Facing foreclosure is one of the most terrifying things a homeowner can go through. We see it all the time. The biggest question people have is, "What happens to my house if I file for bankruptcy?"

The answer is simple: filing for bankruptcy puts an immediate stop to any foreclosure. It’s a powerful legal move called the automatic stay. Think of it as a court-ordered “pause button” that gives you some desperately needed breathing room to figure things out.

The Automatic Stay: Your Home's First Line of Defense

When you're caught in a financial storm, the constant creditor calls and scary foreclosure notices feel like they’ll never end. But the second you file for bankruptcy here in North Carolina, the court issues an automatic stay.

It’s like an instant legal ceasefire.

This protection is immediate and stops almost every collection activity against you and your property. From the moment your case is filed, the following must stop cold:

- Foreclosure Proceedings: The bank has to postpone any scheduled foreclosure sale. They can’t move forward with taking your home.

- Harassing Phone Calls: Creditors and their collection agencies are legally forbidden from contacting you. The phone will finally stop ringing.

- Lawsuits and Wage Garnishments: Nearly all legal actions against you are frozen right where they are.

Key Insight: The automatic stay is your most powerful first move. It brings immediate relief and opens up a crucial window of time to build a real, long-term strategy for your home.

This pause button works whether you file for Chapter 7 or Chapter 13 bankruptcy, giving every homeowner in Fayetteville and across Cumberland County a chance to catch their breath.

But this is just the beginning. The stay buys you time, but what happens to your house in the long run depends entirely on which type of bankruptcy you choose. If you're facing an imminent foreclosure auction, you need to understand the difference. You might also want to read our guide on how to stop foreclosure on my home.

Let's quickly look at what happens right away and what each chapter means for your house down the road.

Immediate Effects of Filing Bankruptcy on Your Home

This table gives you a quick snapshot of the protections you get right away and how the two main bankruptcy chapters handle your home long-term.

| Action | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy |

|---|---|---|

| Foreclosure | Immediately Halted. The automatic stay stops the sale, but this is temporary. You must have a plan to address the mortgage long-term. | Immediately Halted. The stay stops the sale, and the repayment plan is specifically designed to help you catch up on missed payments. |

| Creditor Contact | Immediately Stops. All creditor calls, letters, and lawsuits must cease. | Immediately Stops. All creditor calls, letters, and lawsuits must cease. |

| Long-Term Goal | Liquidation. Sells non-exempt assets to pay debts. Keeping your home depends on equity and exemptions. | Reorganization. Creates a 3-5 year repayment plan to catch up on debts, including your mortgage, while keeping your property. |

As you can see, both paths offer immediate relief, but they lead to very different outcomes.

Two Paths to Protection

The automatic stay kicks off two very different journeys for your home:

- Chapter 7 Bankruptcy: This is known as a liquidation bankruptcy. The stay gives you some time, but whether you can keep your house permanently comes down to how much equity you have and what you can protect under North Carolina's exemption laws.

- Chapter 13 Bankruptcy: This is a reorganization. It's built specifically to help people catch up on missed mortgage payments over a three- to five-year period. This makes it a very powerful tool for saving your home from foreclosure.

The initial ceasefire is the same for both, but the long-term battle plan for keeping your home is decided by the chapter you file. The stay gives you the time to make that critical decision without the immediate threat of losing your house.

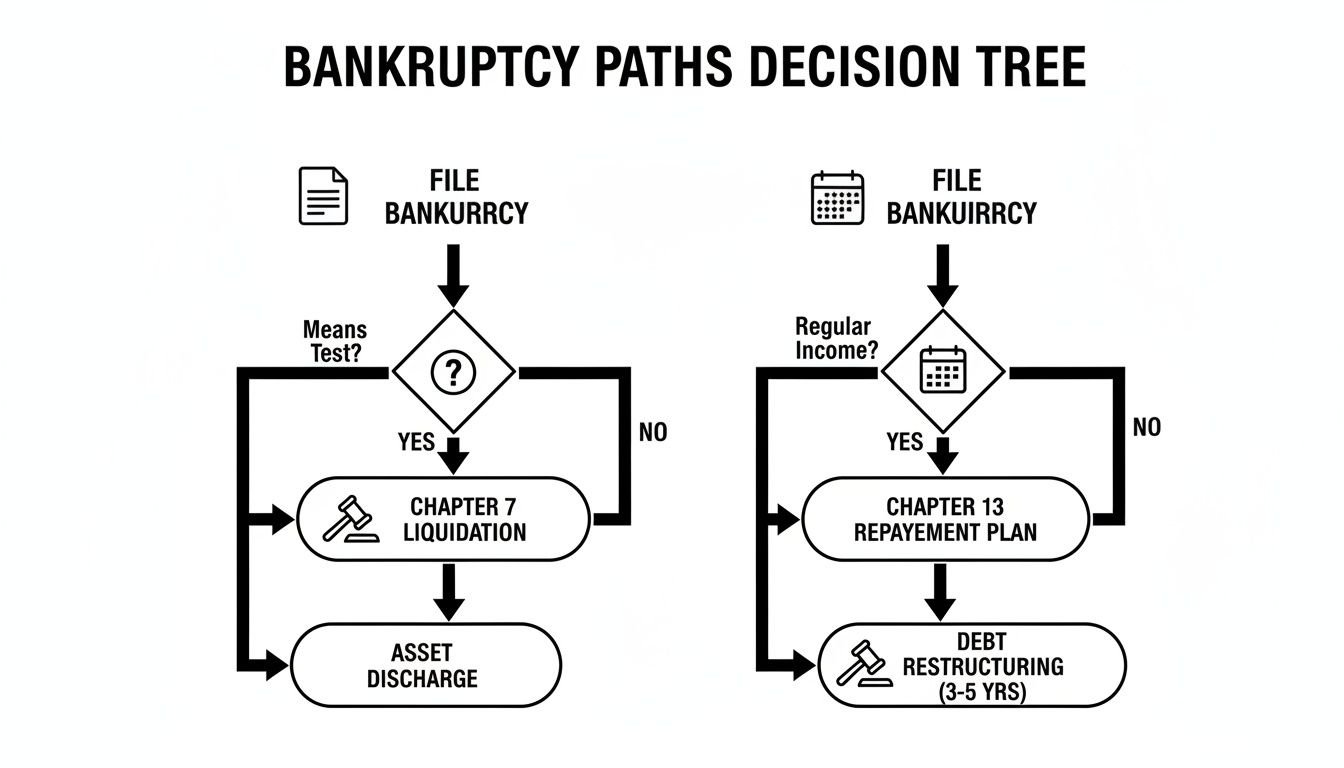

Chapter 7 vs. Chapter 13: Which Path Protects Your Home?

The automatic stay is a powerful first step, but it’s really just a temporary pause button. What happens to your house in the long run comes down to one massive decision: filing for Chapter 7 or Chapter 13 bankruptcy.

These are two completely different roads. Choosing the right one is absolutely critical if you want to keep your home. Think of Chapter 7 as a quick, clean break, while Chapter 13 is more like a structured workout plan to get your finances back in shape. Each has huge implications for your property.

Chapter 7: The Liquidation Path

Chapter 7 is often called "liquidation" bankruptcy for a reason. A court-appointed trustee takes a hard look at your assets to see what can be sold off to pay your creditors. It's the faster route, usually wrapping up in just a few months.

When it comes to your house, everything boils down to one word: equity. That’s the difference between your home’s market value and what you still owe on the mortgage. It’s the portion you actually "own."

If you have very little equity, or if the equity you do have is protected by a North Carolina bankruptcy exemption, the trustee likely won’t bother with your house. There's just no money in it for the creditors. But here’s the risk: if you have significant non-exempt equity, the trustee can and will sell your home. They’ll hand you the cash for your exempt amount and use the rest to pay off your debts. This makes Chapter 7 a huge gamble if your main goal is saving a home you’ve been building equity in for years.

Chapter 13: The Reorganization Path

Chapter 13 bankruptcy is a whole different ballgame. It’s a "reorganization" built for people with steady income who are determined to keep their property, especially their house.

Instead of selling off your assets, you create a repayment plan that gets approved by the court. Over the next three to five years, you make structured payments to catch up on what you owe.

This is the path designed to stop foreclosure dead in its tracks. It lets you take all your past-due mortgage payments and spread them out over the life of the plan. Your new single monthly payment to the trustee will cover your current mortgage payment plus a piece of the arrears.

A Chapter 13 plan is a clear roadmap to saving your home. It forces the lender to accept a structured repayment of what you owe, providing a predictable way to get current and keep your property long-term.

For most homeowners falling behind on their mortgage, Chapter 13 is by far the safer bet. It’s designed specifically to solve the problem of mortgage arrears, and the numbers don't lie.

This chart helps visualize the two very different outcomes.

As you can see, Chapter 7 puts your assets at risk of being sold, while Chapter 13 is built around a plan to let you keep them.

Research shows that filing for bankruptcy is incredibly effective at preventing foreclosure. Homeowners who are behind on payments and file for bankruptcy are about 70 percent less likely to see their home sold at auction. But the type of bankruptcy matters immensely. Homeowners who choose Chapter 13 are five times less likely to lose their home compared to those who file Chapter 7.

Why the huge difference? Chapter 13 has a built-in cure for mortgage default. Chapter 7 only provides that temporary stay without a real plan to get current.

Of course, a Chapter 13 plan means committing to years of consistent payments. If you're worried about keeping up with that commitment, it's smart to look into all your options, including other mortgage payment assistance programs that might offer relief.

Bottom line: Chapter 7 can work if you’re current on your mortgage and don’t have much equity. But if you’re already facing foreclosure notices, Chapter 13 is the specific tool designed to get you back on your feet and keep you in your home.

Understanding North Carolina's Homestead Exemption

When you're weighing Chapter 7 vs. Chapter 13, one of the biggest things you have to wrap your head around is bankruptcy exemptions. This isn't just legal jargon—it's what could save your house.

Think of an exemption like a legal shield you get to place over your property. State law gives you this shield to protect certain assets, keeping them out of the hands of the bankruptcy trustee who wants to sell them off to pay your debts.

For any homeowner in Fayetteville, Hope Mills, or anywhere else in North Carolina, the most important shield you have is the North Carolina homestead exemption. It’s the rule that directly protects the equity in your primary home and ultimately decides if the trustee can force a sale in a Chapter 7.

How Much Equity Can You Protect in North Carolina?

The law in North Carolina is pretty specific about how much of your home's equity you can shield from creditors. These numbers are there to give everyday homeowners a fighting chance to keep their homes, as long as their equity isn't too high.

Right now, the homestead exemption lets you protect:

- $35,000 in home equity for an individual filer.

- $70,000 in home equity if you're a married couple filing together.

This applies to your main residence, whether it's a traditional house, a condo, or a mobile home. If the equity you have is less than this amount, the Chapter 7 trustee can't touch your home. There’s simply no unprotected value there for them to go after for your creditors.

Calculating Your Home Equity Step-By-Step

So, how do you know if your house is safe? You need to do some quick math. Figuring out your home equity is simple and will tell you exactly where you stand.

Just use this formula:

Market Value – Mortgage Balance = Your Home Equity

That's it. First, get a realistic idea of what your home could sell for on the market today. Then, subtract what you still owe on the mortgage and any other loans tied to the house, like a home equity line of credit (HELOC).

Let’s look at an example:

Say your house in Hope Mills could sell for $250,000. You have $220,000 left on your mortgage.$250,000 (Market Value) – $220,000 (Mortgage Balance) = $30,000 (Your Home Equity)

If you're filing bankruptcy by yourself, your $30,000 in equity is completely covered by North Carolina's $35,000 exemption. The trustee can't sell your house. You're safe.

When Your Equity Exceeds the Exemption Limit

But what happens if your equity is higher than the exemption? This is where things get serious. Any equity above the limit is called non-exempt equity—it’s the part the legal shield doesn't cover, and the trustee can grab it.

Let's use that same house but change the numbers. Your home is still worth $250,000, but you’ve paid down your mortgage to $190,000.

- $250,000 (Market Value) – $190,000 (Mortgage Balance) = $60,000 (Your Home Equity)

As a single filer, you can only protect $35,000 of that equity. The other $25,000 is non-exempt and up for grabs.

In this situation, the trustee will almost certainly move to sell your home. They’ll sell it for $250,000, pay the bank its $190,000, hand you a check for your protected $35,000, and use the remaining $25,000 to pay back your other creditors. This is the biggest risk of filing Chapter 7 when you have too much equity in your home.

The Wildcard Exemption: An Extra Layer of Protection

North Carolina does throw you one more lifeline: the "wildcard" exemption. It’s a flexible tool that can sometimes save the day.

If you haven’t used up all of your other exemptions, you can apply up to $5,000 of your unused homestead exemption to any other property. That includes adding it on top of your standard homestead exemption to protect a little more equity. It’s not a huge amount, but sometimes, that extra $5,000 is all it takes to put you under the limit and keep your house safe.

Deciding Your Mortgage's Fate: Reaffirm, Redeem, or Surrender

Okay, so you’ve picked your bankruptcy chapter and figured out how exemptions can protect your home’s equity. Now you’re at a major fork in the road. Filing for bankruptcy doesn’t mean the court just decides what happens to your mortgage. You actually have to tell them what you want to do with the debt, giving you more control than you might think.

This decision comes down to three paths: reaffirming the loan, redeeming the property, or surrendering it. Each one has huge, long-term consequences for your finances, so it’s critical to understand what you’re getting into.

Option 1: Reaffirm Your Mortgage Debt

If you want to keep your house, the most common route is to reaffirm the mortgage. Think of it as formally re-upping your commitment to the loan. You’re essentially signing a new agreement that pulls the mortgage debt completely out of the bankruptcy process.

By reaffirming, you’re stuck with the original loan terms. The debt is no longer part of your bankruptcy discharge, which means you have to keep making payments exactly as before. The upside is that the lender will keep reporting your payments to credit bureaus, which can slowly help you rebuild your credit.

But be careful. This path has serious risks. If you default on the mortgage after the bankruptcy is over, the lender can still foreclose. And because you reaffirmed, they can hit you with a deficiency judgment—suing you for the difference between what the house sells for and what you owed. You lose all the protection the bankruptcy offered for that specific debt.

Option 2: Redeem Your Property

Redemption is a less-known but powerful move, though it's only available in a Chapter 7 bankruptcy. It lets you "redeem" the house by paying the lender its current fair market value—not the full mortgage balance—in one giant, lump-sum payment.

Here’s an example. Let's say your home is worth $200,000, but your mortgage balance is still $240,000. Redemption would allow you to pay the lender $200,000 cash. The extra $40,000 you owed is then wiped out in the bankruptcy, and you own the house free and clear.

Key Takeaway: Redemption sounds amazing if you’re "underwater" on your mortgage. But the catch is huge: you have to come up with the entire market value in one shot. For most people filing bankruptcy, that’s just not realistic.

Option 3: Surrender Your House

Your final option is to surrender the property. This means you’re giving the house back to the lender and walking away from the mortgage debt for good. When you surrender a home in bankruptcy, your personal responsibility for that loan is completely eliminated by the discharge.

This is the right strategic move for homeowners in a few tough spots:

- You're seriously underwater: If you owe way more than the house is worth, surrendering lets you ditch a bad investment and start fresh.

- You just can't afford the payments: If the mortgage is breaking your budget every month, surrendering gives you a clean financial break.

- The house needs a ton of repairs: If you’re facing a money pit you can’t afford to fix, letting it go might be the smartest decision.

Once you surrender, the lender will eventually foreclose to get the title back. The key difference is that they can't come after you for any leftover debt. Bankruptcy gives you a complete exit. In some cases, a lender might even be open to a deed in lieu of foreclosure to avoid a long, drawn-out process.

Ultimately, choosing between reaffirming, redeeming, or surrendering is a pivotal moment. It forces you to take a hard, honest look at your home's real value, your budget, and what you want your financial future to look like.

When Bankruptcy Isn't the Right Answer

Sometimes, after you’ve looked at all the rules and done the math, you hit a wall. You realize that bankruptcy, for all its potential benefits, just isn't the right path for you.

For many homeowners, the answer to "what happens to my house?" is a dealbreaker. Maybe your home has too much equity that isn't protected, putting a giant target on it for the trustee in a Chapter 7. Or maybe the monthly payments for a Chapter 13 plan are just too steep to commit to for three to five years.

For others, the goal is simply a clean break—without the long shadow that bankruptcy casts over your credit for years to come.

When Filing Creates More Problems

Bankruptcy can be a lifeline, but it's not a magic wand for every situation. It can end up being the wrong move.

- Too Much Equity for Chapter 7: If the value of your home is well over North Carolina's homestead exemption, filing for Chapter 7 is practically a guarantee the trustee will sell it. You'll get a check for your exempt amount, sure, but you'll lose your house.

- Unaffordable Chapter 13 Plan: A Chapter 13 repayment plan hinges on having a stable, predictable income. If you're facing a job loss, a military PCS, or any other life event that makes a five-year payment commitment feel impossible, the plan will probably fail. You’ll end up right back where you started, but with foreclosure looming even closer.

- You Just Need a Fast, Clean Exit: Bankruptcy is a long, public, and frankly, stressful process. If you’re dealing with an inherited problem property, a sudden job relocation, or a house with overwhelming repair needs, you need a solution that’s faster and more certain.

An Alternative Path to Financial Freedom

If you're in one of these tough spots, it’s easy to feel like you have no good options left. But there is another way—an alternative that puts you back in the driver's seat: selling your house "as-is" to a cash home buyer.

Instead of waiting for a court or a bank to decide your home's fate, you take decisive action. This strategy lets you sell your house fast, sometimes in just a couple of weeks, without lifting a hammer or dealing with real estate agents, showings, and open houses.

A direct cash sale is about taking control. It’s a way to access your home’s equity before foreclosure or bankruptcy takes it, avoid a foreclosure on your credit record, and secure a certain outcome on your timeline.

For a homeowner in Fayetteville staring down a PCS move, or someone in Hope Mills who just inherited a house they can't afford to keep, this offers immediate relief. You get a guaranteed cash offer, you pick the closing date, and you walk away with cash in hand and a fresh start.

Don't forget the long-term damage of bankruptcy. The process can tank a credit score by 200 to 300 points, making it incredibly hard to get another mortgage for years. Research actually shows that homeowners who file for bankruptcy are about 28 percent more likely to lose their homes anyway compared to similar homeowners who don't file.

With only about 33 percent of people who file managing to keep their homes in the long run, the odds can feel stacked against you. You can explore more of the research on how bankruptcy affects homeowners to get the full picture. A fast cash sale completely sidesteps that credit hit and gives you the clean slate you need.

Your Top Questions About Bankruptcy and Your Home, Answered

Going through the nuts and bolts of Chapter 7 and Chapter 13 is one thing, but you probably still have some very specific questions about what it all means for your house. Bankruptcy can get complicated, and every homeowner's situation in the Fayetteville area is a little different.

Let's cut through the noise and get you some straight answers to the questions we hear all the time. Our goal is to give you the clarity you need to make the right next move.

Can I Just Sell My House Before I File for Bankruptcy?

Yes, you absolutely can sell your house before filing. But you have to be careful and completely upfront about it. Selling your home isn't the problem; it's how you sell it that the bankruptcy court cares about.

The most important rule is that you must sell for fair market value. If you try to sell your house to a buddy or a family member for way less than it's worth, the trustee will immediately flag it as a "fraudulent transfer." They see it as trying to hide an asset, and they have the power to reverse the sale and pull that house right back into the bankruptcy.

But making a smart, legitimate sale to a cash buyer for a fair price? That's a different story. It's a strategy that puts you in control and lets you get your hands on your equity. Just make sure you talk to a bankruptcy attorney before the sale to handle everything by the book.

What Happens to My Second Mortgage or HELOC?

What happens to a second mortgage or a Home Equity Line of Credit (HELOC) all comes down to two things: what your house is worth and which bankruptcy chapter you file. These are "junior liens," meaning they're second in line to get paid after your main mortgage.

Here’s the breakdown:

- In Chapter 13: If your home's value has tanked and it's now worth less than what you owe on just your first mortgage, you get access to a powerful move called "lien stripping." Your attorney can ask the court to change the second mortgage's status to unsecured debt—the same category as credit cards. It gets rolled into your repayment plan, and you often only pay back a tiny piece of it.

- In Chapter 7: Lien stripping is not an option. Chapter 7 might wipe out your personal responsibility to pay the second mortgage, but the lien itself sticks to your property like glue. If you ever want to sell or refinance, you'll have to pay off that second mortgage to clear the title.

Here's the Key Difference: Chapter 13 can actually remove the lien from your property's title if you're underwater. Chapter 7 only removes your personal obligation to pay, leaving the lien itself behind to cause problems later.

What If My Chapter 13 Plan Falls Apart?

A Chapter 13 bankruptcy is a marathon, not a sprint. You’re committing to a three- to five-year repayment plan. But life happens. A job loss, a medical crisis—if something stops you from making those payments, your entire case could get dismissed.

The second a Chapter 13 is dismissed, the automatic stay disappears. Your mortgage lender can pick up foreclosure proceedings right where they left off. Suddenly, you're back in the hot seat, but you aren't out of options yet.

You could try switching to a Chapter 7 if you qualify, which would get rid of your other debts. But that won't do anything to stop the foreclosure.

A much better plan is to sell the house fast, before the bank can auction it off. A quick cash sale can pay off the mortgage, stop the foreclosure from destroying your credit, and maybe even let you walk away with some cash from your equity.

Will Bankruptcy Stop an Eviction If I'm Renting?

Yes, filing for bankruptcy can hit the pause button on an eviction, but that pause is usually very brief. The automatic stay freezes an eviction process just like it freezes a foreclosure.

But don't get too comfortable. Your landlord can immediately ask the bankruptcy court to "lift the stay" and let them move forward with the eviction. Judges usually approve these requests quickly, especially if you were already behind on rent when you filed.

Even worse, if your landlord in North Carolina already got a judgment for possession before you filed, the automatic stay might not help you at all. Bankruptcy might buy you a few extra days or a week, but it’s not a real, long-term fix for stopping an eviction.

Feeling crushed by the thought of foreclosure or tangled up in bankruptcy? You don’t have to figure this out on your own. If you need to take back control with a guaranteed, fast, and fair solution, DIL Group Home Buyers is here to help. We buy houses in any condition all over the Fayetteville area, giving you a simple path to your equity and a way out of foreclosure. See how you can get a no-obligation cash offer and close when you're ready at https://dilgrouphomebuyers.com.