When you can't make your mortgage payment, it feels like the whole world is caving in. The first missed payment kicks off a chain reaction of serious problems, starting with late fees and a major hit to your credit score.

If you keep missing payments, the lender will eventually start the formal foreclosure process. This isn't just about money—it's an incredibly stressful ordeal that can end with you losing your home at a public auction.

What Really Happens When You Default on a Mortgage?

Facing a mortgage default is terrifying. Think of that first missed payment like a small snowball at the top of a hill. If you don't stop it right away, it starts rolling, getting bigger and faster until it becomes a full-blown avalanche of financial trouble. It doesn’t all happen in a single day, but it follows a predictable—and often unforgiving—path.

For homeowners here in Fayetteville and across North Carolina, knowing this timeline is the first step to getting back on your feet. The journey from one late payment to foreclosure has several stages, each with its own set of challenges and, importantly, opportunities to take action. It all starts with the lender trying to collect what's owed before things escalate to legal proceedings.

The Immediate Consequences

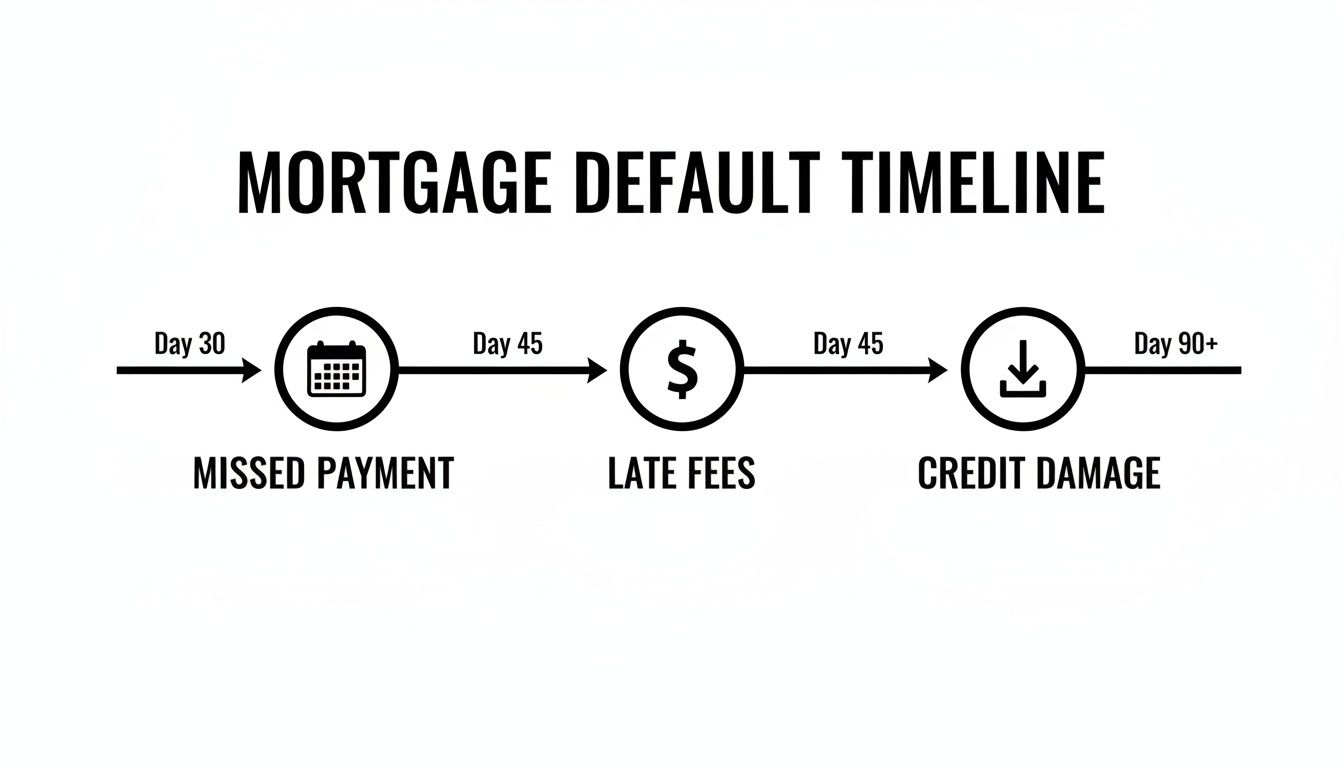

The first hits are almost instant and land right in your wallet. Your lender will tack on late fees, and as soon as you hit 30 days past due, they report it to the credit bureaus. That one report can tank your credit score by 100 points or more, making it incredibly difficult and expensive to get a loan for anything in the future.

As the missed payments pile up, the lender’s calls and letters get more and more serious. They'll go from friendly reminders to stark warnings about foreclosure. If you're in this spot, know you’re not the only one; plenty of families are going through the same thing.

A recent report from the Mortgage Bankers Association showed that the U.S. mortgage delinquency rate jumped to 3.99% of all loans. That means thousands of families are dealing with the same challenges you might be facing. You can read more about these mortgage delinquency statistics to see the bigger picture.

Let's break down exactly what happens in those first critical months.

Here’s a look at the initial chain of events when a homeowner defaults on their mortgage. Understanding these first steps is crucial because the early stages offer the most flexibility for finding a solution.

Immediate Consequences of a Mortgage Default

| Event | What It Means For You | Typical Timeframe |

|---|---|---|

| Missed Payment | The grace period begins (usually 15 days). No credit impact yet. | Day 1-15 Past Due |

| Late Fees Applied | Your lender adds a penalty fee (4-6% of the payment) to your balance. | Day 16 Past Due |

| Credit Report Hit | The lender reports the 30-day delinquency to credit bureaus (Experian, etc.). | Day 30 Past Due |

| Formal Warnings | You'll receive a formal "Notice of Default" letter from your lender. | Day 45-90 Past Due |

These initial consequences set the stage for the more serious legal actions that follow. The key takeaway is that time is not on your side. The sooner you act, the more options you'll have.

This overview is just the starting point. Recognizing how serious a default is is one thing, but knowing you have options is everything. In the rest of this guide, we'll walk through the specific steps of the North Carolina foreclosure process and lay out real, actionable solutions to help protect your home and your financial future.

Navigating The North Carolina Foreclosure Process Step-By-Step

The word ‘foreclosure’ is scary, but the first step to taking back control is understanding exactly what it means. When you know what’s coming, you can get ahead of it. The fear of the unknown is often the worst part.

In North Carolina, the foreclosure process isn't random; it follows a very specific legal timeline. It's not an overnight thing. It actually starts long after you miss that first payment and moves through several distinct phases, each with its own set of rules and deadlines.

For homeowners in communities like Hope Mills and Spring Lake, knowing these steps is your best defense. It helps you protect your rights and see the opportunities you have to turn things around.

Let's look at how a simple missed payment can snowball.

As you can see, one missed payment leads to late fees, which then leads to serious credit damage. This is what kicks off the formal foreclosure process.

The Pre-Foreclosure Period

Before any legal action can even start, federal law gives you a critical window of time. Lenders are generally not allowed to begin foreclosure until you are more than 120 days—that’s about four months—late on your mortgage.

Think of this as your best chance to work things out. During these four months, your lender is legally required to reach out, discuss your situation, and tell you about your options, like a loan modification or forbearance. This isn’t just them being nice; it’s the law, designed to give you a fighting chance to keep your home.

Receiving The Formal Notice

If you’re still behind after that 120-day grace period, the lender will start the official process. In North Carolina, this usually begins with a formal letter, often called a "breach letter" or a "Notice of Default." This is the document that officially states you’ve broken the terms of your loan agreement.

This notice will spell out a few key things:

- The exact amount you owe to get your loan back in good standing.

- A firm deadline to pay that amount (usually 30 days).

- A clear warning that if you don't pay, they will accelerate the loan and start the process of selling your property.

This is a make-or-break moment. Ignoring this notice is the quickest way to lose control of the situation. It’s the bank’s way of saying they are serious about selling your home.

The Courthouse Auction

If the default still isn’t fixed, the lender’s next move is to schedule a public auction. In North Carolina, you’ll get a "Notice of Sale" at least 20 days before the auction date. This notice is also posted at the county courthouse and published in a local paper.

The sale itself is exactly what it sounds like: a public event, often held right on the courthouse steps, where your property is sold to the highest bidder. Unfortunately, homes sold at auction often fetch less than they’re actually worth, which can leave you with even more financial headaches. For most homeowners, the real goal is finding a solution before it ever gets to the auction. If you want to avoid this outcome, you can learn more about selling a house that is in foreclosure in North Carolina.

Key Takeaway: North Carolina has a 10-day "upset bid" period after the auction. This means someone can come in and place a higher bid on the property, which can sometimes extend the whole process.

Post-Sale Eviction Process

Once the sale is final and that upset bid period is over, the highest bidder officially becomes the new owner. If you’re still living in the house, you will have to move out.

The new owner will give you a formal "Notice to Quit," which is a written demand for you to leave. If you don't leave on your own, they can file an eviction lawsuit with the court to have you legally removed by law enforcement. This is the final, painful step that transfers possession and marks the end of your ownership.

Understanding The Long-Term Consequences Of A Default

Defaulting on your mortgage is more than just the immediate crisis of a foreclosure auction. It's the beginning of a long financial hangover that can take years—sometimes a full decade—to shake off. While losing your home is the most painful part, the aftershocks can reshape your financial life in ways you never expected.

Think of your credit score as your financial reputation. A mortgage default is the biggest black mark you can get, shouting "high risk" to any future lender. The initial hit is often a knockout punch.

The Crushing Blow To Your Credit Score

When that foreclosure officially hits your credit report, expect your score to plummet by 100 to 160 points, sometimes more. It’s one of the most destructive events your credit can endure, and that negative mark will stick around for seven long years.

This isn't just an abstract number. It translates into real-world roadblocks that make life more difficult and a lot more expensive. For instance, a trashed credit score can stop you from:

- Renting an Apartment: Landlords almost always run credit checks. A recent foreclosure is a massive red flag that often leads to an instant "no."

- Getting a Car Loan: If you're lucky enough to get approved, you'll be stuck with sky-high interest rates that bloat your monthly payments.

- Qualifying for New Credit Cards: Forget about getting unsecured credit. That door will be slammed shut, limiting your options in an emergency.

- Impacting Job Prospects: Believe it or not, some employers—especially in finance or government roles—look at credit history during background checks.

A mortgage default isn't a one-time problem; it's a long-term financial setback. Rebuilding from that kind of damage takes years of flawless financial behavior, but even then, the foreclosure remains a visible stain on your report for its full term.

The credit damage alone is a heavy burden, but here in North Carolina, the pain doesn't necessarily stop once the house is gone.

The Lingering Threat Of Deficiency Judgments

So many homeowners assume that once the bank sells the house, the debt is wiped clean. Unfortunately, in North Carolina, that’s a dangerous assumption. If your home sells at auction for less than you owe, that leftover amount is called a deficiency.

Let's say you owe $250,000 on your mortgage, but the bank only gets $200,000 at the foreclosure sale. That leaves a $50,000 deficiency. Under North Carolina law, the lender can actually sue you for that remaining $50,000 by getting a deficiency judgment.

If they win in court, the lender gets powerful tools to collect that money. They can start garnishing your wages, seizing funds directly from your bank accounts, or even placing liens on other assets you own. You could be paying for a house you no longer own for years to come.

Tax Implications And Future Homeownership

Here's another nasty surprise many people don't see coming: taxes. If your lender forgives part of your debt—say, in a short sale or deed in lieu of foreclosure—the IRS can treat that forgiven amount as taxable income. You could find yourself with a tax bill for tens of thousands of dollars you weren't prepared for.

Finally, getting back into homeownership is a long, uphill battle. Fannie Mae, one of the biggest players in the mortgage world, typically makes you wait up to seven years after a foreclosure before you can even think about qualifying for another home loan.

When you add it all up—a wrecked credit score, the threat of being sued for leftover debt, and being locked out of the housing market for years—it’s clear. Defaulting on your mortgage isn't a temporary hiccup. It's a lasting financial crisis, which is why finding a way out before it gets to that point is absolutely critical.

Exploring Your Options To Avoid Foreclosure

That moment you realize foreclosure is a real threat can feel like the ground is crumbling beneath you. But here's the thing: you are not powerless. Think of it like a train heading down the tracks; you still have the power to pull a lever and switch to a different, better track.

Taking action is the single most important thing you can do. Most lenders genuinely want to avoid the mess and expense of foreclosure. That means they're often willing to work with homeowners who are upfront and serious about finding a way out. Ignoring the letters just guarantees the worst-case scenario.

It’s a tough environment out there. In 2025, foreclosure starts in the U.S. jumped to 103,000 in the third quarter alone—that’s a 23% spike from the year before. While it's not at peak crisis levels, it’s a real problem. For a military family at Fort Bragg getting unexpected PCS orders or a landlord in Raeford dealing with a sudden vacancy, a default can spiral fast. Homes sold at auction lose an average of 27% of their value. You can see more on this in this deep dive into recent mortgage data.

Lender-Negotiated Solutions

Your first call should be to your lender. Before things get too far down the road, they have several tools designed to get you back on your feet without kicking you out of your home. These all hinge on cooperation.

Loan Modification: This isn’t a temporary fix; it’s a permanent change to your loan terms. The goal is to make your monthly payment manageable, maybe by lowering your interest rate, stretching out the loan term, or in some cases, forgiving a bit of the principal. This is a solid option if you’ve had a permanent drop in income but can still handle a smaller payment.

Forbearance Agreement: Think of this as hitting the pause button. Your lender agrees to temporarily reduce or even suspend your payments for a few months. It’s perfect for short-term crises, like a medical emergency or a temporary layoff, where you fully expect your finances to recover soon.

Repayment Plan: If you’ve only missed a couple of payments and are now ready to catch up, this might be the ticket. You simply agree to pay your regular monthly amount plus a little extra each month until you're current again. It’s a straightforward way to clear the past-due balance over time.

Key Insight: Communication is your most powerful tool. Lenders are far more willing to be flexible with homeowners who call them early and are honest about what's going on. If you wait until you’re months behind, your options shrink dramatically.

Options For Leaving The Home

Sometimes, no matter how hard you try, keeping the house just isn’t in the cards. When that happens, the goal changes. It's no longer about saving the property; it's about protecting your financial future and avoiding the long-term scar of a foreclosure.

Comparing Foreclosure Avoidance Strategies

Navigating these options can be confusing, so we've put together a simple table to help you see how they stack up against each other at a glance.

| Option | Best For… | Impact on Credit | Key Benefit |

|---|---|---|---|

| Loan Modification | Homeowners with a long-term income reduction who can afford a lower payment. | Minimal to moderate impact, can improve over time. | Keep your home with more affordable monthly payments. |

| Forbearance | Those facing a temporary financial setback (e.g., job loss, medical issue). | Minimal impact if the agreement is honored. | Provides temporary payment relief to get back on track. |

| Short Sale | Homeowners who are "underwater" and need to sell. | Significant negative impact, but less than foreclosure. | Avoids foreclosure and potential deficiency judgments. |

| Deed in Lieu | Homeowners who want a clean break and can't sell the property. | Significant negative impact, similar to a short sale. | Voluntarily hand back the keys and avoid a public auction. |

| Bankruptcy | Those with overwhelming debt beyond just the mortgage. | Severe, long-lasting negative impact. | The "automatic stay" immediately stops foreclosure proceedings. |

This table is just a starting point. The right path for you will depend on your specific financial situation, your home's equity, and what you hope to achieve.

A Closer Look at Exit Strategies

Short Sale

A short sale is when the bank agrees to let you sell your home for less than what you owe on the mortgage. This is a go-to solution when you're "underwater"—meaning the house is worth less than the loan.

It's not a walk in the park; it requires a ton of paperwork and the lender's final say-so. While it will still ding your credit score, it's generally seen as a much better outcome than a full-blown foreclosure and lets you walk away clean.

Deed in Lieu of Foreclosure

A "deed in lieu" is exactly what it sounds like. You voluntarily sign the deed over to the lender, giving them back the property. In exchange, they agree to cancel your mortgage debt.

This also hurts your credit, but it saves you from the public humiliation and stress of an auction. Lenders don't always go for it, especially if there are other liens on the property, but it can be a straightforward way to close a difficult chapter. You can learn more about how to stop foreclosure on your home in our detailed guide.

Choosing the right option is deeply personal. It comes down to your finances, your equity, and your goals for the future. The most important thing is to be decisive and explore every single path available to you.

A Direct Cash Sale Offers A Powerful Way Out

When you’re caught in the nightmare cycle of mortgage default, the options can feel slow and complicated. Trying to negotiate with the bank feels like hitting a brick wall. A short sale is a maze of paperwork. All the while, the foreclosure clock just keeps ticking.

But there is another way. A path that lets you bypass all that uncertainty and get a guaranteed exit.

Selling your home directly to a local cash buyer is a lifeline. It’s a clean, simple transaction designed for one thing: getting you out of a tough spot with speed and certainty. Instead of jumping through hoops for lenders and traditional buyers, you work directly with a company that buys your house as-is, for cash.

This approach completely changes the game. No more waiting for a bank’s approval or holding your breath hoping a buyer’s loan goes through. It's about getting a fair, firm cash offer that allows you to pay off your mortgage, salvage any equity you have left, and just walk away clean.

The Pure Simplicity of a Cash Home Sale

Working with a cash buyer like DIL Group Home Buyers cuts right through all the red tape that makes a normal home sale impossible when you're in a financial bind. The entire process is built to solve your problem, not add to it.

Here’s why it’s such a different experience:

- No Repairs Needed. Don't worry about the leaky faucet or the peeling paint. We buy properties "as-is," which means you don’t have to spend a dime or a minute on fixes.

- No Realtor Commissions. In a typical sale, you could lose up to 6% of your home's price to agent fees. With a direct sale, that cash stays with you.

- A Guaranteed Offer. You get a real, no-obligation cash offer. You never have to worry about a buyer's financing falling through at the last second.

- You Pick the Closing Date. If you need to sell in two weeks to stop a foreclosure auction, we can do that. If you need a bit more time to figure out your next move, we can work with that too.

A direct cash sale gives you a hard deadline for your mortgage problems. It replaces months of stress and uncertainty with a clear path forward, empowering you to settle your debt and start fresh without a foreclosure looming over you.

This kind of certainty is priceless, especially when life gets complicated.

A Real Solution for Real-Life Problems

Banks have rigid rules, but life doesn't always fit into their neat little boxes. A cash sale provides the flexibility you need to handle messy situations and gives you a practical way out when other options just won't work.

Think about these common scenarios we see right here in the Fayetteville area:

- Military PCS Orders: A soldier at Fort Bragg gets sudden orders to move. A mortgage default is a non-starter because it could threaten their security clearance. Selling for cash provides a fast, guaranteed closing so the family can relocate without leaving financial messes behind.

- Burnt-Out Landlords: Someone owns a rental in Hope Mills with a tenant who won't pay and a property that’s falling apart. They’re just done with the stress. A cash sale lets them unload the problem property—tenants and all—without dealing with evictions or repairs.

- Inherited Property from Afar: You inherited a house in Spring Lake but live on the other side of the state. It needs work, and you have no way to manage it from a distance. Selling to a local cash buyer is the easiest way to turn that property into cash without ever lifting a hammer.

By knocking down the usual barriers to selling a home, a direct cash sale delivers a fast and dignified exit. You can learn more about exactly how to sell your home for cash to see just how straightforward the process is. It's often the cleanest break you can make from the stress of a potential foreclosure.

Answering Your Toughest Questions About Mortgage Default

Once you start looking into this process, the questions can really start piling up. It's totally normal. Here, we'll tackle the most common concerns we hear from homeowners in North Carolina, giving you straight, practical answers so you can figure out your next move with a bit more clarity.

How Many Missed Payments Before Foreclosure Starts In North Carolina?

The clock doesn't start ticking right away. In North Carolina, federal law gives you a significant buffer. A lender generally can't even start the foreclosure process until you're more than 120 days behind on your payments—that's a full four months.

Once you hit that 120-day mark, the lender can legally send you a Notice of Default, which is the official starting gun for the legal proceedings. But please don't wait that long. The moment you think you might miss a payment, call your lender. You have far more options before things get formal.

Can I Still Sell My House If It's Already In Foreclosure?

Absolutely, yes. You have the right to sell your house all the way up until the final foreclosure auction. In fact, it's often the smartest move you can make to protect your financial future and salvage any equity you've built up.

Working with a cash home buyer is a powerful strategy here. Why? Speed. A cash buyer can close the deal in just days or weeks, which can literally mean the difference between you paying off the bank and the bank taking your home at auction.

Selling your home before the auction is your last real chance to stay in control. It lets you clear the debt, avoid a foreclosure stain on your credit report, and maybe even walk away with cash to help you get a fresh start.

Will A Mortgage Default Mess Up My Military Security Clearance?

Yes, it's a serious risk. Financial instability, especially something as significant as a mortgage default or foreclosure, can absolutely threaten a military security clearance. From a security standpoint, major debt is viewed as a vulnerability.

For service members stationed at Fort Bragg or other North Carolina bases, this is a huge deal. You have to get out in front of the problem to protect your career. Selling the house for cash is often a strategic way to quickly eliminate that financial weak spot before it shows up on your record and puts your clearance in jeopardy.

What In The World Is A Deficiency Judgment In NC?

This is something you really need to understand. A deficiency judgment is when a lender gets a court order to come after you for the rest of the mortgage debt after your home has been sold at a foreclosure auction. If the auction price wasn't enough to cover your total loan balance, you're still on the hook for the difference—the "deficiency."

And in North Carolina, lenders can and do pursue these judgments. This means even after the nightmare of losing your home, you could be facing wage garnishments or liens on your other property until that debt is paid. It's the foreclosure that keeps on taking.

Facing all this is tough, but you don't have to go through it by yourself. DIL Group Home Buyers gives you a fast, guaranteed cash offer to get you out from under the pressure. We can help you stop the auction, protect your credit, and move on. Give us a call for a no-pressure, no-obligation offer and see how we can help you find some peace of mind. Learn more at https://dilgrouphomebuyers.com.