That sinking feeling when you discover a lien on your property is awful, but don't panic. The very first move isn't to worry—it's to get the facts. You need to verify the lien’s legitimacy by digging into public records to find out who the creditor is, the exact amount they claim you owe, and when they filed it. Getting these details straight is the essential first step in creating a plan to get it removed.

What to Do When a Lien Appears on Your Property

So, what is a property lien? Think of it as a legal "sticky note" a creditor puts on your property for an unpaid debt. This "cloud" on your title makes it nearly impossible to sell, refinance, or even give the property away until that debt is cleared. The good news is, you have options. The whole process starts with understanding exactly what you're dealing with.

Before you can figure out how to remove a lien, you need to confirm it even exists and that all the details are accurate. Time for a little detective work.

Verify the Lien Details

Your starting point is the Cumberland County Register of Deeds. You can visit their office in person or check their online portal. Public records are your best friend here. You're hunting for a few key pieces of information that will shape your entire strategy:

- The Lienholder: Who is the person or entity that filed this claim? Is it a contractor, a government agency like the IRS, or another creditor who got a court judgment against you?

- The Amount Owed: What's the exact dollar amount listed on the lien? Just as important, does that number actually match what you owe?

- The Filing Date: When was this lien officially put on record? This is a critical date, as it can impact the lien's validity, especially under North Carolina's statute of limitations.

A lien on your property will stop any sale or refinance dead in its tracks until it's satisfied. The smartest move is to proactively order a title report and resolve any known liens before you even think about selling. It'll save you a world of headaches and costly delays.

Quick Guide to Common Property Liens in North Carolina

Not all liens are created equal, and knowing what you’re up against is half the battle. The type of lien determines the rules of the game and your options for removing it. Here’s a quick rundown of what we often see with homeowners in Fayetteville and Cumberland County.

| Type of Lien | Who Files It? | Common Reason for Filing | Where to Verify in Cumberland County |

|---|---|---|---|

| Mechanic's Lien | Contractors, Subcontractors, Suppliers | Unpaid bills for labor or materials on a home improvement project. | Cumberland County Register of Deeds |

| Tax Lien | IRS, NC Dept. of Revenue, Cumberland County | Unpaid federal, state, or local property taxes. | Register of Deeds and County Tax Office |

| Judgment Lien | A Creditor Who Won a Lawsuit | A court ruling in favor of a creditor for an unpaid debt (e.g., credit card). | Cumberland County Clerk of Superior Court |

| Mortgage Lien | Your Lender (Bank, Mortgage Co.) | Standard practice; filed when you take out a mortgage to buy the property. | Cumberland County Register of Deeds |

Understanding these distinctions is crucial. For example, a local contractor who did a kitchen remodel in Hope Mills but didn't get their final payment can file a mechanic’s lien. These are common in construction disputes, but they have very strict filing deadlines here in North Carolina.

If you fall behind on taxes, a tax lien might pop up from the county or even the IRS. These are serious and can be tough to fight. Another frequent one is a judgment lien, which happens after a lawsuit. If a creditor takes you to court over a debt and wins, they can slap a lien on your property to secure what they're owed.

Once you’ve gathered all this information, you’ll have the clarity you need to tackle the problem head-on, whether that means paying the debt, negotiating a lower amount, or fighting an invalid claim.

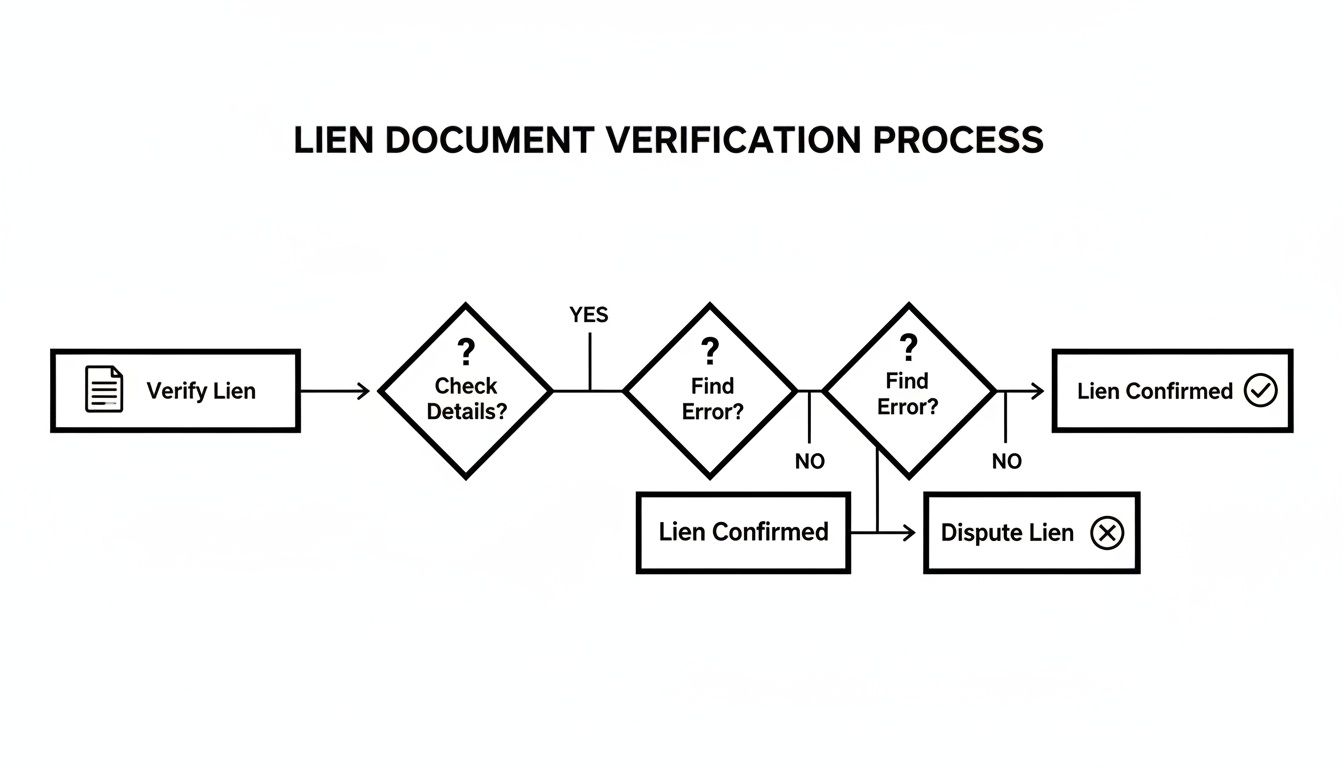

Alright, so you’ve discovered there’s a lien on your property. What’s next? It's time to roll up your sleeves and really dig into the lien document itself.

This piece of paper can look pretty intimidating at first, full of dense legal jargon. But think of it as your roadmap—it holds every critical detail you need to figure out your game plan and get that lien removed for good. The lien filing isn't just a notice; it's a specific claim spelling out who says you owe them money, exactly how much, and why. You absolutely have to master these details before you even think about paying, negotiating, or fighting the claim.

What to Look For in the Lien Document

First things first, you need a copy of the official document. For property owners here in Fayetteville and Cumberland County, that means a trip to the Cumberland County Register of Deeds office or a quick search on their online portal.

Once you have it in hand, you're hunting for a few key pieces of information:

- The Lienholder's Name and Address: Who exactly filed this? It could be a contractor, a lawyer for a credit card company, or a government agency. The document will tell you.

- The Original Debt Amount: There will be a specific number listed as the principal debt. This is the foundation of their entire claim.

- Extra Fees and Interest: Is the total amount more than the original debt? Look closely for any mention of accrued interest, late penalties, attorney’s fees, or other charges they’ve tacked on.

- Filing Date: The date the lien was officially recorded is super important. In North Carolina, there are strict deadlines, and a late filing could make the lien invalid.

Don't Just Read It—Verify Everything

Getting the information is one thing; making sure it's correct is where you can really gain some ground. Never assume the details on a lien are 100% accurate. Mistakes happen more often than you’d think, from a simple typo to a major miscalculation.

It’s time to do some homework. Pull out your own records—contracts, invoices, canceled checks, emails, anything related to the debt. Let’s say a contractor in Fayetteville slapped a mechanic's lien on your house for $10,000. If your records show you already paid $8,000 and they never even finished the job, you’ve just found your starting point for a dispute.

Pro Tip: Don't ever accept the total on a lien at face value. Your first move should be to demand an itemized breakdown from the creditor. This forces them to justify every single dollar, especially interest and fees, which is often where you'll find errors or charges they can't back up.

Found a Mistake? Here’s What to Do Next.

Finding an error is a game-changer. It gives you immediate, solid grounds to challenge the lien, putting you in a much stronger position. Whether it’s the wrong amount, an incorrect name, or they missed a legal deadline, your path forward becomes much clearer.

- Gather Your Proof: Get all your evidence together. This means payment receipts, bank statements, emails, photos—anything that proves their claim is wrong.

- Contact the Lienholder (Formally): Don’t just call them. Send a formal, written notice explaining the error you found. It's best to use certified mail so you have proof they received it. Include copies of your evidence.

- Demand They Fix It or Remove It: In your letter, state clearly that you want them to either correct the filing to show the right information or, better yet, file a "Satisfaction of Lien" to release the wrongful claim entirely.

If the lienholder digs in their heels and refuses to cooperate, you might have to take it to the next level. But honestly, most creditors will back down once you present clear evidence of a mistake. They know that trying to enforce a flawed lien is a losing battle that could even get them penalized. This careful verification process is your first, and often most powerful, line of defense.

Alright, once you've done the digging and confirmed a lien on your property is legit, it’s time to switch gears from detective work to taking action. You’ve got a few different paths to get that lien off your title. The best one for you really depends on your financial situation and how quickly you need to move.

Making the right choice here is everything. It’s about resolving the issue without wasting time or money and finally getting your property free and clear. The whole process, from finding the lien to checking for mistakes, sets you up for the strategic choices we're about to break down.

As you can see, once you've verified the lien and double-checked the details, you hit a fork in the road. If you spot an error, you dispute it. But if it’s valid, you’re looking at one of these options.

Option 1: Pay the Debt in Full

Let's start with the most direct route: paying off the debt completely. It’s clean, it’s simple, and it’s final. While it obviously requires having the cash on hand, this method guarantees the fastest resolution and stops any more interest or penalties from piling up.

Your first move is to contact the lienholder and ask for a formal payoff letter. This isn't a "nice-to-have"; it's a must. This document spells out the exact amount needed to settle everything, including interest and fees, as of a specific date. Never, ever send a payment without this official letter.

Once you pay, the lienholder is legally required to give you a “Satisfaction of Lien” or “Lien Release.” This paper is your golden ticket. You must file it with the Cumberland County Register of Deeds to officially scrub the lien from your property's record. If you skip this final step, the lien will just sit there, continuing to cloud your title.

Option 2: Negotiate a Settlement

What if you just don’t have the full amount? Don't panic. Negotiation is a powerful tool, and you might be surprised at how often it works. Many creditors would rather get a guaranteed lump-sum payment now than drag out a collection process that’s long, uncertain, and costs them money.

When you reach out, be prepared, polite, and professional. Explain your situation honestly and make a reasonable offer. A good starting point is often offering to pay 50-70% of the total debt in one single payment.

I’ve seen this work firsthand. A creditor knows you're in a tight spot—maybe a military family at Fort Liberty with sudden PCS orders—they might be more willing to take a lower settlement to get the deal done before you relocate. It’s all about leverage.

Before you send a dime, get the settlement agreement in writing. That document needs to state clearly that your payment satisfies the entire debt and that they will issue a Satisfaction of Lien once they receive it. This is your protection against any future claims.

Option 3: Wait Out the Statute of Limitations

This one is a bit of a long shot. In North Carolina, creditors have a limited time to enforce certain liens through the courts. For a judgment lien, that window is typically 10 years. If they don’t take action to collect within that decade, the lien can expire.

Honestly, this is a risky strategy. Creditors can often renew judgment liens, which resets the clock. Plus, the lien stays on your title that whole time, making it impossible to sell or refinance. It’s a passive approach that leaves you stuck in limbo for years, so it’s not a practical solution for most homeowners.

When Liens Get in the Way of a Sale

The pressure really cranks up when you need to sell. Liens can bring a sale to a screeching halt, especially when the market is tough. We’re seeing this problem more and more. For example, ATTOM’s latest report showed 28,269 foreclosure starts across the country, a whopping 46% jump from the previous year. Nearby states like South Carolina and Florida are getting hit hard, which tells us these financial pressures can easily spill over into the Fayetteville market. You can see the full numbers in the complete foreclosure activity report on attomdata.com.

It can feel hopeless when the sale price won't even cover what you owe on the lien, and you don’t have the cash to clear it yourself. These situations get even more tangled with multiple properties or ownership transfers. If you’re trying to navigate title issues, you might find some useful info in our guide on how to file a quitclaim deed.

Sometimes, paying off a lien just isn't in the cards. It can feel like you've hit a brick wall when a financial crunch makes settling the debt impossible. But you're not out of options.

There are a few other, more complex legal routes you can take to get a lien off your property. These aren't simple fixes—they often require a lawyer's help—but they can clear the path forward when you're truly stuck.

These strategies go beyond basic negotiation and step firmly into the legal arena. They’re designed for situations where you doubt the lien is even valid, your finances are in a tough spot, or you need to shift debt priorities around to get a new loan. Knowing what’s available is the first step to protecting your property.

Challenging the Lien in Court

Think the lien is bogus? If you have solid proof that it's invalid—maybe it was filed incorrectly, the bill was already paid, or it's just plain fraudulent—you can go on the offensive. This means filing a lawsuit called a quiet title action.

A quiet title action essentially asks a North Carolina court to rule on who truly owns the property, wiping out any bogus claims against it. It's a powerful move, but it's not a walk in the park.

You'll need to build a strong case with solid proof, like:

- Proof of payment, such as canceled checks or bank statements.

- Written correspondence that contradicts what the lienholder is claiming.

- Evidence that the creditor didn’t follow North Carolina's strict lien filing rules, like missing a deadline for a mechanic's lien.

This kind of legal fight can drag on and get expensive, so it's best reserved for when the lien is for a significant amount and you're confident in your evidence. If you win, you get a court order that removes the lien from your property records for good.

The Impact of Filing for Bankruptcy

Filing for bankruptcy is a huge financial step, and it can definitely affect property liens. But it’s not a magic eraser. The outcome really depends on the kind of lien and which type of bankruptcy you file.

For instance, filing for Chapter 7 or Chapter 13 bankruptcy can sometimes get rid of judgment liens on your property. This is done through a process called "lien stripping" or "lien avoidance." It’s often possible if the lien gets in the way of an exemption you're allowed to claim under bankruptcy law.

A lot of people think bankruptcy wipes out every single debt. It doesn't. While it can discharge unsecured debts and remove certain judgment liens, it almost never removes consensual liens (like your mortgage) or statutory liens, like federal and state tax liens. Those debts tend to stick around even after bankruptcy.

Requesting Lien Subordination

So, what if you're not trying to kill the lien, but you just need to refinance or get a new loan? A junior lien (like one from a second mortgage or a court judgment) can stop a new loan in its tracks because lenders always want to be first in line to get paid if you default.

The solution here could be lien subordination.

Subordination doesn't get rid of the lien. It’s just a legal agreement where the current lienholder agrees to step back in line, letting your new lender take the front-of-the-line spot. If you're refinancing your primary mortgage, the new lender will demand first priority. You'd have to persuade the holder of that second-priority judgment lien to sign a subordination agreement, letting them stay on the title but behind the new mortgage.

Getting a creditor to agree to this can be tough. You'll need to show them how the refi is a win for everyone—maybe by lowering your monthly payments so you're more likely to pay off all your debts, including theirs.

Frankly, for a lot of homeowners, the stress isn't worth it. The ability to sell a house with a lien and have the debt cleared at closing is a much simpler solution. Our guide on selling a house with a lien dives deeper into how that works.

Selling Your Property to a Cash Buyer for a Fast Solution

Sometimes the traditional methods for dealing with a lien just don’t make sense. They can be slow, legally confusing, and—most importantly—require cash you simply don’t have on hand. For homeowners who need a clean, fast exit, there’s a powerful alternative: selling your property directly to a cash home buyer.

This approach flips the script entirely. Instead of you scrambling to find the funds to pay off the debt before a sale, the buyer handles the lien as part of the transaction. It's a true game-changer for owners who feel trapped by a title problem.

How a Cash Sale Unlocks Your Equity

The process is built for speed and simplicity. You reach out to a local cash buying company, like DIL Group, and we’ll assess your property and the lien details. Within a day or two, you’ll get a no-obligation, all-cash offer for your house in its current “as is” condition.

If you accept, the real magic happens at closing. The title company uses the sale proceeds to pay the lienholder directly, satisfying the debt for good. The remaining money—your equity—goes straight into your pocket. You walk away with cash in hand, and the lien is gone forever without you spending a single penny out-of-pocket.

This is an incredibly effective solution, especially for situations we see all the time here in Cumberland County.

- Military Families: Service members at Fort Liberty facing sudden PCS orders need a fast, guaranteed sale. A lien can’t be allowed to slow things down.

- Tired Landlords: If you're managing problem tenants in Hope Mills or Spring Lake, selling for cash means you avoid messy evictions and drawn-out legal fights.

- Inherited Properties: When you inherit a home with unexpected debts, a cash sale provides a clean, simple break from the responsibility.

The Real-World Benefits of a Cash Sale

This strategy is about more than just speed; it’s about certainty and convenience when you need them most. The traditional market is unpredictable, but a cash sale eliminates the common hurdles that derail deals when liens are involved.

The biggest advantage? You sell your house completely as is. No repairs, no cleaning, no staging for showings. The buyer takes on all of that.

A cash sale offers a definitive solution. You get a guaranteed closing date, a firm price, and the assurance that the lien will be paid off by professionals at closing. It removes all the stress and uncertainty from an already difficult situation.

You also avoid the typical costs of selling a house. There are no realtor commissions, which can save you 5-6% right off the top. You also skip the seller-paid closing costs. It’s all bundled into one straightforward transaction.

Imagine owning a home in Fayetteville only to discover a stubborn tax lien is preventing you from selling. It’s a nightmare scenario that’s more common than you’d think. Prolonged liens can damage your credit—a problem that affected roughly 357,000 properties in 2023. For out-of-state owners or military families, that’s a risk you can’t afford. You can get more details on U.S. foreclosure trends and their impact on homeowners at rei-ink.com.

A Direct Comparison of Your Options

Seeing your choices side-by-side can make the best path forward crystal clear. While paying or negotiating a lien yourself has its place, selling to a cash buyer offers a distinct set of advantages when time and money are tight.

Comparing Lien Removal Methods Traditional vs Selling for Cash

| Factor | Traditional Removal (Payoff/Negotiate) | Selling to a Cash Buyer |

|---|---|---|

| Upfront Costs | Often requires thousands of dollars out-of-pocket to pay the debt. | $0. The lien is paid from the sale proceeds at closing. |

| Timeline | Can take weeks or months of negotiation and legal filings. | Typically closes in 7-21 days, on your schedule. |

| Repairs & Prep | You may need to repair the home to attract a traditional buyer. | None. You sell the property in its current condition. |

| Certainty | Deals can fall through due to financing or appraisal issues. | Guaranteed sale. The offer is cash, with no financing contingency. |

| Commissions | Standard realtor commissions of 5-6% apply. | $0. There are no agent fees or hidden costs. |

Ultimately, selling your home to a cash buyer is about taking back control. It provides a reliable and efficient way to resolve a property lien, unlock your home's equity, and move on with your life. If you want a deeper look, our guide on how to sell your home for cash breaks down the entire process.

Your Top Questions About North Carolina Property Liens, Answered

When you find out there’s a lien on your property, your mind starts racing. It’s a nerve-wracking situation, and the legal jargon can feel like a foreign language. To help you get your bearings, we’ve tackled some of the most common questions we hear from homeowners right here in the Fayetteville area.

Getting a handle on these key points will give you the confidence you need to get that lien off your property for good.

How Long Does a Lien Stay on Your Property in North Carolina?

The clock on a lien in North Carolina is completely different depending on what kind it is—which is exactly why you need to know what you’re up against.

A judgment lien, for example, usually sticks around for 10 years from the day the court handed it down. What’s worse, the creditor can try to renew it for another decade, keeping that dark cloud over your property title for a long, long time.

On the flip side, a mechanic’s lien has a much shorter fuse. A contractor has to file a lawsuit to enforce it, and they typically only have 120 days from their last day of work to do it. If they drop the ball, that lien becomes useless. But tax liens? They're the most stubborn of all and can hang around indefinitely until you settle the tax bill.

Key Takeaway: Don't ever assume a lien will just vanish. Some have expiration dates, but others, especially tax liens, aren’t going anywhere until you deal with the debt head-on.

Can I Sell My House if There Is a Lien on It?

Yes, you can definitely sell a house with a lien, but here's the non-negotiable part: the debt must be paid off at or before closing. Plain and simple. The next owner needs a clean title, which means every single claim against the property has to be wiped out.

In a normal sale, the money you make from selling the house is used to pay the lienholder. The title company manages this, making sure the creditor gets paid before you see a dime. The real trouble starts when the sale price isn't high enough to cover your mortgage and the lien. That's a deal-killer right there.

This is where a cash buyer makes all the difference. We make an offer that already has the lien factored in, and the payoff is handled smoothly at closing. You don't need a penny out of pocket.

What Is a Satisfaction of Lien and Why Do I Need It?

A Satisfaction of Lien (sometimes called a lien release) is the golden ticket. It's the official piece of paper that proves you've paid what you owed. Think of it as your receipt for clearing the claim. Once you pay the lienholder, they are legally required to give you this document.

But just getting the release isn't the final step. You have to take that document and file it with the Cumberland County Register of Deeds. This is what officially scrubs the lien from your property's public record. If you forget this part, that lien will keep popping up on title searches, stopping you from selling or refinancing down the road.

Will Removing a Lien From My Property Improve My Credit Score?

Getting a lien removed can definitely help your credit score, but it's an indirect boost. The lien itself doesn't show up on your personal credit report (like your FICO score), but the debt behind it almost always does. For instance, a court judgment for an old credit card bill is a major black mark on your credit history.

When you pay off that debt to get the lien removed, the negative account on your credit report is updated to "paid" or "satisfied." That’s a positive change that stops the bleeding and prevents future damage from collections, wage garnishments, or even foreclosure.

Feeling buried by a property lien in Fayetteville? You don't have to go through this alone. DIL Group Home Buyers is in the business of buying homes with liens. We handle all the headaches so you can walk away with cash. We buy houses in any condition, pay off the debts at closing, and help you move on. Get your fair, no-obligation cash offer today at https://dilgrouphomebuyers.com.