pain points.

- No Repairs Needed: You sell the house "as is." That means no managing contractors from 500 miles away.

- No Showings or Listings: The sale is direct and private. No need to deal with realtors, showings, or strangers walking through the home.

- A Guaranteed Timeline: You get a firm closing date you can count on. No more uncertainty—you can plan your finances and move on.

For an heir living out of state, a cash sale isn't just about the money. It's about getting your time back and finally having some peace of mind. You can learn more about how probate property sales offer a straightforward solution to this complicated and stressful situation.

Why a Cash Sale Is the Simplest Way to Move Forward

You've waded through the complexities of estate taxes and the step-up in basis. That knowledge is your biggest asset, but it’s only half the battle. Now, it's time to turn that understanding into a clear-cut decision that brings you peace of mind.

For many heirs, especially those trying to manage a property from another state, a direct cash sale cuts through all the noise. It’s the most straightforward path forward, offering a clean break from a responsibility you never asked for.

Get Rid of All the Financial Guesswork

Putting a house on the traditional market can feel like a marathon of endless expenses and waiting games. A cash sale turns it into a sprint with a guaranteed finish line. It systematically strips away all the financial burdens that make inheriting a house so stressful.

Think about everything a cash sale lets you skip:

- No Realtor Commissions: Those 5-6% commission fees can take a massive bite out of your inheritance. With a direct sale, that money stays right where it belongs—in your pocket.

- No Expensive Repairs: You sell the house completely "as-is." Forget about spending thousands on updates or losing sleep over what an inspector might find.

- No More Holding Costs: Every single month you own that house, you’re bleeding money on property taxes, insurance, and utilities. A quick cash sale stops that drain immediately.

A direct cash sale gives you one thing you can't get on the open market: certainty. You get a firm offer and a set closing date, letting you sidestep all the market’s unpredictability and just move on.

This isn't just about getting a check faster. It's about getting immediate financial relief and finality. You can access the real value of your inheritance without the months of stress, surprise costs, and emotional drain of managing an unwanted property. It truly is the simplest solution to a very complex problem.

Here is the rewritten section, crafted to sound completely human-written and natural, following the provided style and guidelines.

Your Inherited House Tax Questions, Answered

When you inherit a house, a million questions probably pop into your head. It's a lot to handle. Let's cut through the noise and get you some straight, simple answers to the most common questions we hear from heirs.

How Long Do I Have to Sell to Get the Step-Up in Basis?

This is a big one, but the answer is simple: there’s no deadline.

You get the step-up in basis automatically, locked in on the date of the original owner's death. You don't have to rush to sell just to qualify for it.

But here’s something to keep in mind: the longer you hold onto the property, the more it could go up in value. Any appreciation that happens after you inherit it is on you, and you'll owe capital gains tax on that new profit when you sell.

What if the Inherited House Has a Mortgage or Liens?

When you inherit a house, you usually inherit its financial baggage, too. That means you're now on the hook for the mortgage payments.

If the property has tax liens or other judgments against it, those have to be settled before you can get a clear title to sell. This is where a cash buyer can be a lifesaver. We can often buy the property as-is and pay off those debts directly at closing, taking a huge headache off your plate.

As the new owner, you are responsible for paying all property taxes from the date you inherit the home until the day you sell it. These holding costs are a key reason many heirs choose to sell quickly.